How Much Fuel Does 3D Systems' Growth Rocket Have Left?

"Eh, good enough."

That seems to be the market's reaction to 3D Systems' earnings today. The company posted results that were right in line with analyst expectations, and several of its key metrics showed a degree of weakening on a sequential basis, although the 3-D printing company still notched a number of year-over-year improvements. Let's take a closer look at 3D Systems' first-quarter earnings to better understand why its stock is up by 7.5% this afternoon and whether the company can expect further gains in the days ahead.

By the numbers

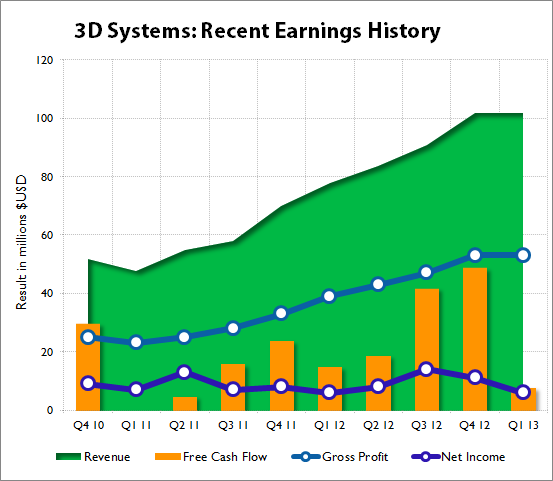

3D Systems reported revenue of $102.1 million and GAAP net income of $5.9 million, or $0.06 per share, for the first quarter. On an adjusted basis, the company reported $0.21 in EPS. Both numbers hit analyst targets: Wall Street was expecting $101.6 million on the top line and $0.21 on the bottom line. The top line grew 31% year over year thanks to an 81% increase in 3-D printer sales, but organic revenue clocked in at a more muted (but still respectable) 22% gain. Adjusted net income was up 43%, but GAAP net income showed a year-over-year decline.

What's interesting, however, is that this quarter was nearly identical to 2012's fourth quarter, and on some metrics 3D Systems actually reported sequential declines:

Sources: Morningstar; company earnings report.

3D Systems' revenue was sequentially flat, as was gross profit. Net income has been in decline for three consecutive quarters, and first-quarter free cash flow is lower than the year-ago quarter's result. This hardly seems like cause for celebration when this company has made waves by repeatedly setting new records with each new report. Technically, 3D Systems did post "record" quarterly revenue -- $102.1 million is a notch higher than the $101.6 million reported for the fourth quarter -- but this is a bit like celebrating a long jump of 10 feet and 1 inch after the previous record of 10 feet even broke an earlier mark by more than a foot.

3D Systems is also standing firm on 2013 guidance of $1.00 to $1.15 in EPS on $440 million to $485 million in revenue, which is a little unusual, given the company's history of raising its projections. Make no mistake -- these numbers are quite optimistic: 3D Systems has only accounted for 18% of its high-end EPS and 21% of high-end revenue with three quarters to go. But does that signal a shift in its expectations? It's a bit early to tell.

Overly optimistic?

It's interesting to see the difference between 3D Systems' progress and that of fellow old-guard 3-D printing specialist Stratasys , which saw revenue skyrocket in the first quarter following its Objet merger, even as net income fell. 3D Systems has historically been a steadier producer than Stratasys, which explains its greater share-price growth. But if the tide is turning in Stratasys' favor, then today's pop makes a bit less sense.

Industrial-scale 3-D printing upstart ExOne trounced both of these companies with its first public earnings report, and it is also being pulled higher by 3D Systems' report today. That doesn't seem any more logical than the pop all three companies enjoyed on ExOne's big day, as the latter company has a different focus from 3D Systems or Stratasys.

Here's where investors need to pause and take stock of the situation. Assuming that 3D Systems can grow revenue by 20% year over year for each of the next three quarters -- a pace Piper Jaffray analyst Troy Jansen thinks the industry could maintain "over the next several years" -- then 2013's total revenue will add up to $434 million, falling below 3D Systems' low-end projection. At a 30% year-over-year growth rate, revenue will hit the middle of expectations at about $460 million -- quite nice, but hardly the monster beat that would send Wall Street into a frenzy. Net income could certainly turn around, but more concerning is the year-over-year decline in free cash flow, as net income can be adjusted in all sorts of ways. If the free-cash-flow number doesn't improve markedly in the second quarter, then 3D Systems' growth expectations might be a tad too optimistic.

I wouldn't call today's report a buying opportunity. Thanks to lower GAAP net income and the day's growing pop, the company's valuation has once again nudged its way back toward record highs -- and that record high is not quite as appealing. The Motley Fool's Stock Advisor has recommended 3D Systems and maintains that recommendation, so they may disagree with my assessment -- and I appreciate the fact that we're allowed to disagree. It's what makes us "motley."

3D Systems is at the leading edge of a disruptive technological revolution, with the broadest portfolio of 3-D printers in the industry. However, despite years of earnings growth, 3D Systems sports a dizzying valuation. To help investors decide whether the future of additive manufacturing is bright enough to justify the lofty price tag on the company's shares, The Motley Fool has compiled a premium research report on whether 3D Systems is a buy right now. In our report, we take a close look at 3D Systems' opportunities, risks, and critical factors for growth. You'll also find reasons to buy or sell the stock today. To start reading, simply click here now for instant access.

The article How Much Fuel Does 3D Systems' Growth Rocket Have Left? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more insight into markets, history, and technology.The Motley Fool recommends 3D Systems and Stratasys. The Motley Fool owns shares of 3D Systems and Stratasys and has the following options: Short Jan 2014 $36 Calls on 3D Systems and Short Jan 2014 $20 Puts on 3D Systems. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.