Is Sysco's Stock Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Sysco fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell Sysco's story, and we'll be grading the quality of that story in several ways:

Growth: Are profits, margins, and free cash flow all increasing?

Valuation: Is share price growing in line with earnings per share?

Opportunities: Is return on equity increasing while debt to equity declines?

Dividends: Are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at Sysco's key statistics:

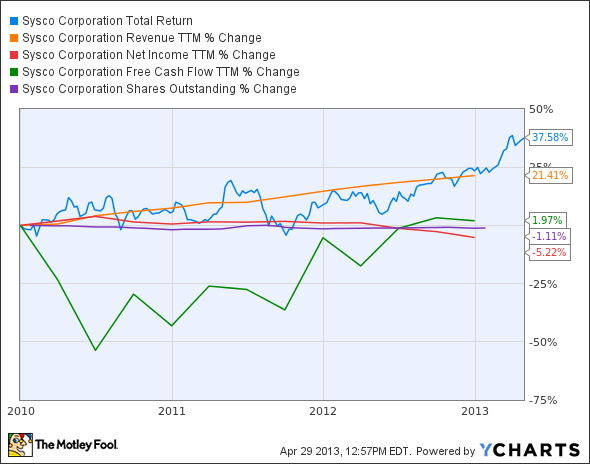

Source: SYY Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 21.4% | Fail |

Improving profit margin | (32.2%) | Fail |

Free cash flow growth > Net income growth | 2% vs. (5.2%) | Pass |

Improving EPS | (3.9%) | Fail |

Stock growth (+ 15%) < EPS growth | 37.6% vs. (3.9%) | Fail |

Source: YCharts. * Period begins at end of Q4 2009.

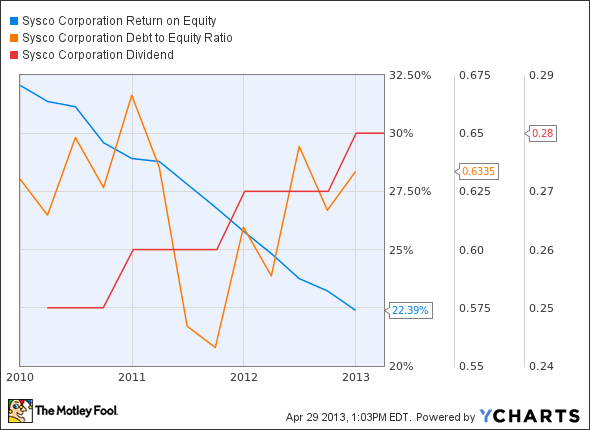

Source: SYY Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | (30.2%) | Fail |

Declining debt to equity | 0.5% | Fail |

Dividend growth > 25% | 12% | Fail |

Free cash flow payout ratio < 50% | 98.6% | Fail |

Source: YCharts. * Period begins at end of Q4 2009.

How we got here and where we're going

Things do not look good for Sysco. The only metrics showing positive momentum are revenue and share price, but neither is good enough to earn a passing grade. Indeed, Sysco narrowly avoids a complete goose egg only because free cash flow hasn't fallen into negative territory -- but investors looking for stable dividends may be in for some frustration, as Sysco is effectively paying out all of its free cash flow as dividends right now. Has this food-service leader given up on future growth, or is this just a low period before the company starts moving again in the right direction?

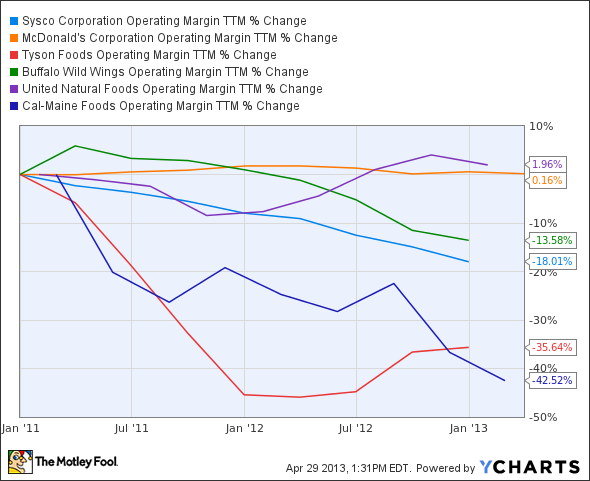

Last year, my fellow Fool Sean Williams pointed out that Sysco should be able to outscale the problems of rising food costs that have plagued both farm providers and restaurant buyers. That hasn't necessarily been borne out, as you can see below:

Source: SYY Operating Margin TTM data by YCharts.

Sysco has avoided the margin compression suffered by chicken producers Tyson and Cal-Maine Foods and which was more deeply felt by smaller food-service operator Nash-Finch . (It is omitted from this chart due to its drop into outright negative operating margin territory (a decline of roughly 250% in two years.) However, fellow food-service company United Natural Foods has actually improved its margins, and restaurant chains both large and small (well, mid-size) have done an admirable job of holding the margin line in the face of rising input costs. So it appears that scale alone isn't enough to help Sysco outrun the rising costs of its products.

However, scale does appear to be enough to attract yield-hungry investors to the stock, which is now neck and neck with United Natural for two-year share-price growth, despite the fact that only one of the two (it's not Sysco) has enjoyed EPS growth to match over the same period. Investors may be considering Sysco's international expansion as the key to future gains, but margins need to grow again to show investors that they aren't pursuing a dividend bubble. Sysco's valuation is at the highest it's been in five years -- including pre-crisis levels -- which implies that future growth may be more muted than many would like.

Putting the pieces together

Today, Sysco has few of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

Solid companies selling at depressed prices have consistently helped generations of the world's most successful investors preserve capital, minimize risk, and achieve long-term, market-trampling returns. For one such company, read our free report: "The One REMARKABLE Stock to Own Now." Just click here to get started.

Keep track of Sysco by adding it to your free stock Watchlist.

The article Is Sysco's Stock Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more insight into markets, history, and technology.The Motley Fool recommends Sysco. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.