Analysts Debate: Is Diageo a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing Diageo , one of the world's top purveyors of alcohol.

Diageo by the numbers

Here's a quick snapshot of the company's most important numbers:

Statistic | Result (TTM or Most Recent Available) |

|---|---|

Market cap | $75.1 billion |

P/E and forward P/E | 18.6 and 16.8 |

Revenue | $17.8 billion |

Net income | $4.1 billion |

Free cash flow | $2.9 billion |

Dividend yield | 2.3% |

Free cash flow payout ratio | 62% |

Cash / Debt | $1.1 billion / $13.6 billion |

Largest brands by volume share |

|

Sales share by region |

|

Sources: Yahoo! Finance, Morningstar, and company annual report.

Alex's take

At one point in the distant past, Diageo and other alcohol distributors might have been readily lumped into the "sin stock" category with tobacco companies. That link hasn't quite been severed, but it's weaker than it once was. However, the link between mind-altering substances and consistent profits is as strong as ever for segment leaders. Tobacco, alcohol, and even coffee have a hold on their users that isn't easy to break, and Diageo reaps the benefit of that (not entirely healthy) relationship as the world's largest spirits company.

Over the past 10 fiscal years, Diageo's operating margins have remained consistently high, ranging between 26% and 30%. Net margins have been in double digits for all but one of those years thanks to a one-time charge in 2003, and the lowest it's ever been during ordinary times was nearly 17% in 2010. That's not likely to tank any time soon, as Diageo has operations in 80 countries serving 180 "markets" around the world, and I've pointed out in my earlier in-depth analysis of the company that there's a great deal of growth remaining in many of these markets.

All you need to do to see the potential is to look at the preceding table, particularly at sales by region. The two areas with less than a fifth of the world's population make up more than half of Diageo's sales. The remaining areas are already heavily targeted by the company's growth engines, and when it comes to the Asian region (just think of India and China), Diageo is perfectly positioned -- between half and two-thirds of all alcohol consumed in that region is of the spirits variety.

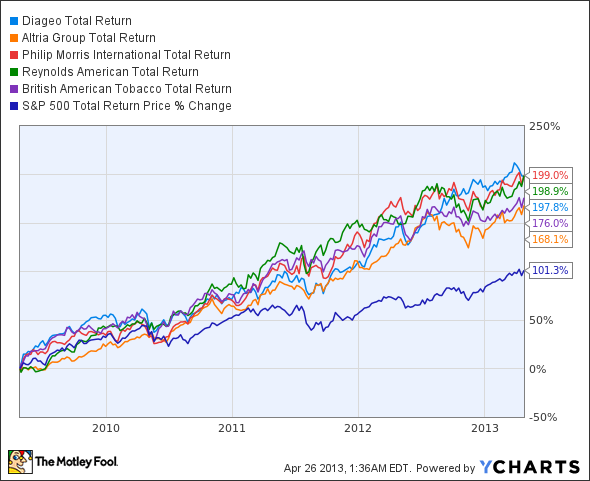

I'll grant that Diageo isn't in the elite-dividend class of tobacco sin stocks, but its total return has kept pace so well with those of tobacco companies enjoying less real growth that it doesn't matter:

DEO Total Return Price data by YCharts

This isn't to say that you should ignore the opportunity in these stocks, but over the long run, Diageo simply has better growth opportunities. Alcohol is heavily regulated, but not demonized as tobacco has been. Its consumption -- particularly of the spirits variety -- has been on the rise over the past few years, in contrast with declining tobacco use in many countries. Thanks to a diverse range of well-known brands, Diageo has that coveted pricing power in a competitive industry, and it also has a distribution infrastructure above and beyond any competitor. I have no problem giving this stock a vote of confidence for the long term, and you can read more about my rationale when you click here to see my in-depth opinion on Diageo.

Sean's take

Diageo is one of those ultimate nice-versus-vice plays. Diageo offers investors the chance to diversify globally into the most affordable legal high in the world: alcohol. Comparatively, alcohol is a vice and, despite a common misperception, not immune to economic downturns.

Diageo has two primary business focuses: its spirits business, composed of Johnnie Walker and Smirnoff Vodka, just to name a few of the many brands in its portfolio, and its beer business, headed by Guinness Stout and including several other brands. The dual focus gives Diageo an opportunity to further diversify its product portfolio both internally and geographically.

Whereas you might think spirits are the quicker "get-rich-quick" investments in alcohol consumption, you'd be dead wrong. Over the past 30 years, wine has drastically gained in popularity in relation to hard liquor, even taking 120 basis points of market share away from beer. That leaves hard liquor producers such as Beam , with its Jim Beam and Maker's Mark brands, Brown Forman , with its lineup of Jack Daniel's and Southern Comfort, and Diageo, in a tough spot of either raising prices to keep pace with rising commodity costs and margins, or keeping prices competitive but suffering on the margin front.

Things haven't been too much better on the beer front, with both domestic giant Anheuser-Busch InBev and Molson Coors looking abroad to make deals. With pocketbooks clenched tight as higher taxes and a slow recovery drain the American consumer, Anheuser-Busch took to purchasing Grupo Modelo's international operations, while Molson Coors gobbled up Eastern Europe's StarBev in a $3.5 billion transaction last year to get their share of faster emerging-market growth. Diageo is attempting to find new pathways to growth as well, but it's approaching things from a distilling angle by attempting to become a majority stakeholder in India's largest distiller, United Spirits.

For Diageo, there's a lot to like with regard to its premier dividend, its geographic diversity, and the general inelasticity of alcohol prices. But with regard to three-decade-long decline in spirits purchases in stores, as well as the fact that its organic growth forecast over the next two years is just 4%, I'm not exactly excited, either.

You can read a much more thorough analysis of my take on Diageo here, but ultimately, I'd consider Diageo a stock to buy, although I'd rather wait for a pretty sizable pullback to $90 before pulling the trigger.

Travis' take

While Sean is seeing a decades-long pullback in demand for liquor, I've seen plenty of evidence that high-end liquors are on the rise. Maker's Mark had so much demand that it tried to dilute its product before a PR backlash forced the company to go back on its plan. Scotch exports from Scotland are up 87% over the past decade, and this is showing in Diageo's 8% organic growth in strategic spirits. Anecdotally, I'm seeing more whisky bars, tequila bars, and high-end Scotches on the menu around the country as consumers begin to trend toward these drinks.

Liquor isn't a recession-proof business, and consumers are willing to trade down in bad times, but it's not a business that fluctuates a lot year to year, either. When you hold strong brands such as Johnnie Walker, Crown Royal, Bailey's, and Hennessy, you're also a step ahead of lesser brands with less distribution power. I think that gives Diageo the kind of competitive advantage I want in a stable industry.

The stock's value at 18.6 times earnings is only marginal, but this isn't the kind of business you get cheap. Still, I like the 2.3% dividend yield and think we continue to see strong enough growth that the stock can outperform the market. For a more in-depth look at my analysis of Diageo, click here.

The final call

With two in favor and one opposed, it looks like we'll be raising our glass to Diageo today. We do have concerns over the stock's valuation, but these are allayed by Diageo's superior market position and distribution infrastructure. There are not a lot of dominant liquor brands, and Diageo controls more than perhaps any other publicly traded company. All told, there are more reasons to buy than to sell, which is why we'll be making an outperform call on our TMFYoungGuns CAPS page as soon as possible. We're beating the indexes by about 400 points right now, and we're hoping that Diageo can push our outperformance even higher.

Solid companies selling at depressed prices have consistently helped generations of the world's most successful investors preserve capital, minimize risk, and achieve long-term, market-trampling returns. For one such company, read our free report: "The One Remarkable Stock to Own Now." Just click here to get started.

The article Analysts Debate: Is Diageo a Top Stock? originally appeared on Fool.com.

Fool contributors Alex Planes, Sean Williams, and Travis Hoium have no position in any stocks mentioned here. You can follow us on Twitter: Travis at @FlushDrawFool, Sean at @TMFUltraLong, and Alex at @TMFBiggles.The Motley Fool recommends Beam, Diageo, and Molson Coors Brewing. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.