Starbucks Stock Is Not a Value at Today's Price

Let's get one thing straight: Starbucks is a great company. The problem has to do with its stock. Like a frothy overpriced latte, shares of the Seattle-based coffee chain are just too darn expensive right now.

There are a number of metrics that can be used to demonstrate this. Take its dividend yield. The average stock on the S&P 500 yields 2.12%. Starbucks stock pays out only 1.5%.

And this isn't because the company is stingy with its earnings. Nothing could be further from the truth, in fact. Last year, it distributed nearly 40% of its net income to shareholders. The problem is with the denominator -- its stock price.

Here's another way to look at it. The most commonly used metric to value stocks is the price-to-earnings ratio. This gauges how much an investor must pay for each dollar of a company's earnings. Right now, the average stock on the S&P 500 has a P/E ratio of 18. Starbucks' ratio comes in at 31. That's a 72% premium over the broader market.

What explains the hefty price tag? First and foremost, as I noted earlier, it's a great company. It has a loyal customer base, treats employees like royalty compared to industry peers, and is led by one of the greatest chief executive officers alive.

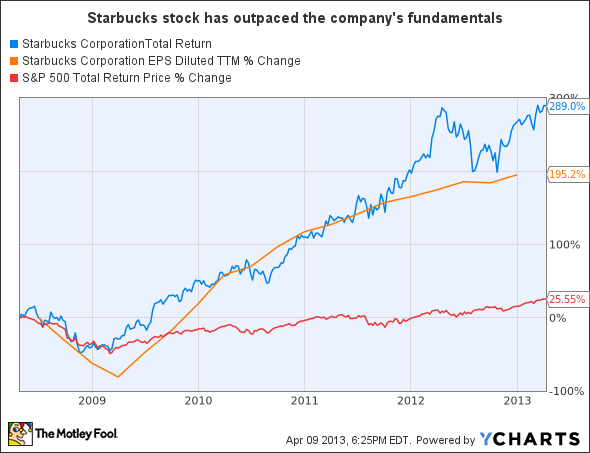

But beyond this, the growth in Starbucks stock has simply outpaced the company's fundamentals over the past five years. Consider the chart below:

SBUX Total Return Price data by YCharts.

As you can see, while the company has increased its earnings per share an impressive 195%, the price of its shares has bounded ahead by 289%. And to make matters worse, the bigger Starbucks gets, the slower it grows.

So what does this mean? If you ask me, it means that you should wait to buy Starbucks stock until the price comes down. Since the financial crisis, investors have flocked to solid companies with predictable revenue streams. Thus, once things resettle, it's not unreasonable to think that valuation multiples for traditional defensive stocks like Starbucks will readjust accordingly.

Profiting from our increasingly global economy can be as easy as investing in your own backyard. The Motley Fool's free report "3 American Companies Set to Dominate the World" shows you how. Click here to get your free copy before it's gone.

The article Starbucks Stock Is Not a Value at Today's Price originally appeared on Fool.com.

Fool contributor John Maxfield has no position in any stocks mentioned. The Motley Fool recommends Starbucks. The Motley Fool owns shares of Starbucks. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.