Is Texas Instruments Destined for Greatness?

Investors love stocks that consistently beat the Street without getting ahead of their fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with robust and improving financial metrics that support strong price growth. Does Texas Instruments fit the bill? Let's take a look at what its recent results tell us about its potential for future gains.

What we're looking for

The graphs you're about to see tell TI's story, and we'll be grading the quality of that story in several ways:

Growth: are profits, margins, and free cash flow all increasing?

Valuation: is share price growing in line with earnings per share?

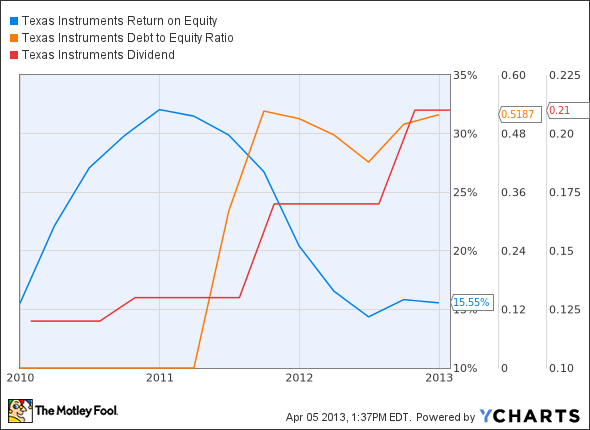

Opportunities: is return on equity increasing while debt to equity declines?

Dividends: are dividends consistently growing in a sustainable way?

What the numbers tell you

Now, let's take a look at TI's key statistics:

TXN Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 23% | Fail |

Improving profit margin | (59.1%) | Fail |

Free cash flow growth > Net income growth | 54.4% vs. 18.9% | Pass |

Improving EPS | 31.3% | Pass |

Stock growth (+ 15%) < EPS growth | 40.4% vs. 31.3% | Pass |

Source: YCharts.

*Period begins at end of Q4 2009.

TXN Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 0.2% | Pass |

Declining debt to equity | 61.7% (since Q2 2011) | Fail |

Dividend growth > 25% | 75% | Pass |

Free cash flow payout ratio < 50% | 28.1% | Pass |

Source: YCharts.

*Period begins at end of Q4 2009.

How we got here and where we're going

Most mature companies struggle to earn passing grades on many of these growth tests, but TI puts in a solid showing, earning six out of nine possible passing grades. The only real failing in the company's progress is a deteriorating profit margin. Can TI push that margin higher by the time we examine it next year? Let's dig a bit deeper into the company's potential in 2013.

We know one area that won't offer TI any potential for growth this year: mobile. That's because the chipmaker made a high-profile decision to stop developing for the space last year, citing the fact that many large customers were beginning to produce chip designs in-house. According to Foolish tech analyst Evan Niu, that may have been the right choice. Samsung has long developed most of its chips in-house, and other major mobile makers (say that five times fast) either are doing the same, or soon will. Licensing ARM Holdings' reference designs, tweaking them for efficiency, and outsourcing the fabrication to Taiwan Semiconductor seems to be the order of the day. Where does that leave TI?

TI seems to be doing all right focusing on what it knows. One thing it's been good at is developing simple Wi-Fi chips that are ideal for use in the nascent industrial Internet, a project spearheaded by General Electric but supported by many other companies under the broader designation "Internet of things." There may not be quite as many applications for these processors as there are for mobile devices, but Broadcom is TI's only serious competitor in this space, which implies a straighter path to domination -- by either party.

However, TI hasn't abandoned mobile completely. It's reportedly supplying the processor for Amazon.com's entry-level Kindle Fires, continuing a relationship that began with earlier Fires. That doesn't seem like it would be enough to reverse a slide that you can clearly see in the charts up above. TI's latest quarter experienced both sequential and year-over-year revenue declines, a trend that is sure to turn some passing grades into failures next year, should it continue. Despite that weakness, TI execs felt comfortable enough to boost the dividend by a third earlier this year, which is at the least a show of confidence in the company's financial future. Will this optimism be justified? We'll have to wait and see.

Putting the pieces together

Today, TI has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

It's incredible to think just how much of our digital and technological lives are almost entirely shaped and molded by just a handful of companies. Find out "Who Will Win the War Between the 5 Biggest Tech Stocks" in The Motley Fool's latest free report, which details the knock-down, drag-out battle being waged among the five kings of tech. Click here to keep reading.

Keep track of Texas Instruments by adding it to your free stock Watchlist.

The article Is Texas Instruments Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter, @TMFBiggles, for more insight into markets, history, and technology.The Motley Fool recommends Amazon.com and owns shares of Amazon.com and General Electric. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.