How Profitable Is Main Street Capital?

Earlier this week, I took a look at where Main Street Capital gets its money, but revenue is only part of the story. What's more important is how much of this revenue eventually makes its way to investors in the form of earnings.

Main Street is unique because it receives special tax treatment as a business development company, and because of this, it's not as simple as subtracting expenses from the net revenues earned as it is for other companies. Nevertheless, when compared to others in its business, it seems to be a strong performer and should be able to perform well for quite some time.

What unique tax treatment?

Similar to real estate investment trusts (REITs), a business development company (BDC) can avoid paying corporate income taxes on its shareholder distributions as long as it distributes 90% of its "investment company taxable income" each year. Because of this, like REITs, BDCs also tend to have high dividend yields and tend to be favored by investors seeking regular income. Currently, Main Street's dividend yield is near 6%, making it an attractive investment option.

Because of its unique tax treatment, the "bottom line" at Main Street is different from most companies. Whereas most companies will report a net income after subtracting out expenses from revenues, Main Street is required to account for the gain in its investments as well, and reports the net increase in net assets each quarter. Earnings per share are then determined by dividing the number of outstanding shares by this number, which is why Main Street's payout ratio may not always equal 90%:

2012 | 2011 | 2010 | |

|---|---|---|---|

Net increase in net assets per share | $3.53 | $2.76 | $2.38 |

Dividends paid per share | $1.71 | $1.56 | $1.50 |

Payout ratio | 48.4% | 56.5% | 63% |

Source: Company 10-K.

Expenses still matter

Though Main Street has a unique way of determining its net income, we can still take a look at its expenses to see its costs for doing business. A large portion of the capital that Main Street uses when investing in companies comes from the Small Business Administration (SBA) in the form of loans, which totaled $225 million at the end of 2012. The interest paid on these and other loans was the largest expense paid by Main Street during 2012, totaling $15.6 million during the year.

Other expenses at Main Street also totaled around $15.6 million for the year. Unlike a bank like PNC Financial, which needs 56,000 employees to run its business, Main Street has only 30 employees, keeping personnel costs to a minimum. Its business model doesn't require a lot of employees, but as it continues to expand, it could potentially add more down the road.

What about some other BDCs?

Traditionally, what Main Street and other BDCs do is typically the realm of private equity firms, so there aren't a whole lot of public BDCs doing similar work. Nevertheless, there are a few that tend to garner some attention, and they are all close to the same size:

Company | Market Cap | Net Investment Income* | Net Increase in Net Assets* | Profit Margin |

|---|---|---|---|---|

Main Street Capital | $1.08 billion | $90.5 million | $104.4 million | 115.3% |

Apollo Investment | $1.67 billion | $322.2 million | $155.9 million | 48.4% |

Prospect Capital | $894.3 million | $488.0 million | $180.3 million | 36.9% |

Source: FinViz.com and Company filings. *Trailing 12 months.

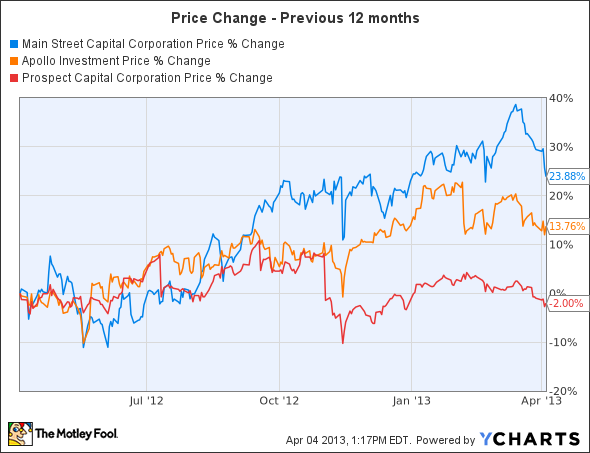

Without diving too deep into Apollo Investment or Prospect Capital, Main Street appears to be getting a boost from the growth of its equity investments, at least it has over the past 12 months, reporting $60.9 million in net gain and appreciation. These gains are also shown in share appreciation over the past 12 months, with Main Street posting almost twice the return of Apollo:

This in and of itself does not make Main Street the better investment, and both Apollo and Prospect Capital have higher yields than Main Street, making them attractive in their own ways. Nevertheless, one thing that Main Street appears to be doing well is investing in appreciating companies, which will hopefully serve them well over the coming years.

Is "business development" the new wave?

Main Street Capital and its current compatriots are doing alright for themselves investing in smaller companies that need additional capital. Even Goldman Sachs is getting involved, filing paperwork to start its own business development company to try to take a piece of the BDC pie. In my opinion, this is a segment of our economy that will continue to improve before it gets worse, giving plenty of opportunity for Main Street and others to succeed.

Its new interest in business development notwithstanding, Goldman Sachs could still be an interesting addition to your portfolio. To help figure out whether Goldman Sachs is a buy today, I invite you to read our premium research report on the company. Click here now for instant access!

The article How Profitable Is Main Street Capital? originally appeared on Fool.com.

Fool contributor Robert Eberhard owns shares of Main Street Capital. The Motley Fool recommends Goldman Sachs. The Motley Fool owns shares of PNC Financial Services. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.