How's That Long-Term Biotech Investment Looking?

If you invested in Arena Pharmaceuticals a year ago, you're sitting on some pretty solid gains; shares are up about 150% since last March. The Nasdaq over that timeframe is up only about 4%, while the Dow is doing a little better, up 10%, but still nowhere near the returns the biotech has seen.

The gains, of course, are thanks to getting its first product approved. If you bought a year ago and sold just after the approval of its obesity drug Belviq, you could have pocketed nearly a five-bagger.

Zoom out the chart a little more, though -- let's say five years -- and the investment doesn't look so good. Buying a Nasdaq index fund would have produced double a return over holding shares for that long.

Delays are costly

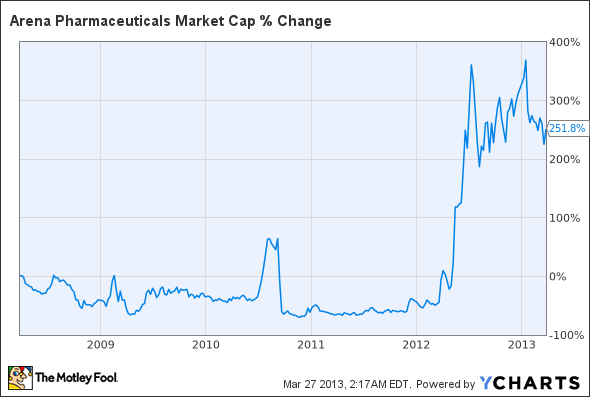

That spike up and down in 2010 was when the company produced positive data showing that its drug helped patients lose weight, and then the FDA advisory committee voted 9-5 recommending against approval. The agency subsequently followed suit, rejecting Belviq and asking for more safety data.

Before that, Arena was your typical biotech with multiple shots on goal. There was APD125 to treat insomnia, APD791 for arterial thrombosis, and a collaboration with Johnson & Johnson to develop a diabetes drug codenamed APD597, which the pharma handed back to Arena in 2010. None of them turned out to be as potentially lucrative as Belviq.

Despite not much gain in the share price over the past five years, Arena's valuation has grown substantially.

ARNA Market Cap data by YCharts.

The share price hasn't risen by nearly as much because Arena has had to sell additional shares to raise capital. Drug development isn't cheap. Over the past five years, share count has more than tripled. The pie is bigger, but each share constitutes a much smaller slice.

But what about the next five years?

No point in dwelling -- too much -- in the past; it's the future that counts.

Clearly, most of Arena's current valuation is locked up in Belviq. The drug should launch shortly, as soon as the Drug Enforcement Agency makes a final decision about the its potential level of abuse. Belviq will be marketed by Arena's partner Eisai.

Based on how VIVUS' competing drug Qsymia has done, I wouldn't expect a fast launch for Belviq. Arena and Eisai still have a lot of work to do convincing payers that it's worth covering the drug; otherwise it's too expensive for many patients to bother with.

The companies also have to alleviate doctors' worries about the safety. Wyeth's fen-phen and Abbott Labs' Meridia, which were both pulled from the market for safety reasons, have doctors questioning the risk-benefit ratio for new drugs. It'll take some time for doctors to get comfortable with Qsymia and Belviq and prescribe them for a large fraction of their obese patients.

Can it be done? Absolutely. I believe both drugs could be blockbusters some day. Same goes for Orexigen's Contrave, which is further behind in development. The potential market for obesity drugs is huge.

How long it takes to get over the hurdles will determine whether Arena has to raise capital again. At the end of last year, Arena had $156 million, got about $5 million for licensing rights to sell Belviq in South Korea to Ildong Pharmaceutical, and will receive another $65 million from Eisai following final DEA scheduling.

Arena plans to burn through up to $100 million this year, consisting of up to $28 million in general and administrative expenses and up to $71 million on research and development. Even if it gets only minimal revenue from its share of Belviq sales, Arena shouldn't have to raise capital this year.

It could run into issues in 2014, especially if its pipeline progresses well. All the development-stage drugs are currently in phase 1, which is relatively cheap to run. Research and development costs will increase as it launches larger trials.

Of course, if Arena does have to raise additional capital before becoming cash flow-positive, hopefully it'll be at a higher valuation, which will reduce the dilution.

Are there any reasons left to own Arena?

With Belviq's FDA approval now a distant memory, investors are scrambling to decide whether to buy or sell Arena. In the Fool's premium research report, senior biotech analyst Brian Orelli takes you through a comprehensive look at this contentious stock, including its massive opportunity, potential pitfalls, and key reasons to both buy and sell. To find out more about Arena, click here to access your report today.

The article How's That Long-Term Biotech Investment Looking? originally appeared on Fool.com.

Fool contributor Brian Orelli has no position in any stocks mentioned. The Motley Fool recommends and owns shares of Johnson & Johnson. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.