Analysts Debate: Is Monster Beverage Still a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing Monster Beverage , the largest publicly traded energy drink purveyor in the world.

Monster by the numbers

Here's a quick snapshot of the company's most important numbers:

Statistic | Result (TTM or Most Recent Available) |

|---|---|

Market Cap | $8.1 billion |

P/E and forward P/E | 26.2 and 16.4 |

Revenue | $2.1 billion |

Operating margin | 26.7% |

Net income | $340 million |

Free cash flow | $238 million |

Cash and investments | $320 million |

Sales by customer type |

|

Case sales (192-ounce cases) |

|

U.S. alternative* beverage market share | 4.7% |

Key competitors |

|

Sources: Morningstar, corporate reports, Net Applications, and press releases.

* Includes ready-to-drink iced tea, lemonade, juice and fruit beverages, dairy and coffee drinks, sports drinks," natural" sodas, flavored sparkling beverages, single-serve water, and energy drinks.

Alex's take

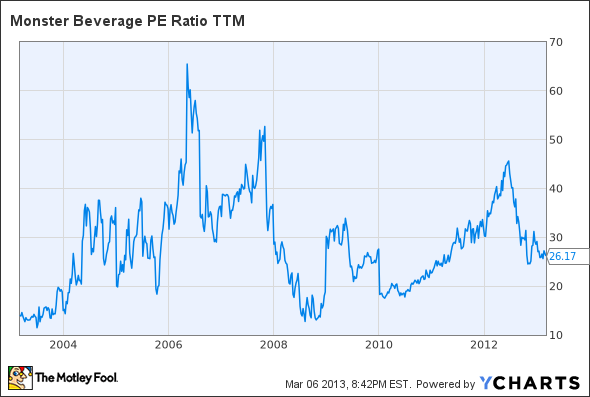

I've had my eye on Monster for some time, but I found it to be too pricey an opportunity last year as its P/E soared toward bubbly territory:

Source: MNST P/E Ratio TTM data by YCharts.

However, now that investors have backed away -- a flight that began, contrary to what you may think, well before the legal challenges over several purported deaths -- Monster is starting to look a bit more palatable. With the exception of a brief period after the financial crash and in early 2010, Monster's valuation hasn't been this low in a decade. Is this an opportunity or the warning sign of a pending sales slowdown? While Monster didn't offer up any annual guidance for its 2013 fiscal year, we can extrapolate its growth rate from analyst estimates:

Year | Revenue Growth* | Net Income Growth* |

|---|---|---|

2009 | 11% | 94% |

2010 | 14% | 1% |

2011 | 31% | 35% |

2012 | 21% | 19% |

2013 (estimated ) | 13% | 22% |

Sources: Morningstar, Yahoo! Finance. * Year-over-year growth rate.

Monster can't keep up its monster (pardon the pun) growth rates forever. The energy drink segment is reaching maturity in the American market, according to a Nielsen report on a 13-week sales period that ended in mid-February. During this period, energy drink sales grew by 5.7% on a dollar-value basis, which is not that far ahead of Coca-Cola's 3.2% year-over-year revenue growth rate and comes in at less than half the 13.7% year-over-year revenue growth rate Starbucks posted from its 2011 to 2012 fiscal years.

However, Monster is one of the few energy drink purveyors to outpace its category's growth, as Nielsen reported an 8.1% year over year for those 13 weeks. Pepsi's AMP is fading fast, its sales down 17.6% year over year, but sales of Coke's NOS Energy (which is starting from well back in the energy drink pack) are up 11.7%. The energy drink market, at least in the U.S., is increasingly becoming a two-way battle between Monster and Red Bull, which increased its sales by 10.8% during this 13-week period.

Monster has one big thing going for it that Red Bull does not, and that's variety. A quick glance at Monster's expansive product list, outlined in its latest annual report, shows not only a wide variety of Monster Energy flavors and formulations but also two primary varieties of chilled coffee beverage, several juice drinks, an iced tea, and an energy-enhanced line of juice-based "Rehab" drinks. Monster classifies most of these as subsets of its energy drink segment, but many of these brands could be considered something else within the wider alternative beverage category -- and, as you'll recall from the earlier chart, Monster's relatively small share of that category still presents significant upside.

The other thing to consider is that, while Monster's P/E may seem a bit pricey, it's not far out of line when compared to its peers, especially when forward growth rates are taken into account:

Company | P/E Ratio | 2013 Est. Income Growth |

|---|---|---|

Monster | 26.2 | 22% |

Coca-Cola | 19.8 | 7% |

Pepsi | 19.6 | 7% |

Dr Pepper Snapple | 14.9 | 5% |

Starbucks | 30.7 | 21% |

Sources: YCharts and Yahoo! Finance.

Despite a cheaper valuation than Starbucks, Monster is expected to grow at a faster rate this year. The only thing Monster does not have as an advantage over these competitors is a dividend, but a modest divided is easily in reach -- a 1% yield, at current prices, would take up only a third of the company's current cash flow. That's just hypothetical, but Monster's history of growth is very real, and it appears poised to continue to grow faster than the pack. For these reasons, I have no problem making an outperform call today.

Travis' take

Let me first admit that I don't like Monster drinks. I think they're too large and I prefer a small 5-Hour Energy or a Red Bull if there's an adult beverage involved. With that off my chest, let's get down to the investment side of things.

There's no doubt that the energy drink category continues to grow and through product expansions Monster is taking share in growing markets outside of traditional energy drinks. This is where I find Monster to be an appealing company. With the Java and Rehab lines, Monster has proven that it can expand beyond the traditional energy drink and adapt to new markets. This will be key as the energy fad dies down or morphs into something new.

I won't rehash the numbers Alex ran through above but I'll say that I see Monster's stock as fairly valued, but by no means a steal. Starbucks, Pepsi, and Coca-Cola have far bigger and better brands in far more established markets so they deserve a premium price. Monster doesn't deserve the same and with net income up only 5% in the fourth quarter, I'm afraid projections for 2013 are overcooked.

I do have one big red flag that caught my eye -- management. Monster's management has chosen to effectively burn cash over the past year by buying back shares of stock. The company spent $499.8 million on a 2011 buybacks program during 2012, buying shares at an average price of $57.35. On Nov. 13, 2012, the board authorized another $250.0 million buyback program, of which management burnt through $236.5 million by the end of the year, buying at an average price of $49.26. Today, shares trade at $47.75 so the buybacks were a terrible use of cash.

I fail to grasp how companies trading at insane multiple seem to think that buying back shares is a good use of cash when study after study shows it's terrible for shareholders. When a company is trading at a discount to book value, sure, buy back shares, but Monster is nowhere near that.

I'd be OK with owning Monster, but only if the stock falls farther. I just don't see downside protection at the current price, especially if management keeps burning through excess cash. I'd be comfortable buying at $40 per share, a price limit I'll propose for the group.

Sean's take

Since my colleagues are being up-front, I admit that I loathe energy drinks. Period. You won't catch one in my hand or near my fridge. Knowing that, I'm pretty certain you can guess where this is headed.

As Alex and Travis both mention, Monster's boom is a direct result of the rapid growth in the energy drink sector. Few brands offer anything close to the number of drink alternatives Monster gives consumers. However, one of the biggest concerns I've stressed with Monster -- and why I'd avoid owning it like the plague -- has to do with the potential for increased levels of government or FDA regulation in the energy drink industry.

In October, Monster was hit with an FDA probe into the safety of its energy drinks following accusations of alleged deaths related to Monster's energy drink. Even if the FDA can't physically prove causality between Monster's energy drinks, which Monster itself has deemed perfectly safe, and the deaths currently being investigated, it could be enough probable cause for activist mayors such as Michael Bloomberg to place a ban on the high-caffeine substance down the road and further crush the public image of the company.

Monster is still also a mile from what I would call an attractive valuation. Being that a massive chunk of its revenue is tied to the energy drink market - a market I find to be highly susceptible to future regulation - I would only be willing to invest in Monster if I were getting a forward P/E that's considerably below the sector average. But that's not the case, with Monster's forward P/E tracking similarly to just slightly higher than Coca-Cola and PepsiCo. despite their considerably more diverse product offerings and the fact that both pay a dividend whereas Monster does not.

Reporting an income rise of just 5% last quarter, Monster's growth has tapered off quicker than many expected as it's been forced to spend quite a bit on marketing its non-energy drinks just to make a dent in markets dominated by Coca-Cola and Pepsi. With growth slowing and the threat of regulation rising, I say stay far, far away from Monster Beverage.

The final call

We're fairly split on this one. I (Alex here) would like to make an outperform call, but with Travis waiting for a better entry price and Sean not interested in a stock with possible regulatory risks, we don't have the votes to put this one on our TMFYoungGuns CAPS portfolio today. We're beating the indexes by almost 400 points after just one year of selections, so here's hoping that our next debate produces more agreement and a new addition to the CAPS portfolio.

Got a great stock you'd like us to debate soon? Send us an email with your idea, and we just might feature it on an upcoming Analysts Debate!

The stakes are high for Monster Beverage these days. The stock had been nothing short of a rocket, but recent developments have sent shares spiraling downward. Health scares sparked a number of investigations at the state and federal level into the energy drink's role in several fatalities. With the company's value slashed in half, investors are wondering whether Monster Beverage is a value or a bust in the fast-growing energy drink category. Find out now in our brand-new premium research report, which details all the ins and outs you need to know about Monster Beverage. Click here now to claim your copy and start reading today.

The article Analysts Debate: Is Monster Beverage Still a Top Stock? originally appeared on Fool.com.

Fool contributors Travis Hoium, Alex Planes, and Sean Williams do not have positions in any companies mentioned here. You can follow Travis on Twitter at @FlushDrawFool, Sean at @TMFUltraLong, and Alex at @TMFBiggles.he Motley Fool recommends and owns shares of Monster Beverage, PepsiCo, and Starbucks. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.