Can Melco Crown Continue to Shine?

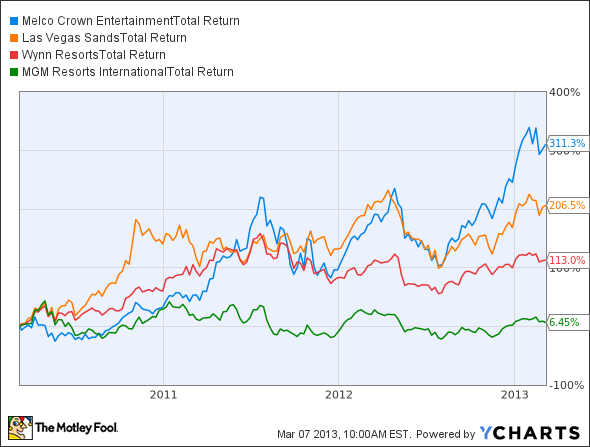

Melco Crown has been one of the best performing stocks on the market over the past three years, easily surpassing rivals on a total return basis. Even Las Vegas Sands and Wynn Resorts , who generate most of their revenue in Asia, haven't kept up with Melco's pace.

MPEL Total Return Price data by YCharts.

How does this much smaller rival continue to beat out competitors with much greater resources?

Growth that just won't stop

The first reason Melco Crown's stock continues to outperform is the company's improving finances. Fourth-quarter revenue grew 9% to $1.1 billion, EBITDA was up 7% to $247.5 million, and net income was $108 million, or $0.20 per share.

But the key for Melco is why revenue and profits continue to grow. For that, we need to look at the company's improving competitive position.

Location, location, location

The single biggest reason Melco Crown has been able to outperform rivals is the central location of its largest casino. City of Dreams sits in the middle of Cotai and it has been able to leverage three resorts from Las Vegas Sands and one by Galaxy to draw more revenue there.

Look at the image above and then compare revenue, EBITDA, and mass-market growth over the past year on the Macau Peninsula versus Cotai. You can draw a quick conclusion that gaming is trending toward Cotai, particularly in the mass market.

Q4 Revenue Growth Y/Y | Q4 EBITDA Growth Y/Y | Mass-Market Table Drop Growth Y/Y | |

|---|---|---|---|

City of Dreams | 11% | 17.6% | 24.5% |

The Venetian | 10.3% | 17.6% | 10.5% |

Wynn Macau | -9.7% | -9.5% | -1% |

Sands Macau | -2% | 4.2% | 3.1% |

Source: Company earnings reports.

Just the location of Melco's Cotai resort has been a huge advantage for the company and is a main driver of its stock performance. And it doesn't look like the draw of Cotai will stop any time soon. Las Vegas Sands is working on another resort, Wynn is as well, and MGM Resorts will soon join the fray with a resort next to City of Dreams. If the mass-market continues to grow like it has recently then Melco Crown should see improving results.

Low expectations

To outperform on the stock market you have to do well financially but it doesn't hurt if the market sets low expectations to begin with. Two and a half years ago, I lamented that Melco Crown was the worst performing gaming company in Macau by reporting mid-teen EBITDA margin when rivals exceeded a 30% margin.

During the second quarter of 2010, City of Dreams reported a 13.9% EBITDA margin. Today, that margin is up to 28.4%, more than doubling over that time. Even if revenue didn't more than double, EBITDA would have doubled over that time. With growing revenue and expanding margins Melco Crown was able to rapidly grow the bottom line and it's shown on the stock market.

Will the outstanding performance continue?

The big question for investors today is; will the great performance continue?

There's not a lot more the company can squeeze out of existing revenue, so margin expansion won't be a plus. The company has a project in the Philippines and another one on Macau, but the Cotai project doesn't currently have table games. We also don't know what the impact of its venture in the Philippines will be when it is completed later this year.

I think that financially the company will continue to improve but the worrisome part is the company's valuation. In late 2010, the company had an enterprise/EBITDA value of 16 at a time when Macau was growing nearly 60% annually and the company had margin upside. Today, the company trades at 13 times EBITDA and Macau will grow in the single digits or low double digits for the year.

Melco Crown still has upside, especially if pending projects are completed on time and operate profitably, but it isn't the steal it once was. I doubt the stock will wildly outperform rivals over the next three years, one of the challenges of being the hottest stock in gaming.

More on Melco Crown

Melco Crown is often a forgotten company in gaming, but it has tremendous upside from Studio City and its partnership in the Philippines, which could more than double the company's revenue base. This being a more speculative investment, is it worth the risk for smaller investors? The Motley Fool answers this question and more in our most in-depth Melco Crown research available for smart investors like you. Thousands have already claimed their own premium ticker coverage, and you can gain instant access to your own by clicking here now.

The article Can Melco Crown Continue to Shine? originally appeared on Fool.com.

Fool contributor Travis Hoium owns shares of Wynn Resorts. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.