3 Companies That You Can't Survive Without in 2028

Getting sticky -- whether gum on the bottom of your shoe or that feeling you get on a hot, muggy day -- is something we try to avoid at all costs.

But in the world of business, sticky is good, at least when it comes to attracting lifetime customers. There are lots of ways to define a "sticky" business, but for this article, a company can be considered sticky when:

It provides something that you generally must use or suffer some type of consequence.

Switching to a competitor would either be prohibitively expensive, or far too inconvenient.

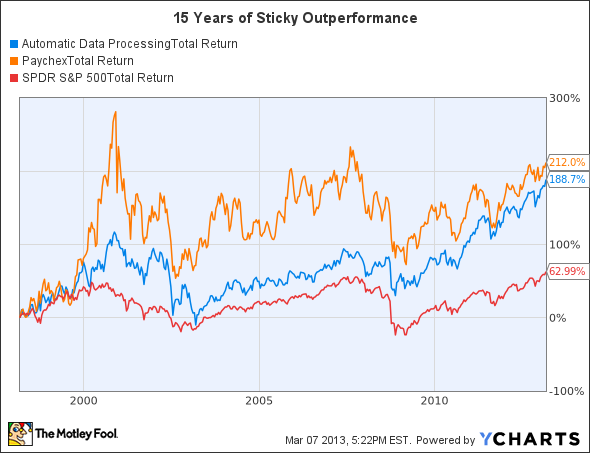

Usually, when we talk about sticky stocks, we're talking about large companies in slow-growth industries. Names like Automatic Data Processing and Paychex are prime examples. These two companies handle things that must get done -- paying one's employees -- and over time, become far too inconvenient for a client to switch to someone else.

If you look at how the stocks of these payment solution companies have performed over the last 15 years, there's no doubt that their stickiness garnered big returns for investors.

ADP Total Return Price data by YCharts.

I'd like to flip the approach to investing in sticky stocks on its head

Usually, sticky stocks provide investors with low volatility while paying out some nice dividends.

But what if we could find companies that were not yet as sticky as some stalwarts, but were undeniably headed in that direction? These stocks would certainly be more volatile, and probably won't offer a dividend. But for true buy-and-hold investors, those risks could be more than worth it over the next 15 years of potential stickiness.

With that approach in mind, here are three companies I consider to be some of the next decade's stickiest.

Intuit

If you're anything like me, or roughly 30 million other Americans, when tax time hits, there's only one place to head: Intuit's TurboTax.

Intuit's products qualify as sticky because there are certainly consequences for not paying your taxes and, as you'll see, there are prohibitive cost and convenience factors that keep customers coming back.

Though it currently makes up only about 35% of the company's revenue, I'm going to focus on the growing demand for TurboTax -- rather than the equally successful and larger Quicken suite -- to show why Intuit will get stickier as the decade goes on.

TurboTax is infinitely easier than trying to figure out the tax code yourself, and a lot cheaper than taking all of your papers to a professional to complete your taxes for you. And after you've filed with TurboTax once, it remembers and stores all your past information, making each successive year's tax returns easier to complete than if you started all over.

And yet, there is still a huge market opportunity for Intuit to tackle.

Source: Intuit. TurboTax fits in the green "Software" slice.

Many older folks who started doing their taxes before TurboTax was around are less likely to use the product. But every year, 3.5 million taxpayers exit the system, and 5 million more enter.

Just like cigarette companies, Intuit is laser-focused on getting these recent graduates into their ecosystem right off the bat. The company has already come out with a SnapTax solution that allows mobile-minded youth to complete their taxes from their smartphones and tablets alone.

LinkedIn

The human resources division is a vital part of any company, with the responsibility for recruiting the top talent that becomes the lifeblood of continued survival in the business world. What was once a haphazard, word-of-mouth ordeal has been streamlined through the use of LinkedIn's powerful network.

Instead of focusing on individuals who sign up with LinkedIn, I'd like to zero in on the businesses that use the service. A full 53% of revenue comes from companies that pay to use the site to fulfill their recruitment needs. And this segment -- dubbed Talent Solutions -- has grown from generating just $17 million in the first quarter of 2010 to $161 million last quarter.

Source: LinkedIn.

As LinkedIn has grown its base of individual members from 64 million in 2010 to 202 million today -- a 215% increase -- it becomes even more perilous for a company to go with anyone other than LinkedIn. Not only would the pool of potential candidates be thinner, but the costs of hiring a firm or full HR staff would also be greater.

Medidata Solutions

Finally we have a company you may not have heard of in Medidata. The company basically helps medical companies do everything possible to centralize and lower the costs of clinical developments and medical trials.

As fellow Fool Sean Williams excellently pointed out last week, if there's one sector poised for huge gains over the next decade, it's health care. With international markets waiting to be tapped, the results of Obamacare set to take effect in 2014, and a growing population of long-lived retirees, there's never been more incentive for medical companies to find solutions to tomorrow's health problems.

Since the market bottomed in 2009, the company has quickly gobbled up market share and increased its application backlog.

Source: SEC filings.

Obviously, a drug company has to figure out some way to navigate the approval process, or it will never gain approval. And once a pharmaceutical company has become familiar with a standard system, the lag and cost of switching to a different system could produce disastrous results on productivity.

Don't forget to balance things out

Of course, there's no guarantee that these three companies will become the best sticky plays of 2028, and it's important to balance out your portfolio. To do so, I suggest you check out the Fool's special report: "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, and includes three companies that have already established their stickiness; so just click here and get your copy today.

The article 3 Companies That You Can't Survive Without in 2028 originally appeared on Fool.com.

Fool contributor Brian Stoffel owns shares of LinkedIn. The Motley Fool recommends Automatic Data Processing, Intuit, LinkedIn, and Paychex. The Motley Fool owns shares of Intuit and LinkedIn. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.