1 Key Reason Big-Bank Investors Should Love "Too Big to Fail"

"Too big to fail" is alive and well, and investors in the U.S.'s biggest banks should be pleased that that's the case.

Equity investors that own any of the four biggest banks -- Wells Fargo , Bank of America , Citigroup , and JPMorgan -- are getting a boost from the fact that if any of these institutions ended up on the ropes, Uncle Sam would almost undoubtedly come to the rescue. Investment banking giants Goldman Sachs and Morgan Stanley would also likely get a rescue in dire times.

The benefit to shareholders of these banks isn't the fact that a future bailout would prevent the respective stocks from going to zero. Few great investment theses start with "If something goes terribly wrong, it won't go all the way to zero. Just very close." The benefit also isn't something that equity owners have to wait for a crisis to see. This is something they're reaping in the here and now.

What is the key "too big to fail" benefit? It's the fact that shareholders aren't the biggest beneficiary at all in times of crisis. Bondholders are.

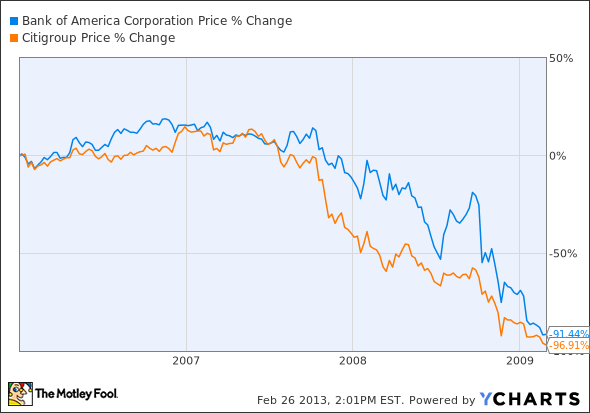

As the financial crisis hit its high pitch, the "too big to fail" promise was little more than cold comfort for shareholders of the two hardest-hit banks, Citi and B of A.

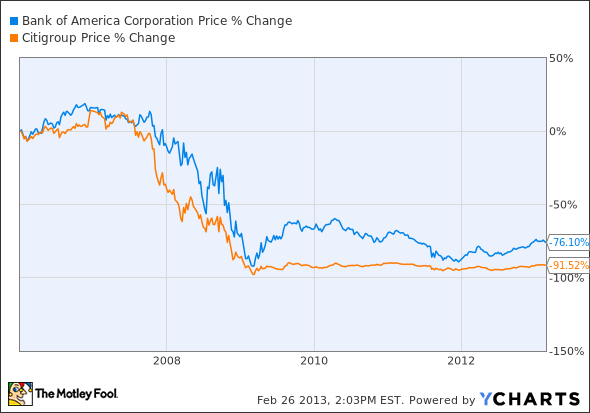

Even if we extend that out to today, it doesn't look a whole lot better. Stock investors that owned prior to the financial crisis have been taken to the cleaners.

On the other hand, the fact that these banks did not, in fact, fail outright, meant that bondholders were paid back. In full.

That had serious implications at the time, and with TBTF still with us today, it has serious implications still. If, as a bond investor, you can be pretty darn sure that when things get hairy, the government will step in and backstop the bank you've lent money to, you can feel a lot more comfortable lending to that bank. You can also lend to that bank more cheaply -- since you can justify a lower return because of a reduced risk of loss.

For the bank itself -- and, of course, its shareholders -- that means cheaper capital, which means more profit. And I'm sure I don't need to belabor the idea that more profit is good.

Of course, we don't want to get carried away about how much banks are reaping from this. While there seems little reason to believe that TBTF is going to disappear any time soon, it'd be folly to think that it's a lock into eternity. So banks aren't getting the full theoretical borrowing discount that they would if TBTF's future was guaranteed. At the same time, while low debt-market borrowing is all well and good, low-to-no cost deposits are even cheaper -- and many banks have been turning increasingly to deposits to salvage their spreads.

The question of whether it's wise to have a banking system dominated by banks considered "too big to fail" is a worthy debate to continue having. And you'll find me far more disposed to the idea of capping the size of banks. But we don't live in a theoretical world where there are no TBTF banks. We live in the U.S. of right now, complete with at least four of these hulking institutions.

And for investors, with that four-letter label comes another reason to be bullish.

One TBTF for your radar...

Bank of America's stock doubled in 2012. Is there more yet to come? With significant challenges still ahead, it's critical to have a solid understanding of this megabank before adding it to your portfolio. In The Motley Fool's premium research report on B of A, analysts Anand Chokkavelu, CFA, and Matt Koppenheffer, Financials bureau chief, lift the veil on the bank's operations, including three reasons to buy and three reasons to sell. Click here now to claim your copy, and as an added bonus, you'll receive a full year of FREE updates and expert guidance as key news breaks.

The article 1 Key Reason Big-Bank Investors Should Love "Too Big to Fail" originally appeared on Fool.com.

Matt Koppenheffer owns shares of Bank of America and Morgan Stanley. The Motley Fool recommends Goldman Sachs and Wells Fargo. The Motley Fool owns shares of Bank of America, Citigroup, JPMorgan Chase, and Wells Fargo. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.