The Natural Gas Game Has Changed

"It has to go up."

If you are an investor in the natural gas space, you have probably said these words to yourself more than once, thinking about the price of natural gas. There are several logical arguments that would justify such a statement. Unfortunately, it looks like some of those arguments are being thrown out the window.

Natural gas is in unprecedented territory, and here's why.

Apparently, not all BTUs are created equal

Generally speaking, the value of both oil and gas are based on their energy potential. When we burn these type of fuels, they emit a certain amount of energy, which is measured in British Thermal Units, or BTUs. In a similar way to how the amount of alcohol in a can of beer is different then if that can was full of whiskey, the amount of energy in the standard measure of oil is greater than the standard measure of natural gas. The standard ratio is that one barrel of oil is equal to about 6,000 cubic feet of natural gas. This is known as the BOE equivalent rate.

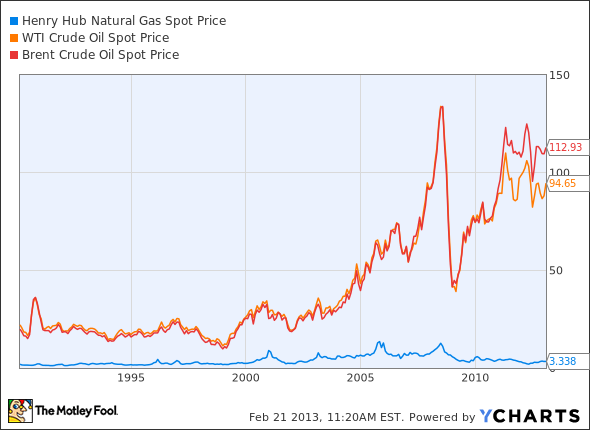

If the energy density of oil is about six times greater, then the BOE equivalent rate should be about 6:1, right? For years, this trend had generally held true:

Henry Hub Natural Gas Spot Price data by YCharts

Thanks to new drilling technology, though, U.S. gas production took off. All of a sudden, the country was producing gas at such a rapid pace, the market could not keep up with the supply. This has sent gas prices tumbling all the way to decade lows, and the BOE equivalent rate went way out of sync. With prices low and natural gas E&P companies struggling, some value investors saw this as an opportunity to gobble up some deeply discounted companies under the premise that natural gas prices would return to the BOE equivalent rate. Heck, even I made a case for it.

Those who have held onto the BOE equivalent rate are in for a bit of bad news. During Devon Energy's recent conference call, Devon CEO John Richels said that he believes that you can no longer use that rate as a fair assessment for natural gas prices:

Given the sustained divergence in the value of oil and natural gas, it's become pretty obvious to just about everyone that the energy equivalent BOE conversion rate of 6:1 has been rendered meaningless from an economic perspective. Based on the current price realizations of our oil and gas mix, a value or price equivalent is a much more meaningful way to evaluate growth in the value of a hydrocarbon stream.

So much for BOE parity. In retrospect, this should be a little less of a surprise. Several big natural gas players such as Chesapeake Energy and Linn Energy have spent much of the past few quarters reducing their exposure to natural gas, and more to oil. Chesapeake has done a rather commendable job of increasing liquids production by 41,000 barrels per day, and Linn has done what it does best ... buy things. It just recently announced the acquisition of Berry Petroleum, which has a 75% oil portfolio.

Don't hate the game, pick new players

If we have to throw out the BOE parity price, than what should we use instead. According to Mr. Richels, Devon expects to use an oil to natural gas price ratio of 20:1 for its guidance. Even based on current price parity, that would involve either a significant dip in oil prices, or a surge in natural gas prices to the $5.00 range. This may still be hopeful thinking, considering that, during Ultra Petroleum's conference call, CEO Michael Watford stated that the ramping down of U.S. natural gas production may take all of 2013 before any real impact on price would take place.

If this is what we can expect from the natural gas space, then the best candidates to perform well in these conditions is natural gas users. Sustained low gas prices will help to push the door open even further for companies like Westport Innovations and Clean Energy Fuels , which look to turn natural gas into a viable transportation fuel. With major U.S. Trucking firms taking a hard look at converting truck fleets, Westport will be the go-to company for engines, and Clean Energy Fuels will have one of the most complete natural gas fueling station networks in the country.

What a Fool Believes

Great investors have two great traits: 1) they maintain poise when others panic, and 2) they are willing to reconsider an investment when the market dynamics change. When a major company like Devon starts to think of natural gas in a different way, then investors should do the same, as well.

Westport has taken on a great challenge: make natural gas a viable transportation fuel in the face of gasoline. This David and Golaith story has caught the attention of investors, and the expectations for this company have steadily risen. To help you determine whether Westport Innovations can meet these lofty expectations, The Motley Fool has just released a brand-new premium report breaking down the company's opportunities, competitive advantages, and risks. To get started, simply click here now for instant access.

The article The Natural Gas Game Has Changed originally appeared on Fool.com.

Fool contributor Tyler Crowe owns shares of Westport Innovations and Linn Energy, LLC. You can follow him on Fool.com under TMFDirtyBird, Google +, or Twitter: @TylerCroweFool.

The Motley Fool recommends Clean Energy Fuels, Ultra Petroleum, and Westport Innovations. The Motley Fool owns shares of Devon Energy, Ultra Petroleum, and Westport Innovations and has the following options: Long Jan 2014 $20 Calls on Chesapeake Energy, Long Jan 2014 $30 Calls on Chesapeake Energy, Short Jan 2014 $15 Puts on Chesapeake Energy, Long Jan 2014 $30 Calls on Ultra Petroleum, Long Jan 2014 $40 Calls on Ultra Petroleum, and Long Jan 2014 $50 Calls on Ultra Petroleum. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.