Is UPS Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what United Parcel Service's recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell UPS's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much UPS's free cash flow has grown in comparison with its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If UPS's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

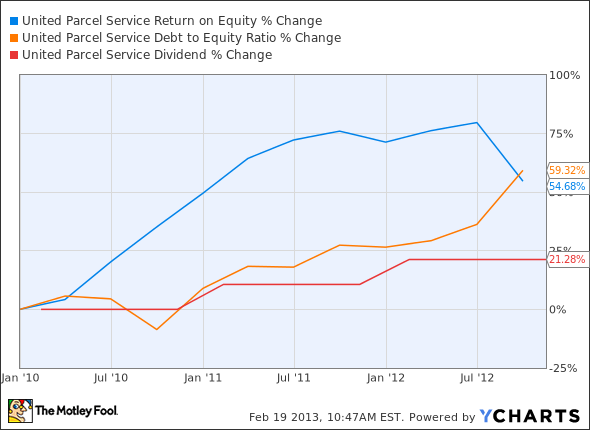

Is UPS managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

Healthy dividends are always welcome, so we'll also make sure that UPS's dividend payouts are increasing, but at a level that can be sustained by its free cash flow.

By the numbers

Now, let's take a look at UPS's key statistics:

UPS Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 19.5% | Fail |

Improving profit margin | (359.1%) | Fail |

Free cash flow growth > Net income growth | (100%) vs. (59%) | Fail |

Improving EPS | (59.2%) | Fail |

Stock growth (+ 15%) < EPS growth | 59.1% vs. (59.2%) | Fail |

Source: YCharts.

*Period begins at end of Q4 2009.

UPS Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 54.7% | Pass |

Declining debt to equity | 59.3% | Fail |

Dividend growth > 25% | 21.3% | Fail |

Free cash flow payout ratio < 50% | 43.5% | Pass |

Source: YCharts.

*Period begins at end of Q4 2009.

How we got here and where we're going

UPS doesn't do much to impress today, with a measly two out of nine possible passing grades. Still, many of our Foolish analysts remain at least somewhat optimistic. Let's look at why this poor performance might not be indicative of UPS's potential, and how it might recover from what seems to be a momentary weakness.

UPS's big drop in its latest quarter was the result of a multibillion-dollar writeoff for pension obligations. Forbes reports UPS's normalized P/E, which discounts such one-time effects, at 24.1, slightly above its two-year average of 19.4, but still far more reasonable than the currently inflated result. With FedEx sporting a P/E of just 17.2, it looks as if UPS might be a little bit overheated. On the other hand, UPS's operating margin handily beat FedEx's for the 2012 fiscal year, and average daily package volume increased by half a million packages for its fourth quarter. Despite its iffy earnings, UPS has remained committed to returning cash to shareholders. A 9% dividend increase, while not reflected in our current results, will kick in with the company's next payout. The company will also be spending more on share buybacks following its failed acquisition attempt of European shipper TNT Express.

Another factor that might work in UPS's (and FedEx's, for that matter) favor is the U.S. Post Office's shutdown of Saturday deliveries. While the shutdown currently doesn't include packages, it does indicate that the Post Office is having a difficult time maintaining positive cash flow in the face of private competition. Amazon.com and eBay , two of UPS's most important shipping partners, both saw annual revenue grow more than 20% year over year for 2012. That's a lot more deliveries to make, and a bit less competition to face to do so. And at $10 billion more in annual revenue than FedEx, UPS remains in a better position to expand once its temporary financial woes are behind it.

Putting the pieces together

Today, UPS has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

The Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock it is in the brand-new free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

Keep track of UPS by adding it to your free stock Watchlist.

The article Is UPS Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter, @TMFBiggles, for more insight into markets, history, and technology.The Motley Fool recommends Amazon.com, eBay, FedEx, and UPS and owns shares of Amazon.com and eBay. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.