Is ABB Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what ABB's recent results tell us about its potential for future gains.

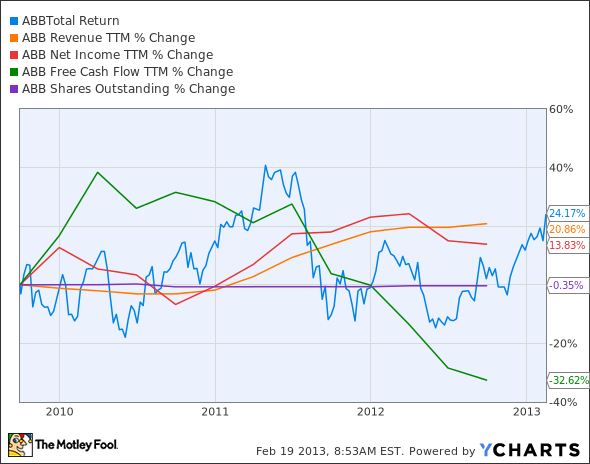

What the numbers tell you

The graphs you're about to see tell ABB's story, and we'll be grading the quality of that story in several ways.

Growth is important on both the top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much ABB's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If ABB's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is ABB managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

Healthy dividends are always welcome, so we'll also make sure that ABB's dividend payouts are increasing, but at a level that can be sustained by its free cash flow.

By the numbers

Now, let's look at ABB's key statistics:

ABB Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 20.9% | Fail |

Improving profit margin | (40.4%) | Fail |

Free cash flow growth > Net income growth | (32.6%) vs. 13.8% | Fail |

Improving EPS | 11.3% | Pass |

Stock growth (+ 15%) < EPS growth | 24.2% vs. 11.3% | Pass |

Source: YCharts.

*Period begins at end of Q3 2009.

ABB Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | (14.3%) | Fail |

Declining debt to equity | 202.7% | Fail |

Dividend growth > 25% | 45.2% | Pass |

Free cash flow payout ratio < 50% | 97.8% | Fail |

Source: YCharts.

*Period begins at end of Q3 2009.

How we got here and where we're going

ABB earns an underwhelming three out of nine possible passing grades. It hasn't been a particularly strong three years for ABB, with declining margins, shrinking free cash flow, rising debt, and a dangerously high free cash flow payout ratio. Its stock price growth, while respectable, is only about half that of the S&P 500 during the same period. So what will it take for ABB to recover and turn some of these failing grades around?

Operating in a wide range of industrial segments certainly helps, but only if those segments provide the right opportunities. Two such segments have been recently highlighted here at the Fool are the smart grid, specifically distribution automation, or DA, and terminal automation. ABB is big on automation, and it's no surprise that it's been buying its way into new automation opportunities, including a very recent acquisition of optical character recognition company APS Technology. This acquisitive binge can easily explain a large part of ABB's cash-flow decline, as the company spent only $193 million on buyouts in 2009 but also spent $1.2 billion in 2010 and $4 billion in 2011. Of course, it's far from alone -- Siemens and General Electric are both highly active in the DA space, and both are significantly larger. GE, in particular, has put significant resources into developing its industrial Internet project, which could give it a competitive leg up in the space.

Another area of interest is ABB's industrial robotics segment, which ties in optimally with the rest of its automation portfolio. However, in terms of robotics investments, the two most notable entrants -- iRobot and Intuitive Surgical -- have not only far outperformed ABB's three-year return, but they've also done much better at this greatness tracker. Both iRobot and Intuitive earned six out of seven passing grades, seven being the maximum possible score for a non-dividend stock. Although ABB's dividend makes it more appealing to value investors, its high cash flow payout ratio is worrisome. ABB may need to reduce the payout, add more debt, or cut back on its buying spree to keep paying out.

Putting the pieces together

Today, ABB has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

For GE, the recent financial crisis struck a blow, but management took advantage of the market's dip to make strategic bets in energy. If you're a GE investor, you need to understand how these bets could drive this company to become the world's infrastructure leader. At the same time, you need to be aware of the threats to GE's portfolio. To help, we're offering comprehensive coverage for investors in a premium report on General Electric, in which our industrials analyst breaks down GE's multiple businesses. You'll find reasons to buy or sell GE, and you'll receive continuing updates as major events unfold during the year. To get started, click here now.

Keep track of ABB by adding it to your free stock Watchlist.

The article Is ABB Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter, @TMFBiggles, for more insight into markets, history, and technology.The Motley Fool recommends Intuitive Surgical and iRobot and owns shares of General Electric Company and Intuitive Surgical. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.