Midstream Spinoffs Aren't for Everyone

Despite production volume records and beating analyst expectations for five straight quarters, Occidental Petroleum sure hasn't seen a lot of love lately from investors. With so many other companies in the integrated oil and gas space making big moves to spin off their midstream and refining operations, perhaps investors are waiting for a similar shakeup to unlock shareholder value.

In the company's most recent conference call, Occidental CEO Stephen Chazen was asked if management was considering a similar option. While he said that they have considered the idea, they do not believe it is the best path for the company. Let's take a look why this is the case.

Bucking the spinoff trend

Of all the news that has come out of the oil and gas space in the past couple of years, the performance of some integrated oil and gas players has been some of the most discouraging.

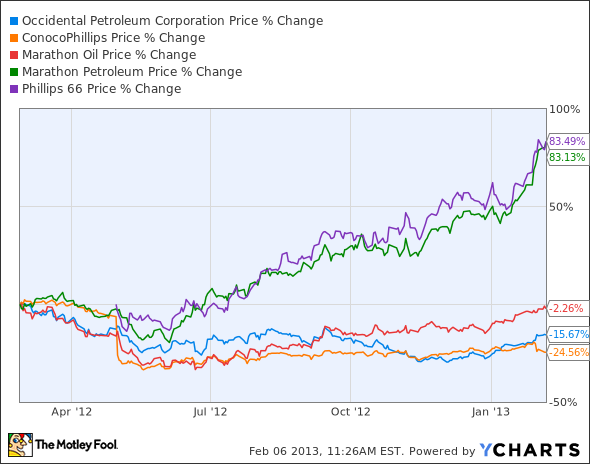

This chart needs to be put in context, though. In the past two years, both Marathon Oil and ConocoPhillips have spun off their midstream and refining operations. The big shifts in share price for the two companies (July 1, 2001 for Marathon; April 1, 2012 for ConocoPhillips), coincide with the dates of their spinoffs. Not only have these moves allowed the two companies to focus their capital programs on exploration and production, but they have also unlocked lots of shareholder value.

Since Phillips 66's IPO back in April of last year, both it and Marathon Petroleum have been two of the best-performing stocks in the market. This is in large part thanks to one of the most advantageous markets for refining in the past decade. With crack spreads for mid-continent refiners reaching as high as $25, some might consider this a golden age of refining.

Just like the parent companies have been able to focus their efforts on their core business, so too have these new spinoffs. In order to maximize crack spreads across all of its refineries in the U.S., Phillips 66 has invested in over 2000 rail cars to deliver cheaper Bakken crude to its East and West Coast refineries. Likewise, Marathon Petroleum has plans also to ship Bakken and Canadian oil sands via pipeline to its facilities as well as develop its capacity in the Ohio region to process natural gas liquids from the Utica formation.

So why won't Occidental join the spinoff party and see if its refining assets can give investors something to smile about? According to Chazen, its midstream and pipeline assets are too concentrated in the Permian Basin to make a difference for investors. Here is why that makes sense.

Of the 15 oil and gas processing facilities the company operates, 13 of them are located in West Texas and New Mexico, the center of the Permian Basin. The company also owns 2,700 miles of pipeline in the basin and large CO2 source fields for enhanced oil recovery. This represents the bulk of the company's midstream and refining operations. These assets, plus its other midstream and chemical operations in the U.S. and abroad, only represented 10% of the company's earnings for the quarter, not including asset imparements. In the case of Phillips 66 and Marathon Petroleum, these two companies have a much more geographically diverse portfolio that allows them to take advantage of price differentials throughout the country. This just simply not possible for Occidental's assets.

Also, we need to consider the exploration and production, or E&P, end of Occidental Petroleum's operations. Occidental produces more oil and gas in the Permian than the next three largest producers (Kinder Morgan, Apache, and Pioneer Natural Resources) combined. Even if these assets were to be spun off into their own entity, it is very likely that it would still be receiving feedstock from Occidental itself. With a large concentration of production, transportation, and refining capabilities concentrated in this one area, the company is able to deliver much greater value for its Permian assets than many of its competitors in the region.

What a Fool believes

Overall, Chazen probably has it right. For the time being, the potential gain for shareholders just doesn't seem to be there in comparison to some of the other spinoffs we have seen in the past couple years. It would also lower the company's competitive advantage in one of the more productive oil basins in the U.S.

With over 90% of the company's earnings coming from exploration and production, its almost more apt to consider the company a pure E&P play rather than a completely integrated oil and gas company. This isn't the best place to be right now. Since the U.S. energy infrastructure is still behind domestic production, places like the Permian are not getting top dollar for product. This could really hurt Occidental's margins, so it will need to rely on production increases to grow earnings.

One midstream company that could help alleviate some upstream pressures

The surge in oil and natural gas production from hydraulic fracturing and horizontal drilling is creating massive bottlenecks in takeaway capacity. However, this problem for producers creates a massive and immensely profitable opportunity for midstream companies. Energy Transfer Partners helps alleviate the gluts in supply with 23,500 miles of transformational pipelines. To see if ETP and its industry-leading yield will be a fit for you, click on this detailed premium report, which will supply you with a thorough analysis of this midstream.

The article Midstream Spinoffs Aren't for Everyone originally appeared on Fool.com.

Fool contributor Tyler Crowe has no position in any stocks mentioned.You can follow him on Fool.com under TMFDirtyBird, Google +, or Twitter: @TylerCroweFool. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.