Falling Revenue? Who Cares!

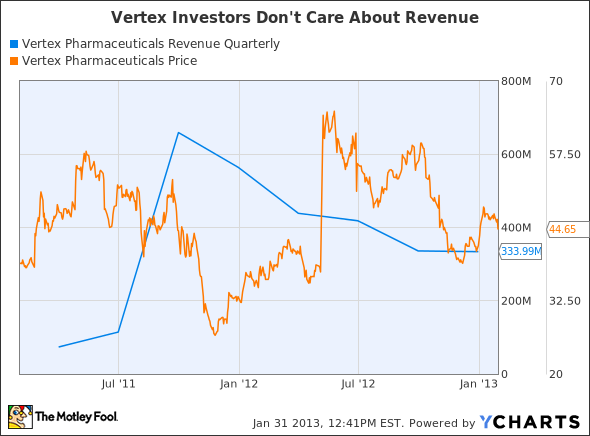

Vertex Pharmaceuticals' revenue peaked in the third quarter of 2011 at $659 million. Since then, revenue from Incivek has slowly fallen as patients have decided to wait for other hepatitis-C drugs, and the company's cystic fibrosis drug, Kalydeco, hasn't been able to make up the difference.

Investors could care less. There's no correlation between revenue and stock price.

VRTX Revenue Quarterly data by YCharts.

This year, sales of Incivek in Europe -- where Johnson & Johnson sells the drug under the brand name Incivo -- are expected to increase, because there's less warehousing of patients for new treatments in Europe. Sales of Kalydeco will also ramp up in 2013 as Vertex launches the drug in additional countries. Neither will make up for declining sales of Incivek where Vertex books sales, which will fall below the magic $1 billion this year. Vertex is guiding for 2013 revenue between $1.10 billion to $1.25 billion, which is below the fourth-quarter run rate of $1.34 billion.

Investors have shrugged off Vertex's falling revenue because of its potential. To expand its hold on the cystic fibrosis market, the company is testing Kalydeco in combination with a newer drug VX-809, which Vertex hopes will help a larger number of cystic fibrosis patients. The company expects to begin a phase 3 program this quarter, putting data a ways away.

Vertex also has some second-generation hepatitis-C drugs. There's no way it beats Gilead Sciences or AbbVie to the market; both have all-oral combinations that are in phase 3 development already. Both cocktails are expected to post cure rates in the 95% to 100% range, so beating them on efficacy will be difficult. And once you get in that range, the difference isn't that meaningful anyway. To compete, the all-oral combinations Vertex is working on with Johnson & Johnson and GlaxoSmithKline will have to be safer and/or work quicker to grab some sales in the tail end of the hepatitis-C epidemic.

If you're going to own Vertex at this point, you've got to have patience. It's going to be years before we see revenue as high as they were right after the launch of Incivek.

If you don't have the patience to see it through, Vertex might be more appropriate for your watchlist at this point. The Fool does have a suggestion for a stock you can buy right now, though. It's our top pick for 2013, and you can find out why in this free report. Grab your copy by clicking here.

The article Falling Revenue? Who Cares! originally appeared on Fool.com.

Fool contributor Brian Orelli, Ph.D. has no position in any stocks mentioned. The Motley Fool recommends Gilead Sciences, Johnson & Johnson, and Vertex Pharmaceuticals. The Motley Fool owns shares of Johnson & Johnson. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.