NextEra Earnings Report: Can a Tiny Dividend Pull Big Profit?

NextEra Energy reported earnings Tuesday, beating income estimates, but falling short of sales expectations . With top line numbers dwindling, investors are wondering whether NextEra's growth days are behind it. Let's take a look at this quarter's results and see if this utility can keep up its market-beating returns .

Number crunching

For Q4 2012, NextEra's revenue fell 12.6%, to 3.38 billion, compared to Q4 2011. Not only does this slump bode badly for the corporation's growth prospects, but it failed to meet analyst's estimates of $4.6 billion in sales .

Net income fell 35% from last year's Q4, clocking in at $433 million. Both revenue and sales came in lower than Q2's results .

Despite the seemingly lackluster numbers, NextEra delivered where it matters the most: earnings per share. Diluted EPS for this quarter came in at $1.03, beating analysts' $0.95 estimate by 8.4%.

For Q3 2012, NextEra missed on sales and EPS estimates , but CEO Jim Robo stressed at the time that he expected Q4 results to deliver. For earnings, at least, Robo was right.

Digging deeper

NextEra is comprised of two separate companies: regulated utility company Florida Power & Light (FPL), and unregulated North American electricity wholesaler NextEra Energy Resources (NEER ).

FPL's Q4 and overall 2012 showed significant improvement over last year's numbers. Its Q4 EPS clocked in at $0.61, 20% more than Q4 2011's $0.51. Likewise, full year EPS bumped up 16%, to $2.96 . NextEra celebrated a regulatory win in January, when the Florida Public Service Commission approved a 10.5% return-on-equity midpoint rate increase .

NEER, the ugly duckling of the two subsidies, felt GAAP earnings squeezed for Q4 and 2012. Fourth quarter EPS fell 57%, to $0.41, while 2012 results came in 12% lower at $1.84 .

NextEra for the win?

The world of utilities is changing fast, and shares of these corporations are no longer the stalwart dividend income earners they were in the past. Big changes are hitting utilities, and management decisions will make or break companies in the next few years.

NextEra offers a unique mix of growth and value, due to its heavy investments in renewable energy. Its 3.3% dividend yield is weak in comparison to most other utilities, but its cash flow puts it in a better spot than many competitors to sustainably return value to shareholders:

Atlantic Power | 9.6% | (54%) |

Exelon | 7.1% | 123% |

First Energy | 5.3% | (1,770%) |

Duke Energy | 4.7% | (252%) |

Southern Company | 4.5% | 855% |

Consolidated Edison | 4.3% | 163% |

Dominion Resources | 4.1% | (1,769%) |

National Grid | 4% | 163% |

NextEra Energy | 3.3% | (27%) |

Source: YCharts and Yahoo! Finance; TTM = trailing 12 months

Looking beyond the numbers, a bet on NextEra is a bet on renewables. The company is the largest producer of renewable energy in the U.S., and focuses especially on wind power.

In the past year, NextEra added another 1,500 MW of wind to its energy portfolio, to pass the 10,000th MW mark in December . It continued its nuclear modernization and uprate projects , and has applied to construct a third natural gas pipeline to serve its Florida customers .

From a policy standpoint, the company pulled in two big wins in 2012. Congress' fiscal cliff deal included a last-minute renewal of a wind production tax credit, and a current bill could give wind-producing companies many of the same tax perks currently available to oil and gas companies.

The most important metric

NextEra's sales have fallen 13% in the last five years, and this most recent quarter's results continue the company's downward trend . Traditionally, top line growth was the most important metric for utilities, but investors shouldn't expect stellar sales growth from any utilities in the near future.

A new report by the Department of Energy estimates 0.58% compound annual growth in electricity rates over the next decade. While this is due in part to a slower economy, $9.5 billion of energy efficiency programs are helping to cut consumption .

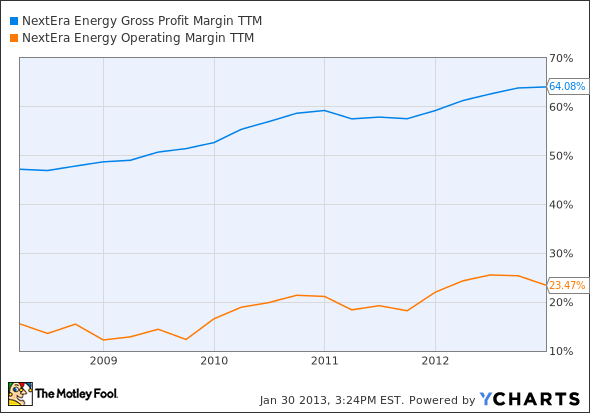

What this means for investors is that, contrary to the past, bottom line metrics will become increasingly important in the years ahead. Although NextEra's sales have slumped, its EPS wins continue to bolster my faith in this utility. Likewise, the company's margins are some of the best around, with a 64% gross profit margin and a 23% operating margin.

NEE Gross Profit Margin TTM data by YCharts

Looking ahead, NextEra expects 2013 earnings to hit $4.70-$5.00 per share, and 2014 EPS in the $5.05-$5.65 range . I think it'll deliver, and have made an outperform call on NextEra on my Motley Fool CAPS page. Booming sales or not, NextEra's got a promising future.

Exelon's margins are as small as its market returns in recent years, but contrarian investors are eyeing Exelon's turnaround. As the nation moves increasingly toward clean energy, the utility is perfectly positioned to capitalize on having the largest nuclear fleet in North America. Combine this strength with an increased focus on renewable energy, and EXC's recent merger with Constellation places Exelon and its best-in-class dividend on a short list of top utilities. To determine if Exelon is a good long-term fit for your portfolio, you're invited to check out The Motley Fool's premium research report on the company. Simply click here now for instant access.

The article NextEra Earnings Report: Can a Tiny Dividend Pull Big Profit? originally appeared on Fool.com.

Fool contributor Justin Loiseau has no position in any stocks mentioned, but he does use electricity. You can follow him on Twitter, @TMFJLo, and on Motley Fool CAPS, @TMFJLo.The Motley Fool recommends Exelon and National Grid plc (ADR). Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.