Will This Buyback Trend Change?

Share buybacks are often looked at as a disastrous decision. One reason for this might be that the most attention goes to negative stories of a company destroying shareholder value, while the well-managed buybacks fail to earn a headline. Wasting money, after all, is more poignant than returning value over time.

However, many insurance companies have done a fantastic job at buying their own shares for cheap. But, now that their share prices are gaining ground, what's in the future?

Let's take a look at past purchases and see what plans insurers have.

Halving share count

A quick look at this chart demonstrates the drastic reduction in shares outstanding:

TRV Shares Outstanding data by YCharts.

From 2006 to today, insurance giant Travelers has reduced its share count by more than 45%. This means that if everything else, like earnings and the P/E ratio, remained the same, one share would've increased in value through nothing but the buybacks.

Many argue that they would rather have a company give a dividend than waste through purchasing its own shares, but Travelers also pays a dividend, which currently yields about 2.4%. And this dividend has grown about 9% per year over the past five years.

It also helps the positive buyback story that Travelers shares now sit at their highest price since 2006, now at $77 per share compared to 2006's beginning price of $47 per share.

In the future, Travelers still has $2.1 billion authorized for more share repurchases after it spent $1.45 billion in 2012. At today's price, that's another 27 million shares that could be bought, leaving shares outstanding at 354 million, or 7% lower than today. Of course, if Travelers has to weather another superstorm like Hurricane Sandy, it may delay continued buybacks. This type of prudent thinking, however, keeps Travelers solvent and its core business safe.

Other share repurchasing

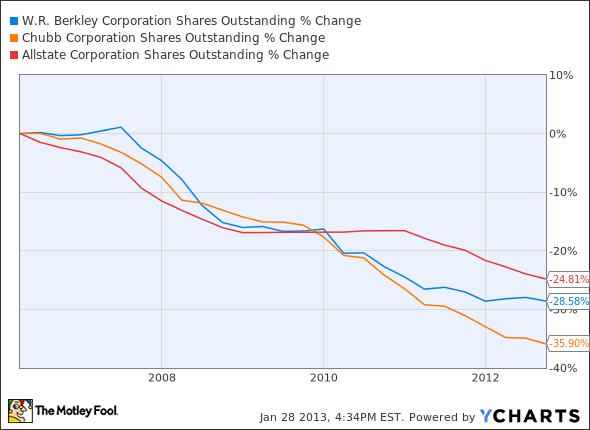

Other insurers have also cut share counts as they search for higher returns while interest rates stay low. While not as drastic as Travelers' 45% cut, W.R. Berkley , Chubb , and Allstate all drove shares outstanding down at least 25%:

WRB Shares Outstanding data by YCharts.

Not every company above had the same timing on their repurchases as Travelers had, particularly Allstate. Allstate's $1.3 billion in purchases in 2007 at an average price of $53.13 per share look like a poor investment now that the stock is near $43 per share. This demonstrates the need to judge management as well as the business. For example, the discord among managers and employees was evident when the president of the National Association of Professional Allstate Agents said in 2011, "no one at the top of the company understands what it's like to be an agent." Even top executives demonstrated the companies internal issues when the president of Allstate's home and auto insurance groups was let go in 2011 after reportedly combining the CEO's name and some choice expletives.

Future buybacks

With many of the insurers near 52-week highs, the positive returns from buybacks due to undervalued stocks may not be so easy to achieve. Even so, Allstate recently approved another $1 billion in stock buybacks, W.R. Berkley increased its buyback program by 10 million shares in August, and Chubb expects to announce a new buyback program by the end of January.

So, it looks like insurers are bent on buying more of their own shares. But any plans do not need to be followed through, especially if there is a catastrophic event that hinders available funds.

Also, as these companies become fairly valued, they may alter strategies to find better returns, as Deloitte explains in its 2013 outlook:

Insurers will likely become more aggressive in their quest for higher yields by exploring or increasing investments in various alternative asset classes such as real estate, private equity, developing-country stocks and bonds, hedge funds, commodities, and oil and gas assets. In addition to higher yields, some alternative investments can provide an additional hedge to insurers against low interest rates, due to their negative correlation with traditional investments.

It may be difficult to think that insurance would mix with riskier bets like commodities and hedge funds, but while low interest rates depress traditional returns and stock valuations for buybacks begin to be deemed too rich, there may be few places to find higher returns. Reinsurance has already headed in this direction, but as The New York Times writes, "the reinsurance market is starting to look like many of the markets before the financial crisis -- lightly regulated and interconnected in ways that policy makers can't see, with banks potentially left with the wreckage."

Of course, if anyone knows risks, it's an insurance company. And maybe that's why they'll stick with buying their own shares.

If you're looking for some long-term investing ideas, let me invite you to read the Fool's brand-new special report: "The 3 Dow Stocks Dividend Investors Need." It's absolutely free, so just click here and get your copy today.

The article Will This Buyback Trend Change? originally appeared on Fool.com.

Fool contributor Dan Newman has no position in any stocks mentioned. The Motley Fool owns shares of W.R. Berkley. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.