Gaming Stocks Are Too Hot to Handle

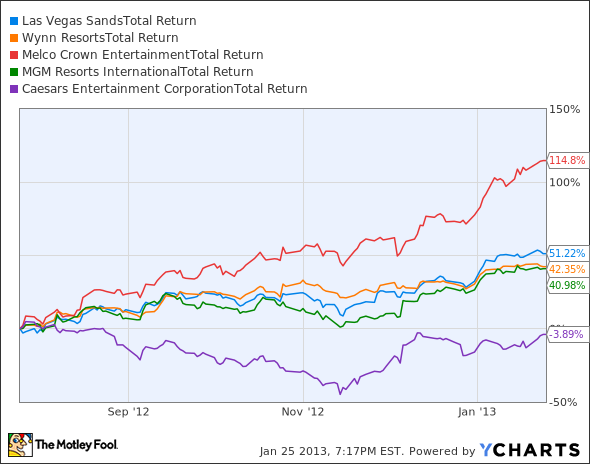

Over the past six months, gaming stocks have had an incredible run. Melco Crown has more than doubled while Wynn Resorts , Las Vegas Sands , and MGM Resorts are all up around 50%.

LVS Total Return Price data by YCharts.

But these huge gains come at a time when gaming growth both in the U.S. and in Macau is growing far slower than the stock prices are growing. So, are gaming stocks too hot to handle?

Value matters

It's relatively easy to look at a gaming company's value by looking at past results, because expansion has slowed from a torrid pace over the last decade. The best way to value gaming companies is by taking the company's enterprise value (market cap plus debt, minus cash) and dividing it by EBITDA, which is an approximation of cash flow. This strips out depreciation and interest payments, which aren't operating expenses and are a factor of money spent and capital structure, respectively.

Below I have laid out the enterprise value/EBITDA of each of the five biggest U.S.-traded gaming companies by revenue and the numbers that go into the ratio.

Company | Market Cap | Net Debt | EBITDA (TTM) | EV/EBITDA |

|---|---|---|---|---|

Las Vegas Sands | $43.3 billion | $8.0 billion | $4.6 billion | 11.27 |

Wynn Resorts | $12.4 billion | $3.9 billion | $1.6 billion | 10.28 |

Melco Crown | $11.2 billion | $996 million | $904.3 million | 13.48 |

MGM Resorts | $6.4 billion | $11.6 billion | $1.7 billion | 10.74 |

Caesars Entertainment | $1.0 Billibillionn | $18.8 billion | $2.0 billion | 9.81 |

Source: Yahoo! Finance and company filings. TTM = trailing 12 months.

What you'll see is that every stock besides Caesars Entertainment has a ratio above 10. But I'll throw out Caesars as a buying option because the company has 18.8 times the debt as it does market equity, and it operates in worse markets than every other company. This makes it an extremely high-risk investment. MGM is in a similar situation and unless you are looking for leveraged growth in Las Vegas, this is a high-risk stock as well.

Melco Crown has the highest ratio above, but the stock has run so far, so fast that I think it's gotten well ahead of itself. Macau gaming revenue grew at just 13.5% last year, down from 57.8% in 2010 and 42.2% in 2011, so the company's organic casino growth will slow. As gaming investors, we need to know when we're buying value and when stocks are overpriced. In 2011, when Melco Crown traded at an 8.19 EV/EBITDA multiple and Macau was growing more quickly, I thought it was the best stock in gaming. Now, it's simply too expensive to touch.

Las Vegas Sands and Wynn Resorts are in similar territory, although I'm not panic-selling at the current valuations; I just wouldn't be a buyer here.

Growth and multiple analysis

Half the battle with gaming stocks is buying at an attractive valuation. In general, I don't like to buy gaming stocks with an EV/EBITDA ratio more than 9 unless there are major growth avenues in the near future. Patient investors can wait for these opportunities and pounce, avoiding overpaying for gaming stocks.

The link above shows that Melco Crown traded at a multiple well below 9 just over a year ago. Wynn Resorts was at 9.6 at the same time and Las Vegas Sands was 11.5 just before opening a huge new casino in Macau. Growth and more attractive multiples made that a great time to buy gaming stocks.

Today, Las Vegas Sands and Wynn are both years away from opening their next resorts in Macau and Melco Crown only has part ownership of a Philippines property and another resort on Cotai (currently without table games). This distant growth doesn't merit paying a premium for any of these stocks right now, especially considering the slowing growth in Macau.

A deeper look at Melco Crown

Melco Crown is often a forgotten company in gaming, but it has tremendous upside from Studio City and its partnership in the Philippines, which could more than double the company's revenue base. This being a more speculative investment, is it worth the risk for smaller investors? The Motley Fool answers this question and more in our most in-depth Melco Crown research available for smart investors like you. Thousands have already claimed their own premium ticker coverage, and you can gain instant access to your own by clicking here now.

The article Gaming Stocks Are Too Hot to Handle originally appeared on Fool.com.

Fool contributor Travis Hoium manages an account that owns shares of Wynn Resorts, Limited. You can follow Travis on Twitter at @FlushDrawFool, check out his personal stock holdings, or follow his CAPS picks at TMFFlushDraw. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.