Under Armour or Lululemon in 2013?

As we settle into the new year, the question on most investors' minds is what stocks will dominate in 2013. Health and fitness trends are getting a lot of attention these days as consumers set their resolutions for the year ahead. There are also lucrative opportunities for investors in this space. In fact, the global athletic apparel industry is set to reach $125 billion by 2017.

It's in this spirit that we'll look at Under Armour and lululemon athletica -- two key players in the sportswear industry today. Let's check out what these companies have planned for the future, and which stock investors should own in 2013.

Lululemon

The yoga-inspired apparel company got off to a rough start this year, with the stock sliding into a downward dog position earlier this month. The sell-off came on the heels of revised guidance from the company for its fiscal fourth quarter. Shares are currently down more than 12% year to date. However, the stock should rebound later this year as Lululemon's growth initiatives start to play out.

Consider this: Lululemon is currently the highest-productivity apparel retailer in North America, with $2,050 in sales per square foot. If the Canadian-based company can replicate this success overseas in markets such as Europe and Asia, it would tremendously boost Lululemon's profitability. The retailer now has distribution centers up and running in Europe, Asia, and Australia, in addition to its locations in the U.S. and Canada.

The company recently opened two showrooms in Hong Kong and one in London, with plans to add more locations in the quarters to come. Lululemon uses showrooms to interact with the local community before opening storefronts in those locations. These showrooms are part of Lululemon's grassroots approach to testing consumer demand in new markets -- a strategy that has worked well for the retailer in the U.S.

The high-end fitness brand plans to test its products in as many as 15 countries this year. As it stands, Lululemon operates 211 stores worldwide, 135 of which are located in the U.S. This is a very different distribution model from the company's competitors. such as Nike and Under Armour.

While Lululemon sells its merchandise in corporate-owned stores, more than 70% of Under Armour's products are sold via wholesale. The same goes for Nike. This means that both Under Armour and Nike rely on retailers such as Dick's Sporting Goods and Sports Authority to move their products. In fact, Forbes reports that a whopping 26% of Under Armour's sales come from Dick's and Sports Authority. This distribution model allows Under Armour and Nike to hit scale faster than Lululemon. However, on the other hand, by selling through its own stores, Lululemon keeps more of the profit from those sales than either Nike or Under Armour does from theirs. This is a trade-off that seems to be serving Lululemon well.

Lululemon's online sales are also contributing more toward the company's profitability. As my fellow Fool Jeremy Bowman pointed out, Lululemon was able to grow its e-commerce channel by 89% in the third quarter. Still, e-commerce penetration is only 14% of total sales, which means Lululemon has an opportunity, both in the U.S. and abroad, to capture more business online.

So we know that Lululemon will focus on building out its e-commerce business, as well as international growth, in 2013. For comparison, here are some of Under Armour's developments for the year ahead.

Under Armour

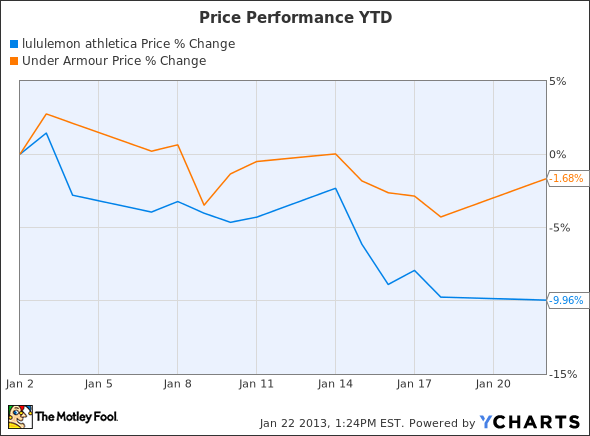

Lululemon and Under Armour are well matched from a valuation standpoint. Both companies have strong balance sheets with little or no debt, and each of the stocks trades at a P/E multiple above 40. However, as you can see in the chart below, Under Armour comes out ahead in terms of price performance year-to-date.

Data by YCharts.

This year is shaping up to be an important year for Under Armour's footwear division. The company has struggled in the past to gain traction in the athletic footwear business, where it faces tough competition from Nike. Sales of Under Armour's sneakers currently account for 12% of the company's revenue, which means there is more than enough room for improvement.

Finding growth in the athletic shoe market won't be easy for Under Armour, especially since it lacks much of the patented technology present in Nike products. From its branded cushioning technology "Nike Air" to its wildly successful Nike+ iPod Sport Kit, Nike is at the top of its game when it comes to shoe innovation. Nevertheless, the hope is that Under Armour will finally grab meaningful market share from Nike in this segment in 2013.

Similar to Lululemon, Under Armour plans to use international expansion as another way to fuel future growth. True, Under Armour already sells its products abroad in regions such as Europe and China. Yet these markets account for only 6% of Under Armour's total revenue, whereas about 94% of the company's revenue is generated in North America.

Unfortunately, Under Armour's distribution model makes it more difficult for the company to succeed overseas. The majority of Under Armour's sales come from its relationships with retailers such as Dick's, Sports Authority, and Foot Locker.

The problem, then, is that these sporting goods companies don't operate in Europe or Asia, which means Under Armour must instead work out licensing deals with local companies to sell its products. Given these hurdles, I suspect international growth will continue to be slow for Under Armour in the coming quarters.

What's in store?

So which of these sporty stocks will come out on top in 2013? Ultimately, I think Lululemon shows a more promising growth trajectory. Lululemon uses what it calls "community connectors" or company representatives to engage with the local communities in new markets. This word-of-mouth approach should work well for the company as it focuses more on global expansion in the year ahead.

More important, Lululemon has the potential to grow its sales by 10 times if it can penetrate its other markets like it has in Canada, but without question, the competitive landscape is starting to increase. Can Lululemon fight off larger retailers like Gap and Nordstrom, and ultimately deliver huge profits for savvy investors like yourself? The Motley Fool answers these questions and more in our most in-depth Lululemon research available for smart investors like you. Thousands have already claimed their own premium ticker coverage, and you can gain instant access to your own by clicking here now.

The article Under Armour or Lululemon in 2013? originally appeared on Fool.com.

Fool contributor Tamara Rutter owns shares of lululemon athletica. The Motley Fool recommends lululemon athletica, Nike, and Under Armour. The Motley Fool owns shares of Dick's Sporting Goods, Nike, and Under Armour. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.