Vale Is a Great Way to Profit From China's Growth

Despite the record cold in China, economic growth is heating up, thanks to the country's stimulus package and strengthening exports. If the Chinese business climate does improve, Brazilian industrial minerals and metals giant Vale could become even more attractive.

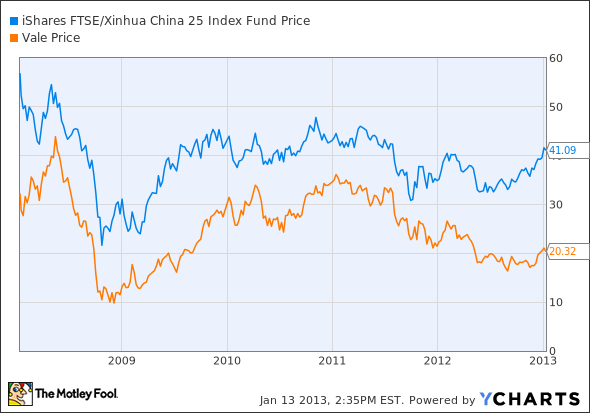

The biggest player in its sector

Even with the difficulties of doing business in Brazil, Vale, the world's largest iron ore entity, is up 14.80% for the last quarter, powered by China's improving economy. As with so many other companies in this sector, Vale needs a booming China; the People's Republic is the world's biggest customer for iron ore and other industrial minerals and metals. The chart below shows how the share price of Vale moves in a trajectory along with that of the exchange-traded fund for China, the iShares FTSE China Index (NYSE: FXI):

The $156 billion stimulus package China recently introduced focuses on infrastructure projects, which bode well for Vale and others in the industrial metal and minerals sector. As the table below shows, industrial metal and mineral companies such as Vale and Rio Tinto, and the shippers who carry assorted commodities, such as DryShips , Eagle Bulk Shipping , and Frontline , have done well.

Shippers in all sectors need for the Chinese economy to surge as it is the biggest consumer of commodities in the world. More demand from China will lift rates for shippers such as Eagle Bulk, which owns one of the world's largest fleet of dry bulk carriers for hauling iron ore and other goods. DryShips is the second-largest carrier of iron ore, and other bulk goods. Primarily transporting oil, Frontline has benefited from the increasing demand from China and India . Since China is the largest importer of iron ore, oil, and other commodities, its renewed demand for those goods could increase the global demand for shipping:

Metric | Vale | Rio Tinto | DryShips | Eagle | Frontline |

|---|---|---|---|---|---|

Share Price Performance Last Month | 8.26% | 4.64% | 25.44% | 22.83% | 5.72% |

Share Price Performance Last Year | 5.26% | 8.25% | (1.40%) | (44.61%) | (15.42%) |

Source: Finviz.

More iron ore and other transport business from China is needed by shippers. As the chart below reveals, earnings per share have plunged for Frontline, Eagle Bulk, and DryShips so that it is now negative for each.

FRO EPS Basic Annual data by YCharts.

What is also troubling is how the earnings before interest and taxes (EBIT)-to-interest expense ratio has fallen for Frontline, Eagle Bulk, and DryShips as shown by the chart below. That indicator reveals how easily the company can pay the interest on its debt; if it's less than 1.0, the company isn't making enough to service its debt. The direction of the EBIT to interest expense for these shippers is troubling. If the ratio remains at these levels, the companies won't be able to service their debt for long.

EGLE EBIT to Interest Expense data by YCharts.

Vale is best in its sector in many ways

As the table below shows, Vale's priced attractively compared with the industry average in several critical areas. It is very profitable, with a 29.10% net profit margin for the trailing 12 months, far above the industry average. The strong, above-average gross margin of Vale demonstrates its ability to raise its prices and increase its profits more than its competitors.

Even with such a superior net profit margin, Vale trades at a price-to-earnings ratio below the industry average. It is even more attractive based on that standard, with a forward price-to-earnings ratio of only 8.47. Not only are the earnings undervalued, but so are the assets of Vale, as the price-to-book ratio reveals.

Metric | Vale | Industry Average |

|---|---|---|

Net Profit Margin TTM | 29.10% | 0.26% |

Price-to-Earnings Ratio TTM | 7.00 | 9.00 |

Gross Margin 5-Year Average | 60.50% | 45.70% |

Price-to-Book Ratio | 2.21 | 2.32 |

Source: The Motley Fool CAPS.

What a Fool believes

Vale needs for the Chinese economy to continue expanding. There are many reasons to be bullish on the future of China. In addition to economic growth well over 7%, that country has the largest foreign reserves, is the biggest exporter, and has the highest domestic savings rate in the world.

Vale should benefit from all of that, since Chinese economic growth requires iron ore and other commodities. At around $20 a share, Vale trades far below its five-year high of about $45. If Chinese economic growth picks up, so will Vale's stock price.

Vale's twice-yearly dividend should satiate Foolish investors as they wait for demand from China to lift the share price again. In 2012, Vale paid out $1.17 per share in dividends. Stack that against the current share price and you get a 5.8% yield -- a lot better than you'll find in fixed income these days.

The article Vale Is a Great Way to Profit From China's Growth originally appeared on Fool.com.

Jonathan Yates has no position in any stocks mentioned, and neither does The Motley Fool. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.