This Week's Top Energy Pick: Chevron

Chevron's refreshing fourth-quarter performance update should come as a treat for investors. More importantly, the company reinstated its position as a solid performer and one for long-term investing.

For the past few quarters, the integrated oil and gas supermajor had been struggling with declining production volumes in its upstream segment, as well as some unimpressive refining margins in its downstream division. However, the latest update shows a significant improvement in the underlying fundamentals, which should enhance the company's bottom line. Value investors should take note of these developments, and I believe this stock should continue rewarding shareholders in the years to come.

Solid upstream results

Total U.S. production volumes for the fourth quarter through November was 676,000 barrels of oil equivalent per day, or Boe/d. That's a 6% increase from the third quarter, and 2% from last year. The sequential growth is impressive, and this is mainly due to increased liquids production through its acquisition of acreage in the Permian Basin from Chesapeake Energy. Last September, I mentioned why this addition should boost Chevron's top line.

International production results were mixed. While liquids production grew almost 7% sequentially to 1.34 billion barrels per day, it fell 2.5% from last year's fourth quarter. However, that shouldn't be discouraging at all. Natural gas made up for the shortfall with an impressive 6.6% increase from last year. Keep in mind that international natural gas prices are profitable for exploration and production companies. The average price realized for this commodity was $5.94 per thousand cubic feet -- 7% better than last year. With Asian demand for natural gas on cruise control, I'm optimistic about the future.

Mixed bag for refining

In the downstream segment, U.S. refining margins improved from last year, while it fell on a sequential basis. But international margins failed to impress with a slight fall from the quarter as well as year over year.

Overall, though, there has been a solid improvement operationally, and this should reflect in the cash flows. Management is anticipating production to hit 3.3 billion bpd from the current 2.6 billion bpd, a phenomenal 24% increase.

Why I love this stock

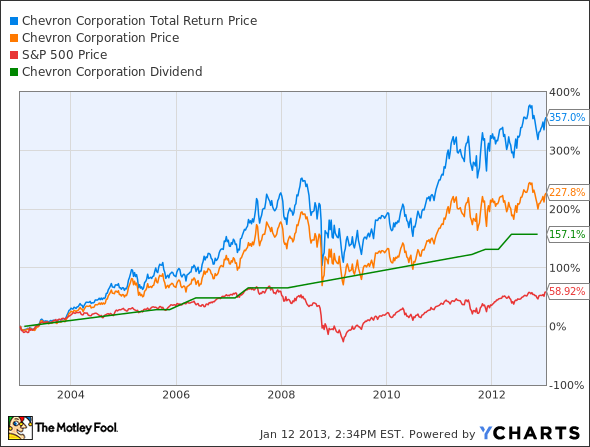

From an investor's perspective, the stock's historical performance is a motivating factor. With reinvested dividends, the 10-year returns have been fabulous.

CVX Total Return Price data by YCharts.

Management has been raising the dividend steadily and should do so going forward. That's why I see little reason this performance shouldn't be replicated going forward.

Form a valuation point, the stock looks pretty cheap.

Company | TTM P/E | Price-to-Book | Dividend Yield |

|---|---|---|---|

Chevron | 9.2 | 1.6 | 3.3% |

ExxonMobil | 9.5 | 2.4 | 2.6% |

Occidental Petroleum | 11.4 | 1.7 | 2.6% |

Source: Yahoo! Finance. TTM= trailing 12 months.

Chevron's price-to book is among the lowest in the industry, meaning its assets could be undervalued. Also, a 3.3% dividend yield is hard to ignore.

For Foolish investors looking for a stable energy stock, this could be the one -- it's my top pick for this week.

But if you're interested in some more dividend players on your quest for high-yielding stocks, The Motley Fool has compiled a special free report outlining our nine top dependable dividend-paying stocks. It's called "Secure Your Future With 9 Rock-Solid Dividend Stocks." You can access your copy today at no cost! Just click here to discover the winners we've picked.

The article This Week's Top Energy Pick: Chevron originally appeared on Fool.com.

Isac Simon has no position in any stocks mentioned. The Motley Fool recommends Chevron and owns shares of ExxonMobil. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.