2 Pipeline Stocks Poised for Profits in 2013

Enterprise Products Partners and Enbridge made a lot of noise last year, when they reversed their 50/50 joint venture Seaway pipeline so that it carried crude oil from Cushing, Okla., down to the Gulf Coast. The reversal helped alleviate what is still quite the glut of crude oil sitting at Cushing. Luckily, Enterprise and Enbridge just announced that expansion work on the Seaway is complete, bringing its Cushing takeaway capacity up from 150,000 to 400,000 barrels per day.

These two companies are among the biggest players in the midstream industry, so let's take a closer look at what 2013 might have in store for them.

High-performance vehicles

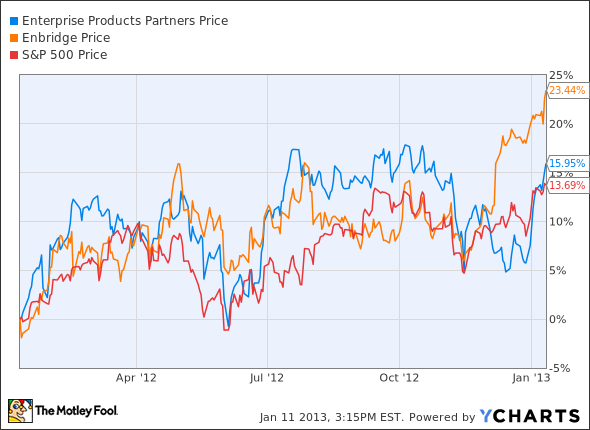

Both Enterprise and Enbridge are coming off great years and continue to find success in share performance in 2013. Take a look at trailing-12-month performance for both companies compared with the S&P.

Though Enterprise's growth wasn't as consistent as Enbridge's, both companies performed quite well.

Canadian leader

Enbridge's performance is especially impressive, taken in context of the public-relations battle it fought last year. It continues to fight that battle this year, but there is seemingly no indication that the horrendous PR will slow down its share-price growth.

After all, the company has an extremely favorable position in the current North American oil boom. Its pipeline system is responsible for 13% of American oil imports -- a percentage, and dependency, that will only increase as the U.S. watches more costly seaborne imports decline in the face of growing domestic production.

We can see an example of Enbridge's dominance in recent news about falling Canadian crude prices. The price of Western Canada Select crude fell almost $2.00 in one day after Enbridge initiated a midmonth apportionment on three of its Canada-U.S. pipelines. Apportioning reduces volumes on the lines and creates a backlog, which in turn creates a price discount. This very problem is what caused Enbridge and Enterprise to reverse the Seaway pipeline to begin with.

Enbridge made the move not to flex its muscle, but because of operational issues across its system. The move had such a strong effect because the pipelines carrying oil across the border have been full for months, with no relief in sight. That sort of demand bodes well for Enbridge in 2013.

Variety show

Like Enbridge, Enterprise operates pipelines -- more than 50,000 miles of them -- but it has plenty of other assets that generate cash. Its business mix includes natural gas pipelines and processing centers, natural gas liquid (NGL) pipelines and fractionating facilities, storage facilities, and terminals. The diversity is compelling and will soon grow to include not one, but two propane dehydrogenation facilities. The first facility was announced last year and has enough long-term fee-based commitments to warrant building a second one, though Enterprise hasn't officially announced it will do so.

The interest in these propane facilities is driven by the fact that there is a growing decrease in propylene supplies now that petrochemical companies are consuming more ethane, along with the growing supply of propane coming out of U.S. shale plays. One such shale play is the Eagle Ford in southeast Texas.

Enterprise is one of many energy companies focusing on the Eagle Ford shale right now. As exploration and production companies rush to cash in on the shale's lucrative oil and NGL windows, Enterprise is there to gather production into its pipelines, bring it to its processing facilities, and eventually move it to its export terminals or to pipelines out of town.

And its footprint will continue to grow to meet demand. Enterprise has more than $3 billion in projects coming online in 2013, and much of that is directed at development in the Eagle Ford. Projects in the shale that are expected to come online this year include a crude oil pipeline joint venture with Plains All American Pipeline , phase 3 of a gas processing facility, and phase 2 of an NGL pipeline.

Diversity is important to Enterprise, and that includes where it builds its assets. The partnership won't limit itself to just the Eagle Ford. In fact, it's also building out in West Texas, Colorado, Wyoming, and Pennsylvania.

Foolish takeaway

These two companies are peers in an industry that is on fire right now. Production in North America is still growing and pegged to continue doing so for at least the next few years, which means volumes across the systems of companies such as Enbridge and Enterprise will continue to grow as well. Expect these stocks to grow this year.

Enterprise Products Partners, with its superior integrated asset base, can profit from the massive bottlenecks in takeaway capacity by taking on large-scale projects. To help investors decide whether Enterprise Products Partners is a buy or a sell today, click here now to check out The Motley Fool's brand new premium research report on the company.

The article 2 Pipeline Stocks Poised for Profits in 2013 originally appeared on Fool.com.

Fool contributor Aimee Duffy holds no position in any company mentioned. Check out her holdings and a short bio. If you have the energy, see what she's keeping an eye on by following her on Twitter, where she goes by @TMFDuffy. The Motley Fool recommends Enterprise Products Partners. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.