Is RF Micro Devices Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what RF Micro Devices' recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell RF's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much RF's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If RF's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

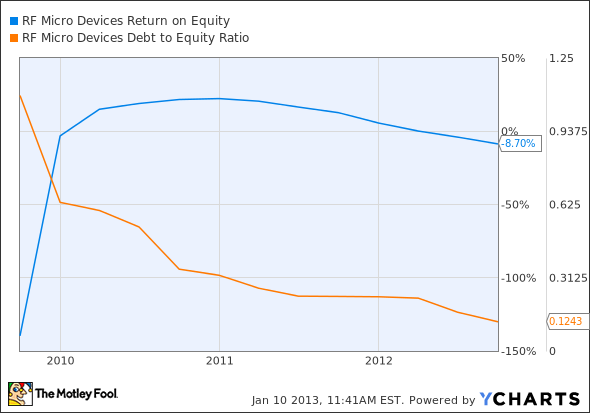

Is RF managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

By the numbers

Now, let's take a look at RF's key statistics:

RFMD Total Return Price data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | (1.9%) | Fail |

Improving profit margin | (237.1%) | Fail |

Free cash flow growth > Net income growth | (69.1%) vs. 93% | Fail |

Improving EPS | 93.4% | Pass |

Stock growth (+ 15%) < EPS growth | (12.7%) vs. 93.4% | Pass |

Source: YCharts. *Period begins at end of Q3 2009.

RFMD Return on Equity data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 93.1% | Pass |

Declining debt to equity | (88.6%) | Pass |

Source: YCharts. *Period begins at end of Q3 2009.

How we got here and where we're going

RF's earned four out of seven passing grades, but it's worth noting that the company started our three-year tracking period in a deep net-income hole as a result of recessionary struggles. Its free cash flow provides a more worrying trend, as it has been sinking for some time. RF remains cash-flow positive, but that may not be the case for long if it can't turn things around. But what will the company need to do in order to improve its failing metrics and earn a better score next time?

A year ago, Fool contributor Harsh Chauhan suggested that you'd be better off avoiding RF, and that's proven prescient. In the past year, the S&P 500 has risen 13.3%, but RF has only recently managed to claw out of a deep hole and return to even-money territory. His reasoning was that RF had failed to diversify away from a small slice of an outdated pie by focusing its business on radio-frequency chips for older cell phones. RF execs are not blind to this problem, and part of the blame for its slide during the first half can be placed on the company's difficult transition period. RF has been historically reliant on lower-tier Nokia phones, which have lost their price edge in the global market as hardware makers increasingly devise ways to sell smartphones at dumb-phone prices.

These misfortunes seemed to change this past summer when analysts began to notice RF's low share price relative to its free cash flow -- which has earned it a P/FCF ratio of 28.3 today after a combination of further share price gains and free cash flow declines. Multiple upgrades were in the offing throughout the latter half of 2012, with the most recent occurring in mid-December.

Undoubtedly, part of this growth is the result of a key placement in Apple's iPhone 5. That alone can't explain this newfound bullishness, as RF rival Skyworks Solutions has multiple placements in the iPhone 5, but has seen both its profit and its free cash flow fall throughout 2012 in spite of sustained high iPhone demand. China's growing adoption of the 3G mobile standard is another reason for optimism, as fewer than 20% of China's mobile subscribers even have a 3G phone at the moment. China Mobile , the largest carrier, has the greatest upside with a 3G penetration rate of less than 10%, but it's also got a more persnickety network standard. That's kept the iPhone off of China Mobile's network so far, but rumors persist that Apple will land on China Mobile's shores at some point this year.

RF has opportunities ahead, but investors should be careful of the company's inability to move its free cash flow levels higher. Without forward momentum, whether in net income or in free cash flow, no company can justify higher prices for long.

Putting the pieces together

Today, RF has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

Apple has been a longtime pick of Motley Fool superinvestor David Gardner, and has soared 219.20% since he recommended it in January 2008. David specializes in identifying game-changing companies like Apple long before others are keen to their disruptive potential, and he helps like-minded investors profit while Wall Street catches up. I invite you to learn more about how he picks his winners with a free, personal tour of his flagship service, Supernova. Inside, you'll discover the science behind his market-trouncing returns. Just click here now for instant access.

Keep track of RF Micro Devices by adding it to your free stock Watchlist.

The article Is RF Micro Devices Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool recommends Apple. The Motley Fool owns shares of Apple and China Mobile. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.