Is Westport Innovations Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what Westport Innovations' recent results tell us about its potential for future gains.

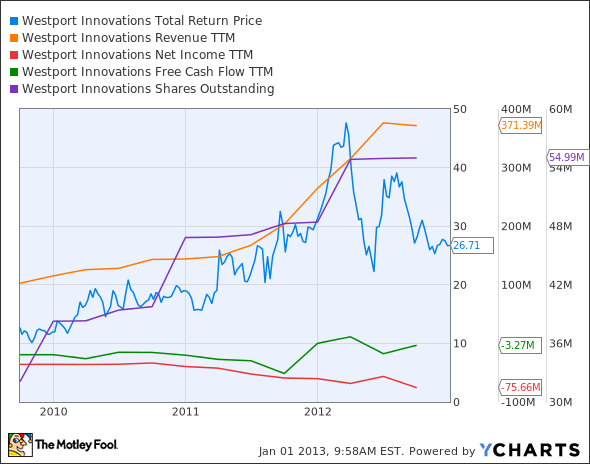

What the numbers tell you

The graphs you're about to see tell Westport's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much Westport's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Westport's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is Westport managing its resources well? A company's return on equity should be improving, and its debt to equity ratio declining, if it's to earn our approval.

By the numbers

Now, let's take a look at Westport's key statistics:

WPRT Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 262.1% | Pass |

Improving profit margin | (50.6%) | Fail |

Free cash flow growth > Net income growth | 83.1% vs. (110.9%) | Pass |

Improving EPS | 26.3% | Pass |

Stock growth + 15% < EPS growth | 110.3% vs. 26.3% | Fail |

Improving return on equity | N/A | Fail |

Declining debt to equity | N/A | Fail |

Source: YCharts and Yahoo! Finance . N/A = not applicable, negative equity.

* Period begins at end of Q3 2009.

How we got here and where we're going

Westport's negative levels of equity make this a much uglier effort than it might otherwise have been. Return on equity and debt to equity had both been trending in the right direction before tracking ceased due to those negative levels late in 2011. Westport shareholders should hope for a return to positive equity next year, which should improve this stock's score from a rather anemic three of seven passing grades.

It may take some time to turn that around, as Westport recently slashed its full-year revenue to the $340 million-$350 million range, which actually comes in below its trailing 12-month revenue of $376 million. Ouch. Some of Westport's big commercial pushes, like its pickup truck engine tie-up with Ford , may not see much in the way of results until later this year, at the earliest. Westport's partnership with engine manufacturer Cummins also takes some of the profitability out of its hands, as Cummins does most of the manufacturing and can thus squeeze more of the efficiency gains from improved processes onto its bottom line.

On the other hand, Cummins and Westport are also working hand in hand with Navistar and natural gas fueling station operator Clean Energy Fuels to push this alternative energy technology. Without Clean Energy's infrastructure, Westport won't see much adoption of its engines, and without more of Westport's engines, Clean Energy's infrastructure won't be worthwhile.

Navistar, as one of the largest truck manufacturers in the country, is an important link in the chain between Westport and Cummins, and it's been in the dumps lately due to weak heavy-duty truck demand. The most recent reports on heavy-duty truck orders indicate short-term weakness that could actually benefit Westport. The analysts at ACT Research, which covered this data point, believe that part of this weakness is tied to buyers' desire to wait for more fuel-efficient vehicles. If you're talking about fuel efficiency, you have to be thinking about natural gas engines, at least in part.

Waiting for a turnaround driven by manufacturing can be agonizingly slow, and Westport's current projections don't impart much confidence. However, 2013 might just turn out to be a worthwhile year for this long-unprofitable company, as truck buyers (and others) find themselves in need of more efficient vehicles. Westport is very close to positive free cash flow, and 2013 might find that line nudging into the black.

Putting the pieces together

Today, Westport has some of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

None

The article Is Westport Innovations Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of Clean Energy Fuels, Cummins, Ford, and Westport Innovations. Motley Fool newsletter services recommend Clean Energy Fuels, Cummins, Ford, and Westport Innovations. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.