Better Know an Energy Play: Marcellus Shale

To help Foolish investors better understand the oil and gas boom in the United States, we are putting together a series of articles focusing on the major energy plays in the lower 48. We'll need to rely heavily on these areas to achieve North American energy independence. Today we're going to take a look at the Marcellus Shale.

Introduction

One of the biggest natural gas plays in the U.S. sits right along the Appalachian Basin, primarily in West Virginia, Pennsylvania, Ohio, and New York. The Marcellus Shale, once known for its black shale is now known for its natural gas. The shale formation is astoundingly deep, ranging from 2,000 feet to 10,000 feet.

Natural gas from Marcellus is primarily found in its rock pores. To get this trapped gas out of the pores, companies need to use hydraulic fracturing, or fracking. Fracking basically means the well is pumped full of water, sand, and chemicals to break up the shale and release the trapped gas.

A U.S. Energy Information Administration (EIA) report released in early 2012 puts the amount of technically recoverable natural gas in Marcellus at 141 trillion cubic feet . For a little perspective, the EIA estimated the U.S. uses about 24 trillion cubic feet per year. The Marcellus Shale has always been known to hold natural gas, but it was too widely spread around to make it worth tapping. But that was before hydraulic fracturing and horizontal drilling came into play. In 2003, Range Resources used drilling techniques from the Barnett Shale to drill one of the first wells in Marcellus.

The moguls of Marcellus

As with any play, companies scramble to buy up the most land leases, because more leases mean more drilling opportunities. The top 11 landholders in the region are Anadarko Petroleum , Cabot Oil and Gas , Chesapeake Energy , Chevron , the joint venture between Consol Energy and Noble Energy , EQT Resources , ExxonMobil , Range Resources , Royal Dutch Shell , Southwestern Energy , and Talisman Energy .

Acreage is one thing, but production is a whole other ball game. The Marcellus play produces 6.8 billion cubic feet of natural gas per day. As you can see based on these charts, there is no direct correlation between the total acreage a company holds and the total production for each company in the region.

Current production and rig count

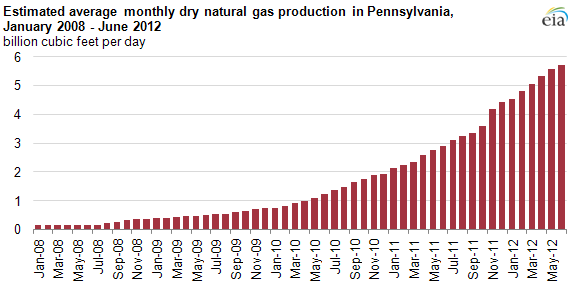

Some parts of the Marcellus Shale will see a slowdown in production in 2013, because there aren't enough existing pipelines to move the natural gas out of the area. New pipeline construction is under way, but most of it won't be online until late 2013. Overall production growth is expected to drop by 1.3 billion cubic feet per day over the next year, down from 2.3 Bcf/d. Although Marcellus production may slow slightly in 2013, overall production is expected to increase to 18 Bcf/d by 2020 - current production is at 6.8 Bcf/d.

As of November, the Marcellus Shale had 88 operational rigs, compared to 111 operational rigs in Pennsylvania alone in 2011. But, the number of rigs doesn't directly correlate to production. Average production in the Marcellus is up 72% compared to last year, because wells extend further into the shale and produce more natural gas than before.

Source: U.S. Energy Information Administration

Source:U.S. Energy Information Administration

Drilling economics: location, location, location

When you drill deep, it isn't cheap. Drilling depths in the Marcellus are some of the deepest in the country. Much of the drilling activity for the Marcellus is occurring around the edges of the play, because this is where drillers can hit the formation at the most shallow depths. As you move further into the center of the formation (right about in the middle of Pennsylvania), the depth of the shale play drops significantly. Some companies with leases closer to the center have drilled to depths as low as 10,000 feet to tap the shale formation.

Drilling costs for a well in the region vary from $2.3 million to $4 million, but this does not necessarily account for all costs. A recent study by the University of Pittsburgh estimated that the total real costs (including leasing and permitting) for a well in the Marcellus to be around $7.6 million. This may seem much less than in comparison to an oil well in, say, the Bakken, but keep in mind that natural gas currently sells at a BTU equivalent price that is less than 1/30 that of oil.

Photo courtesy the Marcellus Center for Outreach and Research at Penn State University

One of the largest costs for these wells is hydraulic fracturing. This process, which is normally done in 10-20 stages per well, costs about $180,000 per fracturing stage. Anadarko and Ultra Petroleum both are reporting wellhead costs on the lower end of the $2 million range, while Range Resources is hovering around the $4 million range.

It is estimated that wells in the Marcellus can be refracked several times (to reopen the shale and improve production rates) and are estimated to have a life span of up to 40 years. EQT Resources estimates that its wells in the play have an estimated ultimate recovery (EUR) of 7.3 billion cubic feet equivalent (or Bcfe, a metric to measure both wet and dry gas).

While the long term prospect of a 40-year well producing 7.3 Bcfe seems appealing, it overlooks the costs required to get to that amount of production. In a recent Department of Energy study of all the major shale plays in the U.S., the government agency discovered that the production decline at a Marcellus well is about 67% in the first 107 days for a horizontal well. Compare this to a 55% decline in the first year for a horizontal well in the Barnett Shale play, and you see how costly it can be to operate in the Marcellus.

Source: U.S. Department of Energy

So if these wells are so expensive to drill, then why are companies so eager to exploit these resources? In this case, it's not what you're drilling for, but where you can drill. The Marcellus and Utica formations are the only gas plays in the Northeast, which puts them right on the doorstep of the most populous part of the U.S. Since natural gas transportation is much more limited than its liquid cousin oil, the costs for moving gas are that much higher.

Based on this info, it would be a rather logical assumption that Marcellus natural gas would sell at a premium to Henry Hub spot prices, the U.S. trading benchmark for natural gas. Sadly, the opposite is happening right now. Based on a recent release from the EIA, natural gas spot prices for the Tennessee Gas Pipeline Zone 4 (a benchmark spot price for Marcellus Shale gas) has steadily dropped since June of this year, as seen in this chart:

Source: U.S. Energy Information Administration

Since production has jumped so quickly in the region, much of the natural gas pipeline network is at capacity. So for gas prices to increase again in the region, the pipeline network in will need to expand. There is plenty of opportunity for some midstream pipeline companies to take advantage of this, and the table below shows some of the largest gas pipeline companies that have projects recently completed, or which will come on line in the next six months.

Company | Total Capacity of New Pipeline Projects (in Mcf/d) | Date of Completion of Projects |

|---|---|---|

Inergy Midstream | 555 | Nov. 2012 |

Dominion Transmission | 1,212 | 2013 |

Texas Eastern | 1,500 | 2013 |

Tennessee Gas Pipeline | 1,306 | 2013 |

Equitrans | 800 | Dec. 2012 |

Spectra Energy | 800 | 2013 |

Kinder Morgan /Equitable | 1,100 | 2013 |

Source: Marcellus Drilling News

This will certainly help to narrow the spread between the Marcellus and Henry Hub spot prices, but it could also further the overall glut of natural gas in the market today. According to analysts at Price Futures Group, a mild winter could see gas prices falling below $2.00 per million BTU.

So you want to buy Marcellus?

With the most lucrative drilling properties around the edge of the play, the biggest story in land purchases is taking place in New York state, where little drilling is happening right now. Because of more restrictive environmental regulations in the Empire State, much of the gas in the region is being left untapped. This trend could come to an end, though. New York Gov. Andrew Cuomo has been in talks with many lawmakers to lift the moratorium on hydraulic fracking in the region. This comes on the heels of a political move by Delaware County, which has asked both New York City and the state to compensate the county $81 billion for unrealized gains from not permitting hydraulic fracking within 4,000 feet of the New York City watershed boundaries.

What these Fools believe

The potential for the Marcellus is there. It is ideally located to supply the most densely populated region of the country, with potential access to some large import/export facilities on the East Coast. The expansion of the pipeline network, and growing demand for natural gas, will help to drive better returns in the region.

Two key areas to keep an eye on are well production efficiency and infrastructure build-out. Companies will work to bring well costs down, while increasing overall extraction production. Low natural gas prices mean companies need to do more with less, and any company that fails in efficiency will be left behind. Also, if those pipelines don't come online in 2013, production could slow down significantly, hurting everyone's bottom line.

With the largest acreage and highest production rates in the entire play, Chesapeake Energy has a lot at stake here in the Marcellus. As the second-largest natural gas producer in the United States, so much of the company's success has depended on natural gas. In our recent premium report on Chesapeake, we examine how the company has shifted its business strategy and what it means for investors. You can get your own copy of this report by clicking here!

The article Better Know an Energy Play: Marcellus Shale originally appeared on Fool.com.

Tyler Crowe has no positions in the companies mentioned above, but he does love to drill down into the secrets of the energy sector. You can follow him on Fool.com under TMFDirtyBird, Google +, or Twitter @TylerCroweFool.Fool contributor Chris Neiger has no positions in the companies mentioned, but he likes to write about companies that dig through rock to find energy sources. Follow him on the Fool.com under TMFNewsie.The Motley Fool owns shares of Kinder Morgan, Ultra Petroleum, and ExxonMobil and has the following options: long JAN 2013 $16.00 calls on Chesapeake Energy, long JAN 2014 $20.00 calls on Chesapeake Energy, long JAN 2014 $30.00 calls on Chesapeake Energy, short JAN 2014 $15.00 puts on Chesapeake Energy, long JAN 2014 $30.00 calls on Ultra Petroleum, long JAN 2014 $40.00 calls on Ultra Petroleum, long JAN 2014 $50.00 calls on Ultra Petroleum, and short JAN 2014 $20.00 puts on Ultra Petroleum. Motley Fool newsletter services recommend Chevron, Kinder Morgan, Range Resources, and Ultra Petroleum. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.