The "Slower Than Molasses" Economic Recovery

All economic measures are moving at a snail's pace. Employment is improving, but only slowly. Housing is also recovering -- slowly. And consumer spending is rising...well, you know. Why is the whole economy acting like it's drenched in molasses?

Blame the sugary-sweet concept of excessive debt.

Sticky unemployment

While the unemployment rate has declined from 10% in 2009 to 7.7% today, it's been accompanied by a decline in the proportion of the population that works from more than 63% before the recession to less than 59% today. Jobs are coming back, but at a rate of roughly 150,000 new jobs per month, that's just enough to slightly outpace the country's population growth.

Source: Federal Reserve Bank of St. Louis.

Current forecasts expect unemployment to sink below 7% sometime around 2015 to 2016. So, expect more of the slow same in job numbers.

But why has job growth been so slow?

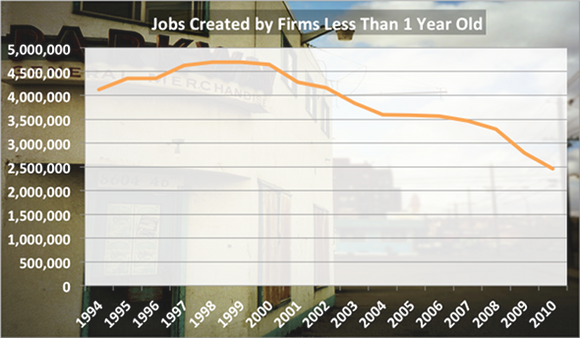

One reason is that new businesses have contributed less and less to job creation:

Source: Business Employment Dynamics, Bureau of Labor Statistics.

If new businesses created as many jobs as they did back in the late 1990s, they would add an additional 2 million jobs per year, or about 160,000 more per month -- more than double the current rate of job creation. And how come new-business hiring has fallen off? It's probably because entrepreneurs are likely saddled with the same debt of consumers. It's difficult to start a business without the capital, and when you have monthly payments to make, it's an easier decision to stick with a job than to take a risk on a new business.

Hindered housing

The Case-Shiller Home Prices Index rose for the sixth month in a row, which puts it back at 2003 levels. Housing stocks like PulteGroup and Hovnanian have both crushed the market this year with respective returns of more than 170% and 265% and respective net contract unit growth of 27% and 33% over last year.

With a rise in home prices of about 3.6% compared to the year prior, housing is on its way back, but it's definitely hampered by debt. As Fool Morgan Housel writes: "Regions with the lowest debt accumulation barely saw any dip in residential investment. Regions where it was the highest saw construction collapse by more than half." Excessive debt built up the real-estate bubble, and it's lingering effects make a recovery more difficult.

And, as Shiller himself says: "It can get as big as it was again maybe in 50 years. This housing bubble was a once-in-a-lifetime thing."

Crippled consumer-spending

With the lack of jobs and cut in housing values, consumers have cut back on discretionary spending more than in any recession since 1959:

And not only did consumers cut back on things like trips to Vegas like never before, but they've also been reluctant to start spending again, as Jonathan McCarthy of the Federal Reserve Bank of New York charts:

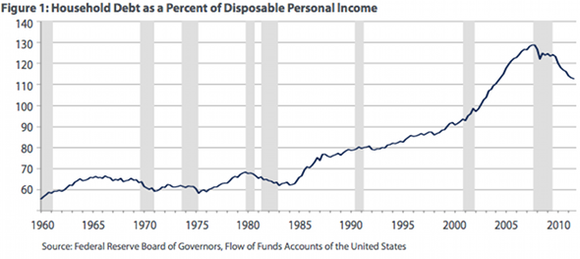

As McCarthy writes, "Households may still see the need to repair their balance sheets from the damage incurred during the recession, especially if they expect the increases in asset prices will be subdued at best and that credit will continue to be constrained." And balance sheets still have a long way to go before they return to where they were even in 2000, as this chart from the Federal Reserve Bank of Richmond shows:

Even though household debt service -- those things like monthly payments -- are at a relative low because of low interest rates, household debt as a percent of disposable income is still at 103%. There are large debts that still need paying off, and although consumers pay a relatively smaller part of their income each month on that debt, the balances are still high compared to historical levels. Until that debt comes down to numbers consumers feel comfortable with, trips to Vegas will be put off. Take a look at MGMResorts' latest quarter as an example: Domestic revenue fell 2% on declines in hotel occupancy, food and beverage, and entertainment sales.

Debt-driven delays

The recovery is far from over, and companies will have to fight with consumers and competitors to win their hard-earned discretionary income as it slowly rises back to pre-recession levels.

And as the recovery crawls along in the right direction, the S&P 500 (INDEX: ^GSPC) and Dow Jones Industrial Average (INDEX: ^DJI) could return to pre-recession levels -- just a lot more slowly than in the past. For the S&P 500, this means a 10% spike from its current price to its historic high of 1,565. And for the Dow, it means a 7% climb to its high of 14,164. Both of these milestones were attained back in 2007, and the five-plus years it has taken to come this close again shows how slowly the economy has trudged along the path to prosperity.

Given this slow recovery, the Motley Fool's chief investment officer has selected his No. 1 stock for the next year. Find out which stock could beat the market in our brand-new free report: "The Motley Fool's Top Stock for 2013." Just click here to access the report and find out the name of this under-the-radar company.

The article The "Slower Than Molasses" Economic Recovery originally appeared on Fool.com.

Fool contributor Dan Newman has no positions in the stocks mentioned above. The Motley Fool has no positions in the stocks mentioned above. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.