Why I Turned Down Annaly's Massive Dividend

I didn't invest in Annaly Capital . I saw its double-digit dividend, and I recognized it as the standard-bearer in the industry. Before the premature passing of CEO Michael Farrell, I also knew that if there was a mortgage REIT industry guru, he was running Annaly.

But I still didn't buy.

A matter of timing

The reason I didn't chase Annaly was largely because of when this company popped up on many people's radars.

When judging the success of a business, there are always a number of factors that the business and its managers can control (think overhead expenses or product mix) and there are things they can't control (the economy, or hurricanes). Often we hear the uncontrollable used as an excuse for poor performance at a company. Rarely do we hear the uncontrollable cited as a key driver in a company's success.

If we look back at Annaly over the past five years, the company has been the beneficiary of some extremely favorable trends. With a strategy of lending long -- that is, investing in longer-dated instruments -- and borrowing short -- funding itself with shorter-dated loans -- the rapid drop in interest rates provided a huge earnings tailwind for Annaly.

If we had stepped back to look at this, it would have been pretty clear that this wasn't a success factor that was likely long lived. And if we bring the focus back to today, we can see some of the external benefit reversing. Assets owned by Annaly are maturing, and the money is being reinvested at today's lower rates, revealing the less-attractive spreads of a lower-rate environment. Further, the Federal Reserve's continuing quest to juice the economy by stomping down rates has led it directly into Annaly's agency-backed paper playground. That's threatened Annaly enough that its starting to take bold moves like proposing to acquire CreXus .

Not convinced?

If you're still not convinced that this has been a particularly favorable period for Annaly, consider the huge influx of mortgage REIT companies starting in 2007. That list includes Annaly offspring Chimera and CreXus as well as American Capital Agency , ARMOUR Residential , and Two Harbors . Notably, 2007 was the year that the Fed began drastically cutting interest rates.

Investors should always view this kind of rapid industry growth with skepticism. Often this kind of expansion means that industry conditions are suddenly highly favorable, and there are low barriers to entry. The first reason can be a positive if those conditions are sustainable, but they're often not. And if you combine short-term favorable conditions with many new companies rushing in, the results usually aren't pretty.

Maybe some day

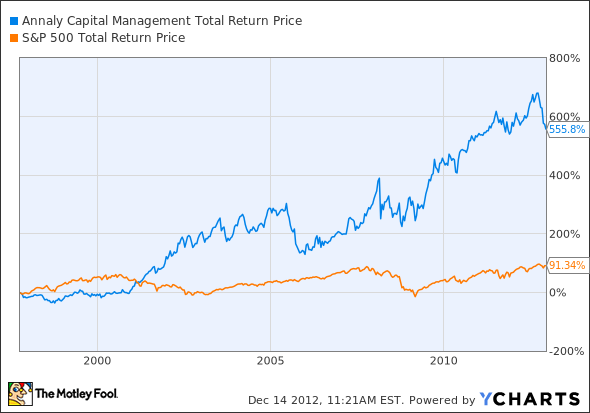

I could look back at the five-year results for Annaly's stock and regret the fact that, on a total-return basis, it's vastly outpaced the S&P 500.

NLY Total Return Price data by YCharts.

But five years ago was the essentially the lift-off point for the factors I discussed above. Kudos are due to those investors who got in right then and rode the tide.

However, much of the excitement over Annaly fired up after the environment was already showing in the company's bottom-line improvements. At that point, it was largely too late to hop in. Over the past three years Annaly has underperformed the S&P.

NLY Total Return Price data by YCharts.

None of this means I've written off Annaly completely. Unlike the recent upstarts in the industry, Annaly has shown a somewhat longer-term ability to manage its business and deliver for investors. Looking back over the stock's complete historical performance (on a total-returns basis of course), we see the results are certainly eye-catching.

NLY Total Return Price data by YCharts.

Just as external conditions can be unusually beneficial to Annaly, they can also be unusually painful for it. When those painful conditions arise, there's a good chance investors will overlook the fact that conditions punishing the company are likely to change in the future. As a result, weak hands will flee the stock. When that day comes, investors with a patient hand and a big-picture view may have a better buying opportunity.

Does this all add up to Annaly's stock being a sell right now? There's more to consider than I've covered here. To dig in further on Annaly, secure your copy of The Fool's premium research report on the company. Our analyst runs through these absolute mu-know topics, as well as the future opportunities and pitfalls of Annaly's strategy. Click here now for instant access.

The article Why I Turned Down Annaly's Massive Dividend originally appeared on Fool.com.

Fool contributor Matt Koppenheffer has no positions in the stocks mentioned above. The Motley Fool owns shares of Annaly Capital Management. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.