Stocks for the Long Run: Tesco vs. the FTSE 100

LONDON -- If the long-run return on the market is 9.4% (as researchers at Credit Suisse say), investing in shares should be a no-brainer. Somehow, however, all too often our portfolios don't seem to reflect that attractive performance.

This is partly because that 9.4% number is an average derived from 100 years of data. Picking various time periods within that 100 years gives very different outcomes -- and the market almost never actually returns 9.4% in any single year.

Needless to say, unless you're holding a market tracker, your portfolio could have dramatically different results than what the market experiences. If you own a disproportionate amount of winning shares, your returns could be significantly better than the market. On the other hand...

In this series of articles, I'm looking at how individual shares have performed against the FTSE 100 during the past 10 years. Today, I'm assessing grocery and retail giant Tesco .

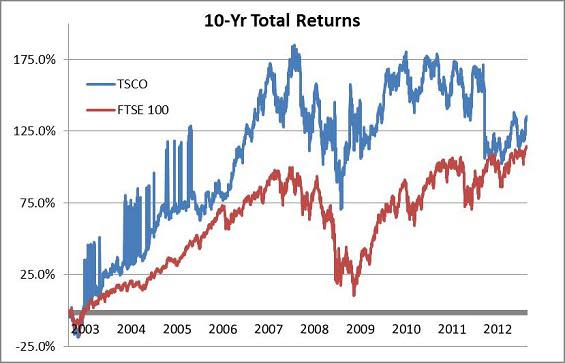

Over the last decade, Tesco's performance has slightly edged out that of the FTSE 100.

Source: S&P Capital IQ.

Until the dramatic sell-off last January, Tesco's shares were solidly thumping the market over the last 10 years, returning an average of nearly 11% per year compared to the 7.8% average return from the FTSE 100. That all changed, however, on Jan. 12, 2012 when Tesco issued its first profit warning in who knows how long, and the shares plummeted 16% in one day. The shares are yet to fully recover.

These days, Tesco's shares are trading on a price-to-earnings (P/E) ratio of 9.7, well below the FTSE 100's 11.6 and near the lowest it's been in the last 10 years.

Source: S&P Capital IQ and Thomson Reuters.

Of course, there's a good reason for these apparently attractive share price. Tesco's domestic struggles are well known and the recent decision to pull out of the US adds one more defeat to the company's attempts to conquer the world.

If Tesco is to grow at any appreciable rate, it needs to succeed in markets outside the U.K. If it can't do that, then the current rating and dividend yield of 4.4% are probably appropriate. However, if shareholders feel Tesco will be able to drive growth through its operations in Asia and Eastern Europe, then the current share price looks attractive.

A company the size of Tesco doesn't change direction quickly, so investors will have to be patient, but the new plan for slower expansion and smaller stores should free up cash flow to support a resumption to growth in the dividend -- which averaged 10% over the past 10 years -- so investors should be paid for their patience.

Large caps for the long run

If Tesco isn't for you or you already own shares, you may also wish to consider the eight large caps spotlighted in "Super-Investor Neil Woodford's Favorite Blue Chips" for your portfolio. You see, this exclusive Fool report evaluates the FTSE shares the legendary index-trouncing investor is backing today, and the investing logic behind them.

You can read all about the potential long-run winners Woodford currently favors by clicking here to download the exclusive report today -- it's free!

The article Stocks for the Long Run: Tesco vs. the FTSE 100 originally appeared on Fool.com.

Nate Weisshaar and The Motley Fool own shares in Tesco.Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.