Is Transocean Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what Transocean's (NYS: RIG) recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell Transocean's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always be reported at a steady rate, we'll also look at how much Transocean's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Transocean's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is Transocean managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

Healthy dividends are always welcome, so we'll also make sure that Transocean's dividend payouts are increasing, but at a level that can be sustained by its free cash flow.

By the numbers

Now, let's take a look at Transocean's key statistics:

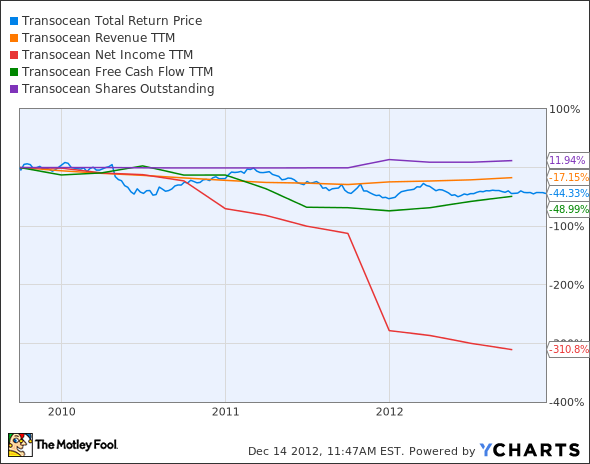

RIG Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | (17.2%) | Fail |

Improving profit margin | (162.1%) | Fail |

Free cash flow growth > Net income growth | (49%) vs. (310.8%) | Pass |

Improving EPS | (309.4%) | Fail |

Stock growth (+ 15%) < EPS growth | (44.3%) vs. (309.4%) | Fail |

Source: YCharts. * Period begins at end of Q3 2009.

RIG Return on Equity data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | (328.6%) | Fail |

Declining debt to equity | 52.9% | Fail |

Dividend growth > 25% | (100%) | Fail |

Free cash flow payout ratio < 50% | NM | NM |

Source: YCharts. * Period begins at end of Q3 2009.

NM = not material due to suspension of dividend.

How we got here and where we're going

We'll give Transocean a mulligan on the final grade, but that still leaves the company with a miserable one of nine possible passing grades. That one pass is due to a technicality more than it is the result of any real improvement. If you've been following along with Transocean's travails, you have a good idea of why this might be so, but a more pressing question is whether or not Transocean can recover soon and begin rewarding shareholders again.

There are a few big roadblocks in Transocean's way. For one, the company has been battling Brazilian authorities over a minor oil spill in the country, which occurred at a Transocean-drilled well in one of Chevron's (NYS: CVX) oilfields. While the legal battle looks to be finally turning in Transocean's (and Chevron's) favor, the company hasn't yet reinstated its dividend, which was last paid in February before executives cut off the payouts.

Transocean's BP (NYS: BP) drama also continues to drag on. The oil supermajor recently received an EPA suspension, cutting off any new business with the government and putting a crimp in deepwater drilling partners such as Transocean. Deepwater Horizon, which greatly damaged the fortunes and public perceptions of both companies, also continues to be a weight. Two months ago, a new oil slick was found in the Gulf, although it wasn't apparently important enough for the government to deal with.

Despite its problems with BP, and the apparent steep losses recorded of late, Transocean's latest results also offered glimpses of a muscular performance, according to the Fool's energy-sector contributor David Lee Smith. Rig utilization rates were up, adjusted earnings beat analysts silly, and the company also reported a big new ultra-deepwater deal with Royal Dutch Shell (NYS: RDS.A) (NYS: RDS.B) .

It appears that there may be some better times ahead for Transocean as it puts a difficult past behind it and refocuses on ultra-deepwater opportunities. The company presents an intriguing play in light of how much better its latest quarter was than was SeaDrill's (NYS: SDRL) . SeaDrill might be one of the faster growing rig operators, but its utilization rate dropped to the same level as Transocean's, which reflects well on Transocean, as the offshore market leader has many more rigs on the water.

Putting the pieces together

Today, Transocean has few of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

The battle between Transocean and SeaDrill for deepwater dominance should only get fiercer as both companies continue to build out their fleets. SeaDrill's become a very attractive stock for investors thanks to its exciting prospect and hefty dividend. Will it continue to outperform, or will Transocean muscle its smaller foe out of the way? What impact will SeaDrill's new MLP and its possible asset spinoffs have on today's shareholders? The Motley Fool's premium research service has plenty of answers to these questions. Getting the information you need is easy -- just click here to subscribe now.

Keep track of Transocean by adding it to your free stock Watchlist.

The article Is Transocean Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.Motley Fool newsletter services have recommended buying shares of Chevron and Seadrill. The Motley Fool has a disclosure policy.We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.