Is Tractor Supply Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what Tractor Supply Company's recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell Tractor Supply's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much Tractor Supply's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Tractor Supply's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

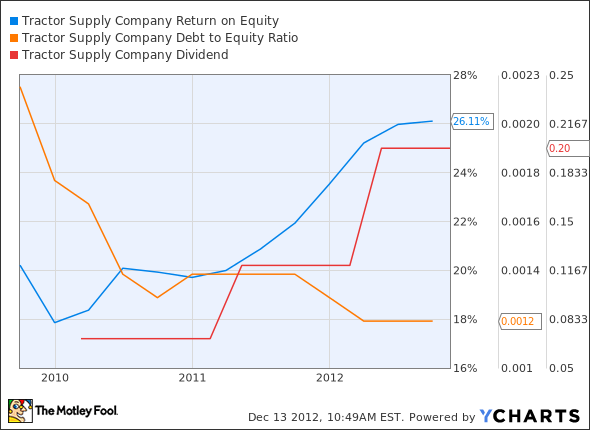

Is Tractor Supply managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

Healthy dividends are always welcome, so we'll also make sure that Tractor Supply's dividend payouts are increasing, but at a level that can be sustained by its free cash flow.

By the numbers

Now, let's take a look at Tractor Supply's key statistics:

TSCO Total Return Price data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 46.9% | Pass |

Improving profit margin | 59.7% | Pass |

Free cash flow growth > Net income growth | 11.6% vs. 109% | Fail |

Improving EPS | 111.0% | Pass |

Stock growth (+ 15%) < EPS growth | 260.1% vs. 111.0% | Fail |

Source: YCharts. *Period begins at end of Q3 2009.

TSCO Return on Equity data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 29.2% | Pass |

Declining debt to equity | (45.5%) | Pass |

Dividend growth > 25% | 185.7% | Pass |

Free cash flow payout ratio < 50% | 35.5% | Pass |

Source: YCharts. *Period begins at end of Q3 2009.

How we got here and where we're going

Although Tractor Supply's free cash flow has lagged its net income, and net income (in the form of earnings per share) has lagged its stock growth by a larger amount, Tractor Supply manages to earn a strong seven out of nine possible passing grades. Is Tractor Supply's outsized stock growth going to be sustainable? It's worth noting that the company's P/E ratio is also up significantly in the past three years, and amounts for most (but not all) of the discrepancy between its stock growth and its EPS improvement.

Tractor Supply's relatively recent dividend is easily sustainable, but its yield has sunk below the 1% level as eager investors hop on the growth train. That places it well behind most farm-supply companies, although its growth rate has trounced nearly all of them. Let's take a quick look at the crowded farming field:

Company | Total Stock Growth* | Net Income Growth* | Dividend Yield |

|---|---|---|---|

Tractor Supply | 260.1% | 109% | 0.9% |

Monsanto | 22.5% | 34.8% | 1.6% |

CF Industries | 148.2% | 260.3% | 0.7% |

Terra Nitrogen | 161.1% | 133% | 7.7% |

Deere | 113.5% | 250.8% | 2.2% |

Source: YCharts. *Growth from end of Q3 2009 (Oct. 30).

Tractor Supply's growth is the only one that's gotten far ahead of the improvement in its bottom line. In fact, only Terra Nitrogen's stock has grown more than its net income, and with a yield like that, it's hard to question why. CF Industries has a lower yield, but it has plenty of room to improve on that payout, which is a minuscule 6% of free cash flow today.

The last time I looked at Tractor Supply, it had hit a 52-week high, from which it's since declined in an almost uninterrupted slide. Shareholders may now be realizing that this well-positioned company can only grow so quickly, and its stock can't outpace fundamental improvements forever.

With so many companies cashing in on the American farming boom, there's no reason to be stuck on Tractor Supply forever. However, if solid gains next year can bring the company's fundamentals back in line with its shares, you might see Tractor Supply pick up additional passing grades and earn a rare perfect score.

Putting the pieces together

Today, Tractor Supply has many of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

Investors in Tractor Supply have gained immensely by hitching their wagons to a fast-growing under-the-radar winner. With the stock at multiyear valuation highs, it may be time to consider other opportunities. The Motley Fool has three suggestions for you in our exclusive free report: "Middle Class Millionaire-Makers: 3 Stocks Wall Street's Too Rich to Notice." Want to learn more? All the information you need is available at no cost, but it won't be around forever. Click here to discover three great small cap stocks today.

Keep track of Tractor Supply by adding it to your free stock Watchlist.

The article Is Tractor Supply Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of CF Industries Holdings. Motley Fool newsletter services have recommended creating a synthetic covered calls position in Monsanto. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.