Top Midstream Company In 2012

As the New Year quickly approaches and we all prepare to make our 2013 investing resolutions, it is a good time to reflect on the year that the energy sector had in 2012.

In this December series, our writers will be recapping some of the most popular, highest-performing stocks across this sector. We will examine whether the gains these companies provided their shareholders in 2012 are sustainable, or whether they should merely be attributed to one-time events or fizzling trends.

Consider these pieces as gifts to benefit our Foolish, long-term investors seeking exposure to the energy sector. Enjoy, and Fool on!

The winner

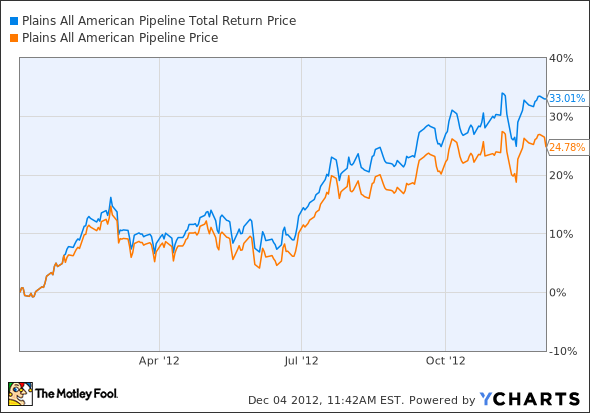

The stock up for discussion today is Plains All American Pipeline . The Houston-based midstream company has had a great year, returning 24.8% at the time of this writing, and an even more impressive 33% with dividends reinvested.

PAA Total Return Price data by YCharts

Let's take a look at what is behind the company's performance, and whether it packs any potential to generate equally impressive returns in the future.

Success!

When I profiled Plains in May, the partnership had returned 9.35%, and was beating the S&P by about 2 percentage points. Its acquisition of BP's Canadian natural gas liquids (NGL) business had closed a month earlier, and Plains was riding high on a very successful first quarter in which revenue climbed 20% year over year, and earnings per share beat analysts' expectations.

As the chart above indicates, Plains continued to find success as the year progressed, but its unit price really took off in July as the company announced excellent second-quarter results and a handful of important new projects.

Interestingly enough, Plains also had to deal with a leak in early June. Its Rangeland pipeline spilled 3,000 barrels of oil into the Red Deer River in Alberta, but the market didn't really react.

In October, the partnership announced a two-for-one stock split. In November, Plains announced another fantastic quarter. Outside of taking an asset impairment charge for giving up on a crude import terminal project in California, Plains reported revenue that was above or in line with guidance across all three of its business segments. Volumes were up, and the new Canadian assets were reporting higher than expected cost recovery for ethane, as well as a reduction in operating expenses.

Growth strategy

Much of Plains' success can be attributed to its plan for growth. The partnership employs a bolt-on acquisition growth strategy, which allows it to pick up assets where management sees the most potential. This allows Plains to grow its asset footprint quickly, with projects that are immediately accretive to the balance sheet. At the same time, Plains is also growing organically, which means that in a few years brand-new projects will compliment the acquisitions and make meaningful contributions to the bottom line.

Here is a snapshot of Plains All American's capital expenditures for the near future:

$250 million geared toward growth in the Permian Basin, including more than 145 miles of expansions and extensions of its mainline pipeline systems.

Construction of a $60 million crude oil pipeline connection in the Bakken Shale, and a $40 million multi-use facility that includes rail service and NGL processing.

$700 million worth of projects in the Eagle Ford, including a joint venture with Enterprise Products Partners that features a 175 mile crude oil and condensate pipeline system and a 1.8 million barrel storage system that is expected to come online in the second half of 2013. Other Eagle Ford projects include an expansion of the Gardendale gathering system and the construction of a stabilization facility. Both projects will be up and running in the first half of 2013.

Notice that all of these projects are geared toward booming oil plays that currently lack adequate midstream infrastructure.

Looking ahead

One of the biggest reasons I like Plains as an investment is because of its management. Aside from having the vision to make strategic acquisitions like picking up BP's NGL assets and building out its rail footprint, there is a tremendous amount of transparency here. It is beyond easy to find presentations, valuable transcripts, and segment operating results on Plains' investor relations page.

Perhaps more importantly, given the demand for quality employees in the oil and gas industry right now, Plains communicates well with its staff and was ranked third in the large company category for the Houston Chronicle's annual "Top Workplaces" survey this year. CEO Greg Armstrong also received the paper's large company leadership award.

Foolish takeaway

The midstream industry as a whole is a pretty good place to find quality investments right now, but I think Plains All American's growth strategy and reliable management make it one of the better opportunities for 2013. Investors committed to finding high-yielding companies should also remember that next year the partnership plans to increase its distribution another 7%-8% over its 2012 exit rate. Plains is committed to growing unitholder returns, and has increased its distribution 32 out of the last 34 quarters, including the last 13 consecutive ones.

One of Plains' joint venture partners, Enterprise Products Partners, is another midstream company to consider. With its superiorly integrated asset base, Enterprise can profit from the massive bottlenecks in takeaway capacity by taking on large-scale projects. To find out if Enterprise Products Partners is a buy or a sell today, click here now to check out The Motley Fool's brand new premium research report on the company.

The article Top Midstream Company In 2012 originally appeared on Fool.com.

Fool contributor Aimee Duffy has no positions in the stocks mentioned above. The Motley Fool has no positions in the stocks mentioned above. Motley Fool newsletter services recommend Enterprise Products Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.