3 Great Fallacies of Investing

The market is full of all sorts of overcomplicated terms and concepts that make investing intimidating for the average person. However, three concepts that are accepted by many money managers and businesses simply don't hold up to reality. Today I'll take a closer look at the widely embraced fallacies of risk-adjusted returns, investment insurance, and the push for reduced regulation on business.

Fallacy No. 1: Risk-adjusted returns are a better judge

Hedge funds, pension funds, and all sorts of investors use a concept called "risk-adjusted returns" to figure out which managers are really outperforming or underperforming the market. The theory is that anyone could outperform the market by making leveraged bets on high-risk stocks, so long as they bet right. And in any bet, you're either right or wrong, so you have a 50-50 shot. So some have decided to use risk-adjusted returns to evaluate someone's real performance.

The concept itself isn't wrong, but it assumes there's an easy way to measure risk. I hate to burst the bubble, but there's not.

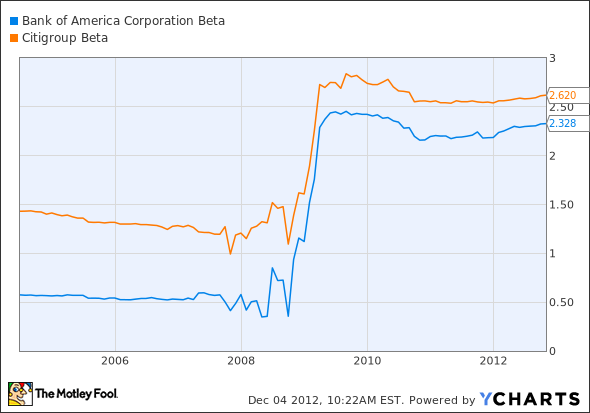

The most common measurement of risk is beta, a calculation that actually measures volatility. To put beta very simply, if a stock goes up 2% when the market goes up 1% and declines 2% when the market goes down 1%, the stock would have a beta of two. This seems simple enough, but it says nothing about the risk involved in any business.

Before the financial crisis, some of the "safest" investments, according to beta, were bank stocks. These were also some of the most widely held stocks. In 2008, Bank of America had a beta of just more than 0.5, indicating that the stock was half as risky as the entire market, while Citigroup's beta was less than 1.5.

Hypothetically, a portfolio holding just Bank of America and Citigroup would have a risk profile about equal to the market. But clearly, these two companies have vastly underperformed the market over the past five years.

BAC Total Return Price data by YCharts.

The point is that returns are returns. Either you make money or you lose money when you make an investment. Trying to quantify risk with a single number is a fool's errand, because by the time your metric accounts for the risk that was inherent in a company or other investment to begin with, it's too late.

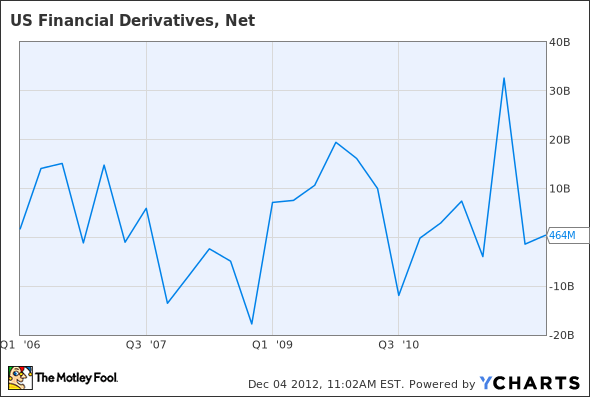

Fallacy No. 2: Derivatives are insurance

Part of the danger of derivatives is that traders actually refer to these products as insurance. But insurance is backed by assets, not leveraged hedge funds and risky banks that normally trade derivatives. We found out just how dangerous and complicated these products were during the financial crisis, but that has done little to shrink the size of the market:

US Financial Derivatives, Net data by YCharts.

If traders want assurance they won't lose money on mortgage-backed securities or any other investment, they should just sell these assets. Derivatives only distort the market by giving a false sense of security that's only exposed after it's too late.

Fallacy No. 3: All regulation is bad for business

Coming out of election season, it would be easy to think that businesses all want less regulation. Oil and gas companies complain about it, and coal companies say it's killing their industry. But the fact is that most companies should want more regulation.

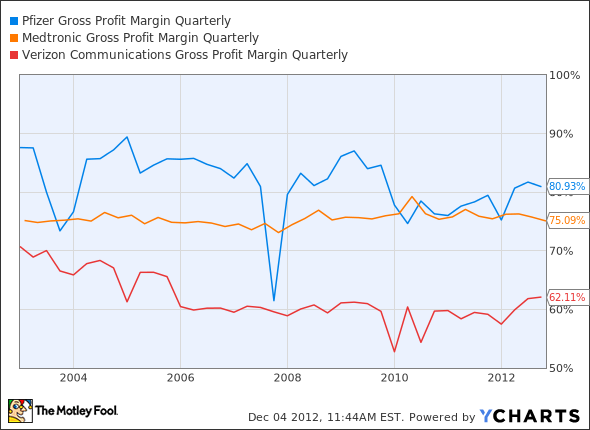

If we look at Porter's five forces -- a widely taught model for evaluating a company's strategic position -- we will get a clue why. Two of these forces are the threat of new entrants and the threat of substitute products. Regulation helps assure that these threats are mitigated by making it harder to start a new company and replace products.

Think about pharmaceuticals, medical devices, and telecommunications businesses, which are highly regulated. Regulation helps keep margins extremely high in these businesses. Below, I've charted the gross margins for Pfizer , Medtronic , and Verizon , which all exceed 60% gross margins.

PFE Gross Profit Margin Quarterly data by YCharts.

Compare that to a business like retail and homebuilding, which is extremely competitive and easy to enter. You see that margins are much lower:

WMT Gross Profit Margin Quarterly data by YCharts.

There are a million factors that go into profit margins, including international trade and technology, but the notion that all regulation is bad for business is misguided. Regulations make it harder for competitors to enter the market and can make replacement products more difficult to make. In many industries, regulation is good for business.

Foolish bottom line

Understanding the factors that truly make one investment better than another over a long period of time is more important than trying to calculate adjusted returns or finding insurance against losses. We're investors, and taking risks is what we do.

In our Foolish opinion, the best investing approach is to choose great companies and stick with them for the long term. In our free report "3 Stocks That Will Help You Retire Rich," we name stocks that could help you build long-term wealth and retire well, along with some winning wealth-building strategies every investor should be aware of. Click here now to keep reading.

The article 3 Great Fallacies of Investing originally appeared on Fool.com.

Fool contributor Travis Hoium has no positions in the stocks mentioned above. You can follow Travis on Twitter at @FlushDrawFool, check out his personal stock holdings or follow his CAPS picks at TMFFlushDraw. The Motley Fool owns shares of Bank of America, Citigroup, and Medtronic. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.