5 Signs Deleveraging Is Working for Telefonica

While the European debt crisis has caused investors to flee from many of the stocks from that continent, there are opportunities for Foolish investors with a long-term outlook. Phone companies, for one, are excellent investments for profiting from the growth of an economy. Among them is Telefonica (NYS: TEF) , the largest Spanish company by market capitalization and the fifth largest mobile network provider in the world. Down more than 20% for the year, Telefonica is starting to recover, with a share-price increase of almost 10% over the past six months.

Instrumental in this boost has been a focus on deleveraging. Moving to shore up its finances, Telefonica has reduced its debt by about 10% since the end of June, a move that facilitated profit growth in September of 24% and that helped generate far greater cash flow and improve the company's liquidity position. Foolish investors should look for future gains from Telefonica, as the deleveraging has earnings-per-share growth surging on a quarterly basis, with a 26.4% year-over-year jump in net income for the first nine months of 2012.

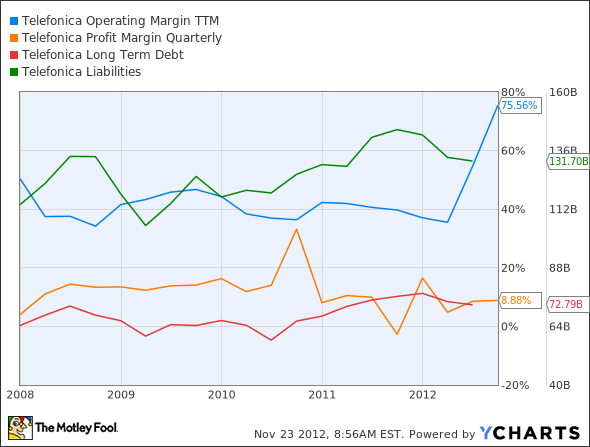

Improving profit margin

This deleveraging is greatly improving Telefonica's margins, too. Its profit margin has increased as total liabilities and long-term debt have decreased.

TEF Operating Margin TTM data by YCharts.

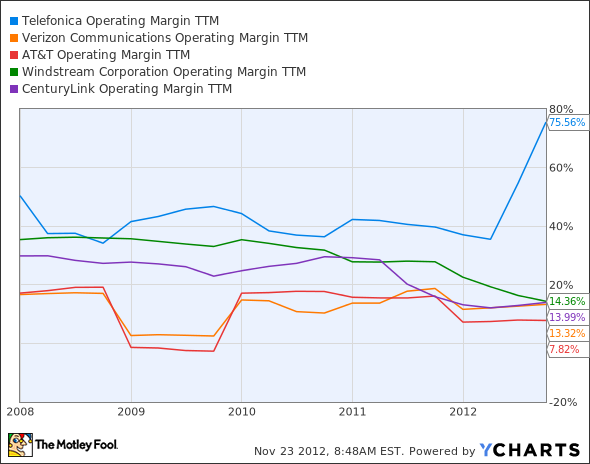

Superior operating margin

The net operating margin, critical for gauging how much cash is left over after the costs of running the company are calculated, has drastically changed for Telefonica, to the point that it's now far superior to phone companies such as Verizon (NYS: VZ) , AT&T (NYS: T) , Windstream (NAS: WIN) , and CenturyLink (NYS: CTL) .

TEF Operating Margin TTM data by YCharts.

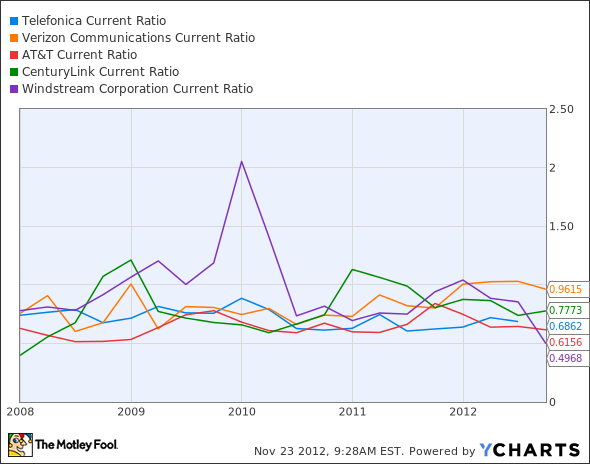

Superior current ratio

Used for measuring a company's ability to pay its short-term liabilities with its ready short-term cash, the current ratio is a solid barometer for a company's viability. Telefonica's current ratio is getting better since it bottomed out in 2011 and is now superior to that for Windstream and AT&T.

TEF Current Ratio data by YCharts.

Superior cash structure

Telefonica's cash structure now compares favorably with others in cash flow, net profit margin, and price-to-earnings ratio. The cash flow and profit margin should continue to improve as the company further reduces its debt load.

Metric | Telefonica | A&T | Verizon | Windstream | CenturyLink |

|---|---|---|---|---|---|

Price-to-Cash Flow | 3.80 | 8.50 | 6.40 | 3.50 | 4.40 |

Net Profit Margin | 10.40% | 3.50% | 2.70% | 2.70% | 3.50% |

Price-to-Earnings Ratio | 7.40 | 44.50 | 40.00 | 33.00 | 37.10 |

Source: Motley Fool CAPS.

Share price rises as liabilities fall

Not surprisingly, Telefonica's share price has been rising as liabilities have fallen. Expect that trend to continue as margins get even better, resulting in greater net income.

TEF Liabilities data by YCharts.

What a Fool believes ... for the future

The debt crisis in Europe is far from being over, and that's a major reason a blue chip such as Telefonica can sell at a P/E ratio of just 2.53. In 2007, the P/E was over 20. Management also responsibly terminated a once-healthy dividend, and the cash left over from that decision has helped to stabilize the balance sheet.

Eventually, the dividend yield and double-digit P/E ratios standard for major phone companies will return for Telefonica. The deleveraging now taking place is a major step in that direction, setting the stage for strong returns for Foolish investors who buy Telefonica as it recovers.

Warren Buffett has said to be greedy when others are fearful, and that's shrewd advice while Telefonica is trading at such an appealing price. Investors don't come much smarter than Buffett. To see what others like Buffett are doing, check out our exclusive free report on The Stocks Only the Smartest Investors Are Buying. Just click here to start reading.

The article 5 Signs Deleveraging Is Working for Telefonica originally appeared on Fool.com.

Jonathan Yates and The Motley Fool have no positions in the stocks mentioned above. Motley Fool newsletter services recommend AT&T. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.