Is Intuitive Surgical Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what Intuitive Surgical's (NAS: ISRG) recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell Intuitive's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much Intuitive's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Intuitive's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is Intuitive managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

By the numbers

Now, let's take a look at Intuitive's key statistics:

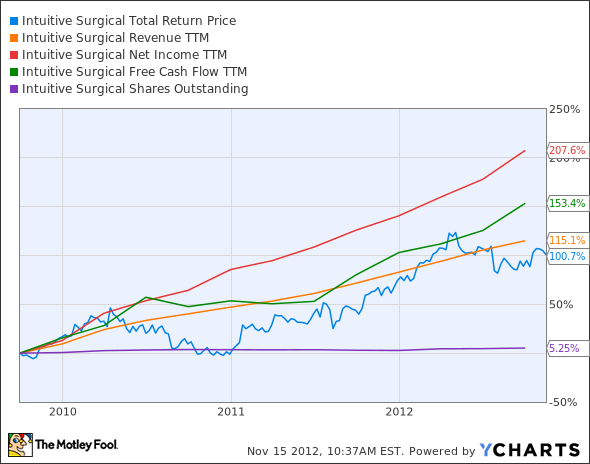

ISRG Total Return Price data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue Growth > 30% | 115.1% | Pass |

Improving Profit Margin | 48% | Pass |

Free Cash Flow Growth > Net Income Growth | 153.4% vs. 207.6% | Fail |

Improving Earnings per Share | 194.3% | Pass |

Stock Growth (+15%) < EPS Growth | 100.7% vs. 194.3% | Pass |

Source: YCharts. *Period begins at end of Q3 2009.

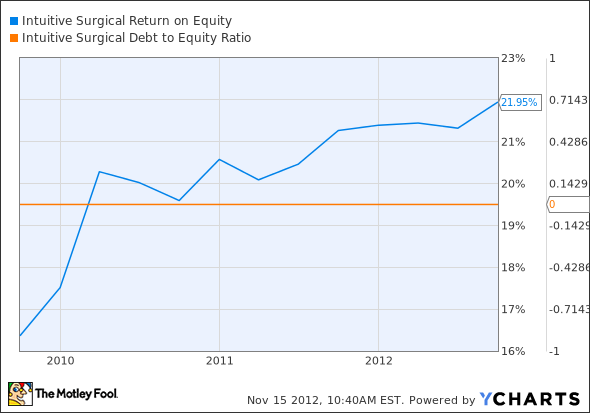

ISRG Return on Equity data by YCharts.

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving Return on Equity | 34.1% | Pass |

Declining Debt to Equity | None | Pass |

Source: YCharts. *Period begins at end of Q3 2009.

How we got here and where we're going

Intuitive earns an impressive six of seven possible passing grades, falling short of a perfect score only because free cash flow hasn't quite kept pace with net income. Otherwise, this is a very impressive score, from a company that's posted extremely consistent growth. Almost... robotic, you might say, in its progress. But will the machine keep churning, or is Intuitive going to need a tune-up soon?

Intuitive's latest earnings, while offering excellent results generally, couldn't quite meet the high expectations Wall Street had for the company. Europe continues to pose problems: Medical-devices company Edwards Lifesciences (NYS: EW) offered a warning bell for Intuitive shareholders when its own earnings showed weakness on the continent. Fool analyst Brenton Flynn points out the unanimity of medical-device executive moping over Europe, which includes normally indomitable Johnson & Johnson (NYS: JNJ) as well as Intuitive.

However, if Intuitive's growth is slowing, it hasn't dampened management's bottom-line expectations. The company is one of the very few American medical-devices companies to have avoided underperformance in Europe. Stryker (NYS: SYK) and Boston Scientific (NYS: BSX) both showed weakness in the third quarter tied to poor international sale, in addition to the companies noted earlier. Intuitive's innovative edge may simply be powering through the cost concerns that crop up when money is tight.

Intuitive's recent history has also been stronger than that of "Intuitive 2.0," MAKO Surgical (NAS: MAKO) . This outperformance is in no doubt due in large part to Intuitive's wider range of procedural offerings. Intuitive's continued to expand these offerings, and recently got FDA clearance for a new surgical stapling instrument. That will help offset what appears to be reduced interest in Intuitive's prostatectomy procedures, eroding after a prostate-cancer screening method failed to meet a government task force's standards.

Putting the pieces together

Today, Intuitive has many of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

Intuitive Surgical's shareholders have enjoyed an epic ride over the past few years. What do the next few years have in store? The Fool's health care team is ready to answer all your questions in an exclusive Intuitive Surgical research service. They've dug deep into Intuitive's data and public statements to put together a complete and fair picture of this exciting company, with frequent updates to make sure you're up to date. If you want to stay ahead of the Street when it comes to Intuitive, the Fool is here to help. Click here to sign up today.

The article Is Intuitive Surgical Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of MAKO Surgical and Johnson & Johnson. Motley Fool newsletter services have recommended buying shares of MAKO Surgical, Johnson & Johnson, and Intuitive Surgical. Motley Fool newsletter services have recommended buying calls on Johnson & Johnson. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.