Is Corning's Glass Half Empty After All?

When I previewed Corning's (NYS: GLW) third quarter, I took a "glass half full" view. The glass and ceramics giant was supposed to show earnings of $0.32 per share on a cool $2 billion in revenue, led by strong demand for its various products for builders of smartphone and tablet screens.

Corning delivered in spades, with non-GAAP EPS of $0.34, and sales hit the Street target right on the nose. The tablet-friendly Gorilla Glass line drove the specialty materials division to 21% year-over-year sales growth, and that helped Corning's total results overcome soft demand for fiber-optic cables.

But if Corning's quarter was so solid, why did the stock plunge as much as 9.6% this morning? That glass must be half empty after all!

It's all about the future, dear Fool. CEO Wendell Weeks lamented "weakening global economic conditions" as he issued a weak forecast for the fourth quarter. He expects the tough market to linger in 2013 and hinted at cost-cutting actions including "modest headcount reductions."

Such bottom-line boosting moves are often seen as a good thing for companies that slash their payrolls, but not this time. Worries about the global economy overshadow any positives you might find in this report.

Does Corning deserve Mr. Market's evil eye? I'm not so sure.

Sure, the company fights the same economic headwinds as everyone else. But the very sectors that hold Corning back today look like springboards for tremendous growth when the grass turns greener.

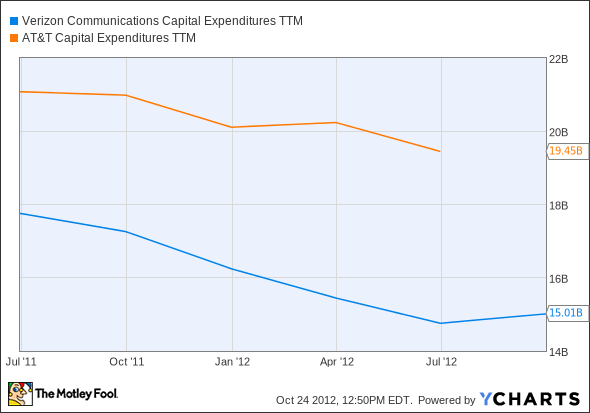

Fiber-optic builds can't remain invisible forever. The demand for high-speed data is exploding far too fast for that. At some point, telecoms and data-link specialists will have no choice but to order Corning's fiber by the boatload. I'm looking at you, Verizon (NYS: VZ) and AT&T (NYS: T) -- your sluggish capital investments simply don't square with your smartphone ambitions and 4G network plans:

VZ Capital Expenditures TTM data by YCharts.

That spring-loaded segment also ties right into Corning's biggest current strength, which rests right on top of mobile computing. Corning doesn't even care who wins the smartphone wars because it sells Gorilla Glass on both sides of the fence -- you'll find its ultra-strong glass panels on both the Apple (NAS: AAPL) iPhone and the Samsung Galaxy S3, just to name the most prominent examples.

And the long-term opportunity doesn't end there. Corning is solidly profitable even in these hard times, and just gave its dividend a 20% boost. There's something to love about this stock for everyone, from growth gurus to dividend disciples. That's why I'm happy to start a bullish CAPScall on Corning today, taking advantage of short-sighted discount pricing on a five-star CAPS stock.

With the explosive growth of smartphones worldwide, many investors thought they would ride Corning's dominant cover glass to massive investment returns. That hasn't played out yet, as mobile growth has failed to offset declines in the company's core business. In this brand-new premium research report on Corning, our analyst walks you through the business, as well as the key opportunities and risks facing it today. Click here to claim your copy, and receive a full year of updates as key events unfold.

The article Is Corning's Glass Half Empty After All? originally appeared on Fool.com.

Fool contributor Anders Bylund has no positions in the stocks mentioned above. Check out Anders' bio and holdings, or follow him on Twitter and Google+. The Motley Fool owns shares of Apple and Corning. Motley Fool newsletter services recommend Apple, Corning, and AT&T. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.