What's Behind Peabody's Big Jump?

Here at The Motley Fool, we encourage investing with a long-term time horizon. Paying attention to the daily gyrations of the market is enough to drive anyone insane. Plus, buy-and-hold investing is a proven method for solid investing results.

That said, when a company's stock price makes a really big move, it's probably a good idea to check up on it and see what the story is. Thus is the case today for Peabody Energy (NYS: BTU) , which has been up by as much as 14% after coming out with earnings.

Read below to see why there was such a pop, and at the end I'll offer up access to a special free report that promises to show you the one energy stock you need to own before 2014.

Surprising the market in a down year

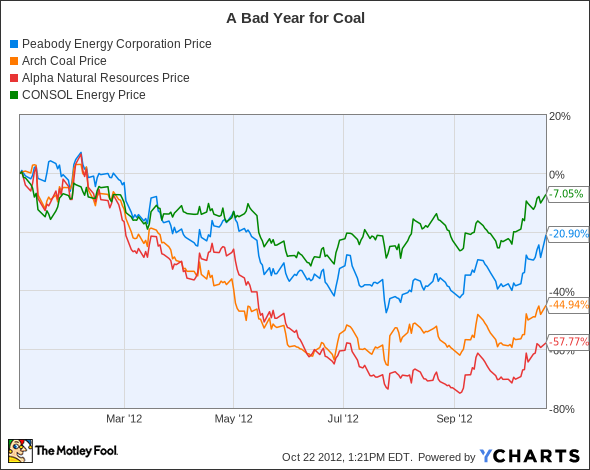

Peabody is a company that mines coal and then sells it to electric utility companies to generate the stuff that powers our lightbulbs, and sells metallurgical coal to industrial companies. The coal industry itself has had a rough 2012.

Here's a look at how some big-name coal companies have performed so far in 2012, including Arch Coal (NYS: ACI) , Alpha Natural Resources (NYS: ANR) , and CONSOL Energy (NYS: CNX) .

The supply glut of natural gas this year has had a dual effect. First, it has significantly reduced the profitability of some major natural-gas extractors like Chesapeake Energy (NYS: CHK) -- though there are several other reasons for the company's tough year.

And it has also made natural gas much more attractive than coal -- as it is also far cleaner and better for the environment when burned, in addition to being cheaper -- which has put a serious dent in the coal business. That helps account for the hard times Arch Coal, Alpha, CNX, and Peabody have had.

All of the doom and gloom that's surrounded the industry might help explain why investors were so happy with today's results. Here's how the company measured up against expectations.

Earnings per Share | Revenue | |

|---|---|---|

Expected | $0.34 | $2.0 billion |

Actual | $0.51 | $2.1 billion |

50% | 5% |

Sources: E*TRADE, Zacks Equity Research.

It's important to keep things in perspective here. While earnings came in significantly higher than expected, they were still 43% lower than the same time last year.

Much of this has to do with accounting standards depreciation, depletion, and amortization expenses. These measures can be a bit esoteric and not reflect the actual cash coming in and going out of Peabody's coffers.

To get a better picture, we can look at revenue. By that measure, there was solid 4% growth year over year.

So is it a buy?

Peabody's management announced back in early 2011 that it thought the coal industry was in the beginning stages of a long-term "super cycle" of growth. But just because they say so doesn't make it so. The role of China's economy and its eventual slowing will likely play a significant role in how demand for coal plays out.

Peabody CEO Gregory Boyce said, "While the global coal environment remains challenged, there are indications that markets are stabilizing through U.S. gas-to-coal switching, higher European coal-fueled generation and increased China infrastructure spending." Investors are likely hoping what Boyce is really saying is that the coal industry has finally hit a cyclical bottom.

Personally, I'll be staying away from the company, as there are too many variables at play -- especially the role of natural gas in providing energy in the future -- for me to make a long-term bet.

Instead, I think there are better places to look. With the swelling of the global middle-class, energy consumption will skyrocket over the next few decades, and long-term investors know that you want exposure to this space now.

We've picked one incredible natural gas company that presents a rare "double-play" investment opportunity today. We're calling it The One Energy Stock You Must Own Before 2014, and you can uncover it today, totally free, in our free research report. Click here to read more.

The article What's Behind Peabody's Big Jump? originally appeared on Fool.com.

Fool contributor Brian Stoffel has no positions in the stocks mentioned above. The Motley Fool has the following options: long JAN 2013 $16.00 calls on Chesapeake Energy, short JAN 2014 $15.00 puts on Chesapeake Energy, long JAN 2014 $20.00 calls on Chesapeake Energy, and long JAN 2014 $30.00 calls on Chesapeake Energy. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.