Is Intel Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what Intel's (NAS: INTC) recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell Intel's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much Intel's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Intel's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is Intel managing its resources well? A company's return on equity should be improving, and its debt to equity ratio declining, if it's to earn our approval.

Healthy dividends are always welcome, so we'll also make sure that Intel's dividend payouts are increasing, but at a level that can be sustained by its free cash flow.

By the numbers

Now, let's take a look at Intel's key statistics:

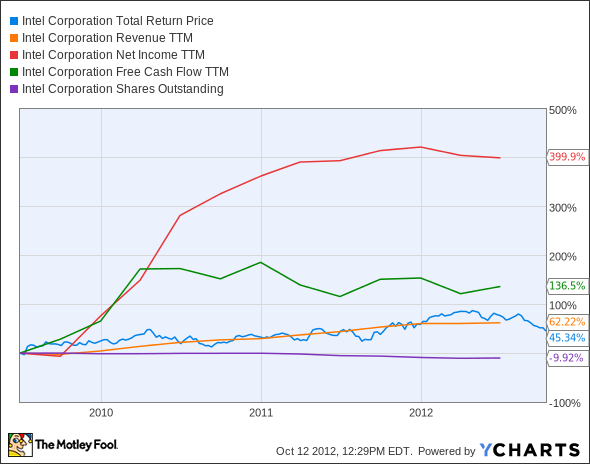

Intel Total Return Price data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | 62.2% | Pass |

Improving profit margin | 5.9% | Pass |

Free cash flow growth > net income growth | 136.5% vs. 399.9% | Fail |

Improving EPS | 475.6% | Pass |

Stock growth (+ 15%) < EPS growth | 45.3% vs. 475.6% | Pass |

Source: YCharts. *Period begins at end of Q2 2009.

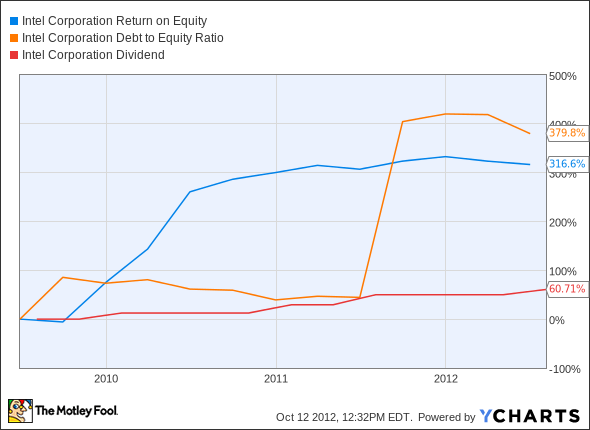

Intel Return on Equity data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 316.6% | Pass |

Declining debt to equity | 379.8% | Fail |

Dividend growth > 25% | 60.7% | Pass |

Free cash flow payout ratio < 50% | 45.1% | Pass |

Source: YCharts. *Period begins at end of Q2 2009.

How we got here and where we're going

Intel earns high marks, with seven out of nine possible passing grades. Intel has rebounded impressively out of the recession, as the numbers show. However, the market's taking that growth with a grain of salt, treating everything short of a blowout as signs of impending doom.

It's been an up-and-down year for Intel, which hit a high in the spring only to spend all summer wilting from the heat in a field of slowly dying PC manufacturers. The chip maker seems to be caught between a rock and a hard place. The three largest PC makers by market share are all suffering year-over-year declines in shipments. Hewlett-Packard (NYS: HPQ) shipped only four PCs this year for every five it shipped last year. Dell (NAS: DELL) lost almost 16% of its sales. Even Apple (NAS: AAPL) , which (unlike HP and Dell) exclusively uses Intel CPUs and also boasts one of the strongest brands in the world, sold 6% fewer Macs than it did in 2011.

Intel finally set foot on the shores of Mobile-ania this year by securing the key spot in six new smartphones. The problem, as fellow Fool Tim Brugger points out, is that these devices aren't compatible with 4G networks. Intel's climb may not seem insurmountable, as ARM Holdings (NAS: ARMH) licensee Qualcomm (NAS: QCOM) powers just under half of the smartphone market. Keep in mind, though, that ARM owns virtually all of the smartphone processor market through licensing deals with every major chip maker not named Intel. Breaking a near-complete architecture stranglehold will be a tall order, and Intel's got a long way to go. Its current smartphone market share? A tenth of a percent.

Microsoft's (NAS: MSFT) Windows 8 is a big opportunity for Intel to claim some defensible territory, and the success (or failure) of its release, planned for later this month, will probably impact market sentiment toward Intel. Intel CEO Paul Otellini seems to have doubts that the launch will go well, and stumbles or setbacks are likely to affect both Microsoft and Intel heading into the holiday season.

There's a lot happening in the near future that will impact Intel's numbers, but few people can say with any clarity what that affect will be. That tends to happen a lot in the tech industry.

Putting the pieces together

Intel has many of the qualities that make up a great stock, but no stock is truly perfect. Digging deeper can help you uncover the answers you need to make a great buy -- or to stay away from a stock that's going nowhere.

With so much happening, it helps to have clear and unbiased information on your favorite stocks. The Fool's premium research service can help you decide whether or not Intel is worth buying now. Our top analysts have dug deep to get you the details you need for an informed decision. Click here to subscribe today.

Keep track of Intel by adding it to your free stock Watchlist.

The article Is Intel Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool owns shares of Apple, Intel, Microsoft, and Qualcomm. Motley Fool newsletter services recommend Apple and Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.