3 Things to Watch with Abbott's Upcoming Earnings

Give Abbott Labs (NYS: ABT) an "A" so far in 2012. Total return, including share appreciation and dividend payments topped 27%. The company recently declared its 355th consecutive quarterly dividend. That streak goes back to the year that Calvin Coolidge was elected President.

As my fellow Fool Brian Orelli recently reported, pharma, in general, is on fire. And Abbott's flames were hotter than most, beating out solid-performers Merck (NYS: MRK) and Pfizer (NYS: PFE) , whose total returns year-to-date are 22% and 18%, respectively.

But another report card time approaches. Abbott announces earnings results for third quarter on Oct. 17. Will this star student get yet another "A?" Here are three keys to its continued success.

1. Humira horsepower

Abbott's strength continues to be powered by Humira. The drug accounted for $4.2 billion in sales during the first half of this year That's nearly 43% of the company's total revenue for the period.

Humira keeps on running strong, as do its rivals. Enbrel, marketed by Amgen (NAS: AMGN) , and Pfizer, totaled sales of $7.2 billion last year. In 2011, combined sales for Remicade, jointly marketed by Johnson & Johnson (NYS: JNJ) and Merck (NYS: MRK) , were $8.2 billion. However, some expect Humira to emerge from the pack as the world's next biggest-selling drug.

Recent news certainly helps bolster that opinion. The FDA approved use of Humira in treating ulcerative colitis a few weeks ago. A month prior to that, the European Commission approved the drug for expanded treatment of Crohn's disease.

I expect continued solid results for Humira in Abbott's earnings announcement.

2. Generic gyrations

While Humira continues to hum along, Abbott's generic drug sales sputter along. Revenue for what the company calls "established pharmaceuticals" fell 6% in the second quarter of 2012 compared to the previous year. That followed a first quarter year-on-year decline of 1.5%.

Abbott attributes the problems in part to European "pricing pressures," particularly with Clarithromycin and Serc. The company saw growth in emerging markets for its generic drugs, though.

Generic drugs generated $5.4 billion in sales in 2011, so we're not talking about small dollars. A continued downtrend could hurt.

3. Currency comeback

One important key to Abbott's success doesn't get as much visibility as others. Currency fluctuations have the potential for wreaking havoc on the company's earnings.

In the second quarter, Abbott stated that unfavorable foreign exchange caused sales to be 4.7% less than they would have been otherwise. Fortunately, Abbott's overall results were strong enough to overcome these headwinds.

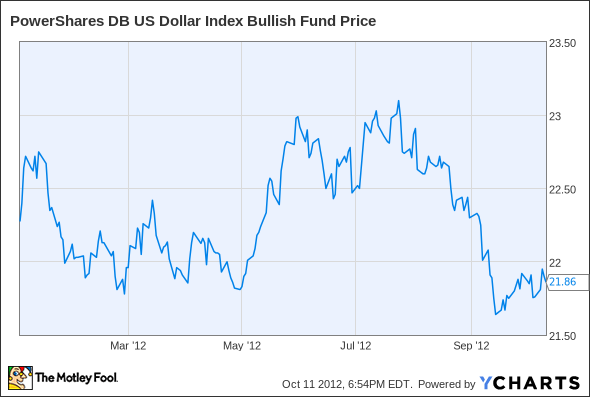

So, how will currency impact Abbott's third quarter results? If we look at the PowerShares DB U.S. Dollar Index ETF (NYS: UUP) as a proxy for the strength of the U.S. dollar against other currencies, we can see some general trends.

During first quarter, the dollar experienced an overall downtrend. Abbott's negative impact from foreign exchange was only 1.3% for the quarter.

The dollar rose against other currencies during the second quarter. As we saw earlier, Abbott suffered fairly significantly from negative foreign exchange effects during the quarter.

The UUP ETF (and, therefore, the dollar) fell again in third quarter. This could be a good sign. While just looking at the dollar against a basket of currencies admittedly permits only a rough analysis, it seems quite possible that Abbott will experience less of an impact from foreign exchange in its third quarter results than it did last quarter.

Ace in the hole

Anything can happen with earnings announcements, of course. The above three factors are important, but other variables could impact earnings positively or negatively.

Over the long run, though, I think Abbott is an excellent choice for investors. With a solid 2.9% dividend and strong drugs in its portfolio, plus opportunities associated with its upcoming spin-off, this stock looks like it might be an ace in the hole.

The article 3 Things to Watch with Abbott's Upcoming Earnings originally appeared on Fool.com.

Keith Speights has no positions in the stocks mentioned above. The Motley Fool owns shares of Johnson & Johnson. Motley Fool newsletter services recommend Johnson & Johnson. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.