Is SandRidge Energy Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what SandRidge Energy's (NYS: SD) recent results tell us about its potential for future gains.

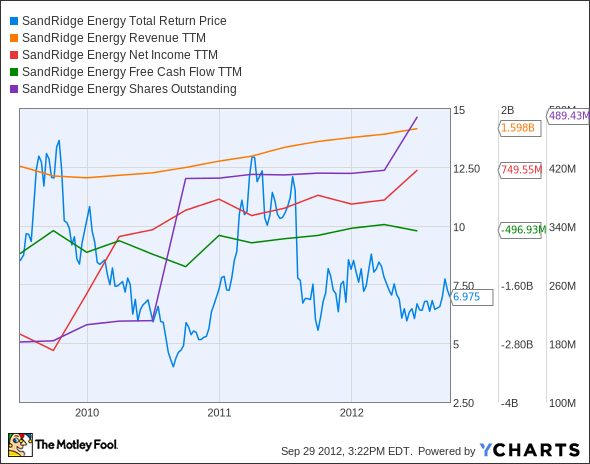

What the numbers tell you

The graphs you're about to see tell SandRidge's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always be reported at a steady rate, we'll also look at how much SandRidge's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If SandRidge's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is SandRidge managing its resources well? A company's return on equity should be improving, and its debt to equity ratio declining, if it's to earn our approval.

By the numbers

Now, let's take a look at SandRidge's key statistics:

SD Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue Growth > 30% | 93.0% | Pass |

Improving Profit Margin | 174.1% | Pass |

Free Cash Flow Growth > Net Income Growth | 48.4% vs. 128.7% | Fail |

Improving Earnings per Share | 108.5% | Pass |

Stock Growth + 15% < EPS Growth | (18.1%) vs. 108.5% | Pass |

Source: YCharts. * Period begins at end of Q2 2009.

SD Return on Equity data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving Return on Equity | 110.4% | Pass |

Declining Debt to Equity** | (57.9%) | Pass |

Source: YCharts. * Period begins at end of Q2 2009. **Two-year calculation.

How we got here and where we're going

SandRidge is making good progress in many directions. It doesn't pay dividends, which would have otherwise been analyzed, but it earns an impressive six of seven passing grades.

Part of SandRidge's success in keeping its debt from ballooning as it explores for oil is a preference for spinning off royalty trusts instead of issuing bonds or taking out loans. Unfortunately, that means shareholders have missed out on a lot of potential dividends. The company's trusts, SandRidge Mississippian Trust I (NYS: SDT) , SandRidge Mississippian Trust II (NYS: SDR) , and SandRidge Permian Trust (NYS: PER) are collectively worth about as much as their parent company, and collectively paid out $6.20 in dividends per share over the past year for a 9.6% aggregate yield.

Investors may get some solid dividends once SandRidge no longer needs these sources of secondary funding. The company expanded its offshore capabilities this year with the attractively priced acquisition of Dynamic Offshore. Fool contributor Arjun Sreekumar views that move as a win for SandRidge, as it immediately increased production capacity.

One potential red flag is SandRidge management's history at Chesapeake Energy (NYS: CHK) . That company's egregious fiduciary mismanagement does not exactly invoke confidence in SandRidge CEO Tom Ward, a former COO at Chesapeake. Ward's compensation stands out in an industry not known for small executive compensation packages, but the counter-argument is that he's certainly managed to improve SandRidge's key financial metrics by leaps and bounds. Top performance deserves top dollar, doesn't it? Ward could justify his pay package by meeting the ambitious expansion plans SandRidge has in store for the next three years, which include tripling EBITDA and doubling oil production.

Putting the pieces together

SandRidge has some of the qualities that make up a great stock, but no stock is truly perfect. These numbers are likely to change over time, so it's important to keep track of SandRidge's progress.

Investors were startled after SandRidge plummeted when natural gas prices reached 10-year lows, but with the company halfway through its ambitious three year plan to profitability, the future looks bright. If you are unsure about the future of this emerging oil and gas junior, and are looking to find out more about its strengths and weaknesses, you should view this brand new premium report detailing SandRidge's game plan and what to expect from the company going forward. To get started--click here!

The article Is SandRidge Energy Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of SandRidge Mississippian Trust II. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.