Is Alcatel-Lucent Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. This sort of stock offers sustainable gains, with improving financial metrics that support strong price growth. Let's take a look at what Alcatel-Lucent's (NYS: ALU) recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell Alcatel's story, and we'll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company has become more efficient over time. Since profits may not always reported at a steady rate, we'll also look at how much Alcatel's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Alcatel's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

Is Alcatel managing its resources well? A company's return on equity should be improving, and its debt-to-equity ratio declining, if it's to earn our approval.

By the numbers

Now, let's take a look at Alcatel's key statistics:

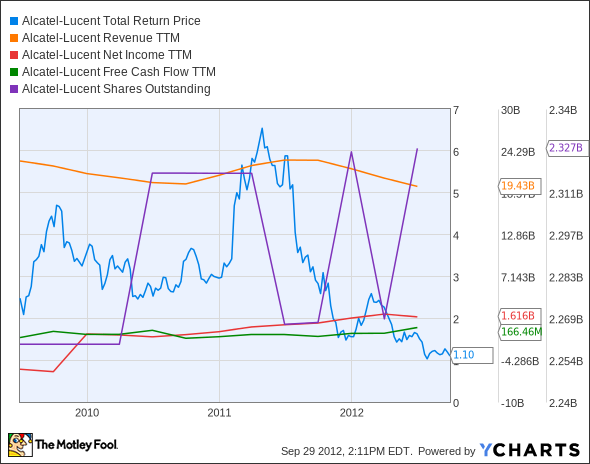

ALU Total Return Price data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue growth > 30% | (15.2%) | Fail |

Improving profit margin | 2,194% | Pass |

Free cash flow growth > Net income growth | 113.8% vs. 129.4% | Fail |

Improving EPS | 575% | Pass |

Stock growth (+ 15%) < EPS growth | (55.7%) vs. 122% | Pass |

Source: YCharts. *Period begins at end of Q2 2009.

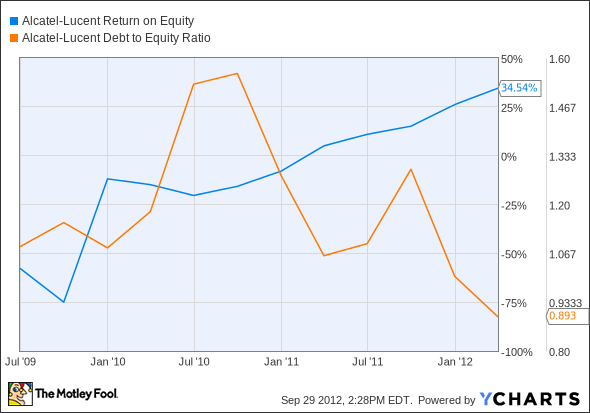

ALU Return on Equity data by YCharts.

Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving return on equity | 159.9% | Pass |

Declining debt to equity | (17.7%) | Pass |

Source: YCharts. *Period begins at end of Q2 2009.

How we got here and where we're going

Alcatel doesn't pay dividends, so our normal dividend evaluation is suspended. The company passes five of its seven remaining tests, which is a good showing for a company that's had such a rough go over the past few years.

Although its numbers have been trending positive, Alcatel's most recent earnings were much weaker than that trend, and the company may wind up losing a few of its passing grades if it can't diversify away from cratering Europe while simultaneously hacking its weighty costs down to a more manageable size.

Although Alcatel's well-known for its networking hardware, the company's attempting to be relevant in more diverse ways as the world connects to ever-more mobile devices. It teamed up with Telefonica (NYS: TEF) and Qualcomm (NAS: QCOM) this summer to transform the nonprofit Mozilla foundation's Firefox browser into a lightweight mobile operating system. That move deepens its partnership with Telefonica, which contracted Alcatel to help build out 3G coverage in popular public spaces.

Alcatel's American hopes are pinned to Verizon's (NYS: VZ) 4G rollout. The company already boasts the largest 4G network, but consumers clamoring for more speed across the country should (hopefully) keep Verizon's capital spending high, and Alcatel's bottom line padded. Internationally, France Telecom (NYS: FTE) provides one faint bright spot in Europe's malaise, with an ambitious plan to grow its fiber network with Alcatel's products.

That may not be enough. Alcatel's executive team is on the chopping block, along with 5,000 employees, as worldwide weakness could easily undo the company's fragile gains of recent quarters. An economic downturn would be devastating for Alcatel as the companies it depends on for capital spending all tighten their belts simultaneously.

Putting the pieces together

Alcatel has some of the qualities that make up a great stock, but no stock is truly perfect. These numbers are likely to change over time, so it's important to keep track of Alcatel's progress. The Fool is here to help. When you add Alcatel to your free personalized Watchlist, you'll get updates whenever we uncover any news you'll need.

Telecom companies might not be your best bet in a downturn, but the Fool's Top Stock for 2012 has the stability and business model to withstand any looming recessions. Consumers will always need to eat, and this company offers scale and low prices in one of the world's brightest growth spots. Find out more about this buying opportunity in the Fool's exclusive free report. Click here for your free copy now.

The article Is Alcatel-Lucent Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of Qualcomm and France Telecom. Motley Fool newsletter services have recommended buying shares of France Telecom. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.