Is ConocoPhillips Destined for Greatness?

Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let's take a look at what ConocoPhillips' (NYS: COP) recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you're about to see tell Conoco's story, and we'll be grading the quality of that story in several ways.

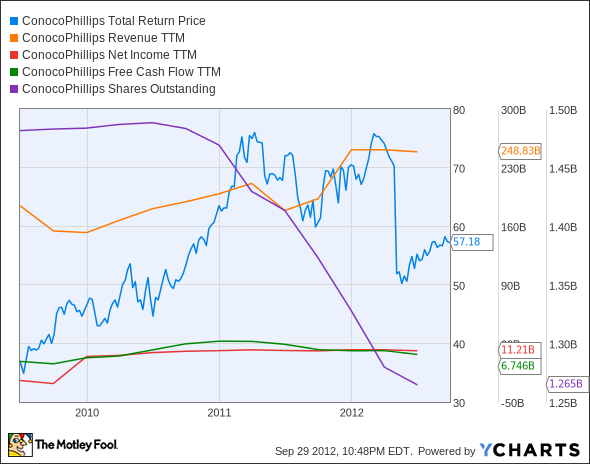

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company's become more efficient over time. Since profits may not always be reported at a steady rate, we'll also look at how much Conoco's free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Conoco's share price has kept pace with its earnings growth, that's another good sign that its stock can move higher.

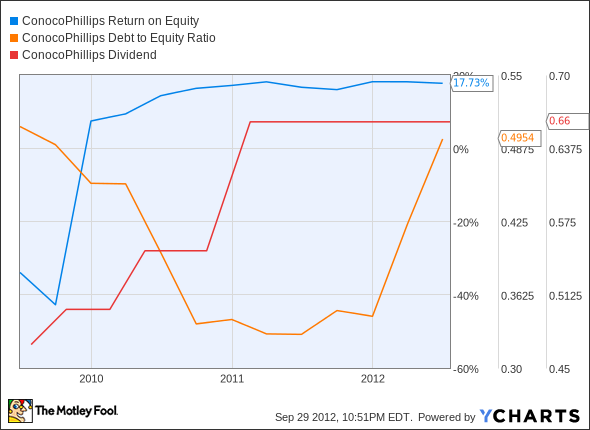

Is Conoco managing its resources well? A company's return on equity should be improving, and its debt to equity ratio declining, if it's to earn our approval.

Healthy dividends are always welcome, so we'll make sure that Conoco's dividend payouts are increasing, but at a level that can be sustained by its free cash flow.

By the numbers

Now, let's take a look at Conoco's key statistics:

COP Total Return Price data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Revenue Growth > 30% | 63.3% | Pass |

Improving Profit Margin | 408.3% | Pass |

Free Cash Flow Growth > Net Income Growth | 133.6% vs. 154% | Fail |

Improving Earnings per Share | 190.5% | Pass |

Stock Growth (+ 15%) < EPS Growth | 28.9% vs. 190.5% | Pass |

Source: YCharts. * Period begins at end of Q2 2009.

COP Return on Equity data by YCharts

Passing Criteria | 3-Year* Change | Grade |

|---|---|---|

Improving Return on Equity | 152.3% | Pass |

Declining Debt to Equity | (2.1%) | Pass |

Dividend Growth > 25% | 40.4% | Pass |

Free Cash Flow Payout Ratio < 50% | 50.9% | Fail |

Source: YCharts. * Period begins at end of Q2 2009.

How we got here and where we're going

Conoco earns seven of nine possible passing grades, and only misses its eighth pass by a hair. That high payout ratio could get worse, as Conoco recently spun off refinery arm Phillips 66 (NYS: PSX) , and its remaining assets have seen production declines.

The Phillips 66 spinoff excised a major chunk out of its parent company, which explains the big stock price drop this year. Conoco might not be able to maintain the same high dividend payouts shareholders have been used to, but its remaining assets are more profitable than Phillips 66's refinery operations. Conoco's still the largest independent oil and gas producer in the world, and is busily developing several major unconventional plays to improve its production volumes.

Conoco's no longer a direct competitor to ExxonMobil (NYS: XOM) or Chevron (NYS: CVX) , although all have dealt with recent production declines. Its lack of integrated refining capacity relative to these two oil giants may hurt it down the line -- you'll need to keep a close eye on Conoco's margins in the coming quarters as it establishes a refinery-free financial history. Fool contributor Arjun Sreekumar points out that the locations of Conoco's former refineries forced them to handle transatlantic oil, which ate into margins with its higher prices.

The company's greater focus on natural gas may also (finally) grant it a stronger position than some oil-focused producers. The United States Natural Gas Fund (NYS: UNG) has finally taken off over the last six months, gaining 32% as the price of crude has declined.

Putting the pieces together

Conoco has many of the qualities that make up a great stock, but no stock is truly perfect. These numbers are likely to change over time, so it's important to keep track of Conoco's progress. The Fool is here to help. When you add Conoco to your free personalized Watchlist, you'll get updates whenever we uncover any news you'll need.

Looking for other ways to play the surprising rebound in natural gas? The Fool's found a stock that sits on the metaphorical mother lode. It's "The One Energy Stock You Must Own Before 2014," handpicked by our energy analysts for its stability, assets, and hefty dividend yield. All the information you need is available in our exclusive free report, so click here to claim your copy now at no cost.

The article Is ConocoPhillips Destined for Greatness? originally appeared on Fool.com.

Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights.The Motley Fool owns shares of ExxonMobil. Motley Fool newsletter services have recommended buying shares of Chevron. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.