These 3 Stocks, Slaughtered in September, Are on Sale

September has been a rough month for some investors, especially if they owned a piece of the three companies I'm covering below.

But in the game that is the stock market, investors are typically more concerned with what the future holds than what's happened in the past month. I actually think all three of these companies are on sale right now, and I'm backing those picks up in my All-Star CAPS profile.

Read all the way to the end and I'll offer access to a special free report that will introduce you to three stocks to own for the next industrial revolution.

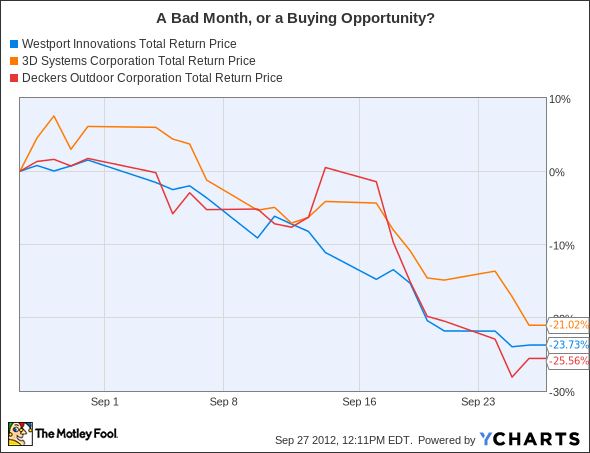

But first, here's a look at how the past month has treated investors in these three companies.

WPRT Total Return Price data by YCharts.

Westport Innovations (NAS: WPRT)

Westport designs natural gas engines for cars, trucks, and other forms of heavy machinery. The technology is especially important since many believe that natural gas will become the fuel of choice in the future.

Obviously, there's a lot of potential here, but there are also a lot of pitfalls. If natural gas filling stations are never built, and if the fuel doesn't catch on, that would hurt the company's shareholders.

There's also the fact that Westport doesn't actually manufacture any of its engines; it simply partners with other companies and designs the technology for natural gas engines in their respective machines.

In the past, the company's biggest partnership was with Cummins (NYS: CMI) , an original equipment manufacturer of engines for long-haul trucks. While that has gone well, investors were spooked earlier this year when Cummins announced it would be making its own natural gas engine moving forward.

One of the weaknesses investors are focused on now is that industrial companies, which make up a large base of Westport's clients, are showing slowed demand. To me, though, that's a short-term concern. Westport's revenue has climbed 134% in the first half of 2012, and I'm comfortable with my bullish CAPScall.

Deckers (NAS: DECK)

This shoe company is responsible for a lot of popular brands, including Simple, Tsubo, and Teva sandals. But no brand is more important to the company than UGG boots, which accounted for two-thirds of all sales in 2011.

Recently, there has been a buildup of inventory and rising prices for the sheepskin that the company uses to make its popular cold-weather boots. Throw on top of that an ill-timed and aggressive expansion into Europe, and there's more than enough to explain the company's fall from almost $120 one year ago to about $50 at the beginning of September.

But the bad news didn't end there. In mid-September, an analyst for Sterne Agee made a bearish call on the company given Deckers' decision to cut the prices of UGG boots by 5% to 8%.

It's never a good sign when a company has to cut the price of its premium brand; other high-end retailers like lululemon athletica (NAS: LULU) have faced similar pressures but haven't cut prices on their core products.

But I'm holding out hope. For one thing, I don't necessarily think the company is suffering because of poor management. Sometimes, timing just doesn't work out, as has been the case in Europe. And Deckers has very little control over the price of sheepskin.

Now, just because shareholders' woes are not due to self-inflicted wounds doesn't mean that the company will automatically recover. But I have faith in CEO Angel Martinez, who recently bought 10,000 shares on the open market, to see the company through this rough patch.

Throw in there the fact that the company is now trading for just eight times earnings (though it trades for a higher 19 times free cash flow), and the fact that the overall company is now worth just $1.3 billion, and I think we could have a long-term winner here.

3D Systems (NYS: DDD)

If you're not familiar with what 3-D printing actually is, get a quick primer here, and a real-world example of the disruption the technology could cause here.

Go ahead and skim them, I'll wait...

Done? Good, then you at least have a taste for the type of potential this technology has. Currently, 3D Systems is one of the only viable behemoths in world of 3-D printing.

I won't beat around the bush: the company isn't cheap. Today's price is roughly twice what it was one year ago, and the company is currently trading hands at 56 times earnings, and 46 times free cash flow.

On the other hand, revenue has grown by about 30% per year and that growth is accelerating. Earnings were also up 81% in the past year.

In the end, my overall thesis is actually pretty simple: if 3-D printing really offers solutions that people want, 3D Systems' current market cap of $1.8 billion will seem tiny in ten years.

If you'd like to find out more about 3-D printing and its potential, check out our special free report: "3 Stocks to Own for the New Industrial Revolution." I'll let you know that 3D Systems is already one of them, but to find out the other two companies, you'll have to get a copy of the report. Check it out today, absolutely free!

The article These 3 Stocks, Slaughtered in September, Are on Sale originally appeared on Fool.com.

Fool contributor Brian Stoffel owns shares of Deckers, Lululemon, and Westport Innovations. The Motley Fool owns shares of Westport Innovations, Lululemon, and Cummins. Motley Fool newsletter services have recommended buying shares of Cummins, Westport Innovations, 3D Systems, Deckers Outdoor, and Lululemon. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.