Analysts Debate: Has Michael Kors Become a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing Michael Kors (NAS: KORS) , a popular luxury retailer that's already seen its stock price double since going public late last year.

Michael Kors by the numbers

Here's a quick snapshot of the company's most important numbers:

Statistic | Result (TTM or most recent available) |

|---|---|

Market Cap | $11.0 billion |

P/E and Forward P/E | 58.3 / 32.8 |

Price to Sales | 6.9 |

Revenue | $1.47 billion |

Net Income | $175.9 million |

Cash | $162.1 million |

Retail Stores (global total) | 253 |

Retail Revenue (% of total) | 48% |

Wholesale Partners (global total) | 2,809 department and specialty stores |

Wholesale Revenue (% of total) | 47% |

Sources: Yahoo! Finance, corporate reports, and industry analyses. TTM = trailing 12 months.

Alex's take

I'll be the first to admit that I don't know much about women's fashion. I've never seen Project Runway, which helped turn Michael Kors into a fashion force. That rather limited understanding led me to give Kors an underperform call on my personal CAPS page shortly after its IPO. That call's been one of my worst performers, as you might expect, and I decided to close it during the course of my Kors research for this article.

The genesis of this article came during a discussion with one of my fashion-conscious and stock-savvy female friends, who suggested I look into Kors, adding this endorsement: "Getting a Michael Kors bag is like getting a Coach [ (NYS: COH) ] bag years ago." If Kors is the new Coach, then the past year's growth may very well be just the beginning. Here's how Coach has done in the past decade:

COH Total Return Price data by YCharts

Pretty impressive, isn't it? I wanted to compare the two companies on the same baseline, which involves going back to Coach's earliest public filings to examine its growth rates leading up to (and immediately following) its IPO. Coach started with far more worldwide retail stores than Kors, but Kors has quickly narrowed the gap:

Sources: Corporate SEC filings. Date ranges: 1998-2002 for Coach, 2008-2012 for Michael Kors.

Not only has Kors enjoyed rapid expansion over the past five years, it's also made greater use of department-store partnerships to really ramp up its sales totals in the first five years for which data is available:

Sources: Corporate SEC filings. Date ranges: 1998-2002 for Coach, 2008-2012 for Michael Kors.

Kors managed to grow its retail sales by double-digit percentages in every year of the past five reported, save 2009, when it still managed a 6.3% comparable-store sales growth rate in the middle of a global recession. For the past two fiscal years, Kors has averaged over 40% in annual comparable-store sales growth.

That sort of growth can't be sustained indefinitely, but Kors has a lot of international potential left, since its outlets are still predominantly located in the United States. The company is also more highly valued than nearly every luxury-retail peer, but that can be largely chalked up to its booming growth rates.

Analysts expect growth to proceed at a relatively modest 27% next year, but over the next five years Kors is expected to grow by 31% annually. If the brand is indeed the new Coach, then that might be a conservative estimate. Its forward P/E puts it in line with other consumer favorites, which makes me more comfortable with its current high price. I'm willing to change my tune on this hot fashion stock and give it an outperform call today.

Sean's take

It's a bird, it's a plane, no... it's Michael Kors' same-store sales figures, which continue to leap tall buildings in a single bound.

Michael Kors' formula for success is very similar to what True Religion Apparel (NAS: TRLG) has done: move away from the wholesale side of the business and aggressively open bricks-and-mortar locations to push higher-margin premium brand merchandise. It's hooked up with Fossil (NAS: FOSL) , which manufacturers its watches that it then rebrands under the Michael Kors name, and has seen sales explode as it begins moving its operations internationally.

Last week, Michael Kors noted its same-store sales were up 45.1% quarter-to-date, and boosted its EPS forecast for the remainder of the year. In spite of this, I still have my doubts.

Don't get me wrong, I wouldn't dare stand in the way of this freight train at the moment, but I don't have the brass to buy into a retailer valued at 33 times forward earnings, either. There are just too many variables in the retail sector that could go wrong.

To begin with, consumer spending habits can change rapidly and even Michael Kors, as a predominantly higher-end retailer, isn't immune to product shifts. Spending activity from Coach and luxury jeweler Tiffany (NYS: TIF) would indicate consumers aren't spending as freely as they were 12 months ago. Second, transitioning to a bricks-and-mortar atmosphere isn't easy -- just ask True Religion. True Religion is on the right path to success, but has learned that rising input costs and international pressure is a concern. Finally, growth trends eventually slow down -- a trend investors rarely seem to anticipate or are willing to accept.

For now, I'd rather be a spectator than attempting to make a call on Michael Kors. I wouldn't stand in the way of its incredible same-store sales growth over the near-term, but I feel it wise to avoid the inevitable slowdown in growth that'll be caused by a mixture of rising input costs and changing consumer trends.

Travis' take

Fashion is a fickle business. There may not be another industry that can rise and fall as quickly as fashion, and when adding retail to the mix it magnifies the trend.

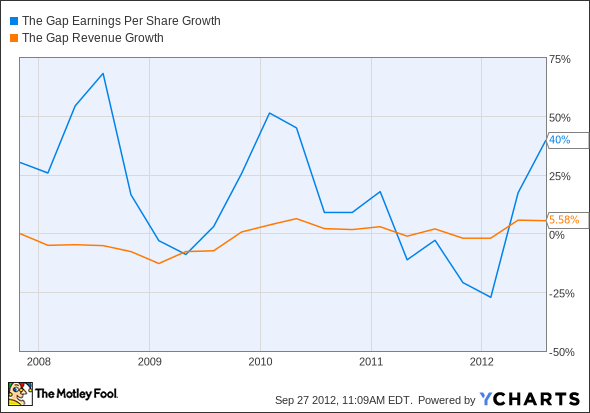

One of the reasons retailers see such a wild swing in earnings is that they're highly levered businesses, even though their balance sheets may not be leveraged. Think about a store like Gap, which rose to retail fame on the back of teen spending a decade ago. When we went into the recession, sales fell and profitability plunged. As sales rose and fell and rose again over the next three years, profit growth was a multiple of revenue growth.

GPS Earnings-per-share growth data by YCharts

This is because retailers and fashion companies have relatively fixed operating costs and relatively high margins. If it costs a million dollars to operate a store for a year and you have $3.0 million in sales at a 40% gross margin, you only make a $200,000 profit. If sales grow 33% to $4.0 million the next year and you have the same 40% gross margin, profits triple to $600,000. That's how operating leverage works.

Michael Kors is riding a hot trend, and I'm not one to get in the way. In fact, I think the incredible growth makes Michael Kors' 30.3 forward P/E ratio look relatively inexpensive. The company can grow quickly enough to justify the price and it has beaten earnings estimates by an average of 77% over the past three quarters, so the forward price may be even lower.

I'll go along with Alex's outperform call, but I admit that I'd like to keep this on a short leash. I like playing in the very high end of retail right now because that's where the disposable income is, but if the company's growth doesn't stay at a high level, this could be a big bust. We'll check back periodically and make sure this fashion company doesn't go out of fashion before we cash out.

The final call

With two in favor and Sean abstaining, it looks like Michael Kors earns an outperform CAPScall from us today, but we'll keep it to a six-month period for now to account for Travis' short leash and Sean's wariness. Our TMFYoungGuns CAPS portfolio is currently beating the market by 87 points after 18 picks so far this year, and we hope Kors' fashion-conscious consumers help push that number even higher.

Michael Kors is off to a great start, but it's not the only stock making waves in high-end retail. The Fool's latest free report highlights "3 Companies Ready to Rule Retail," with a detailed analysis of their long-term prospects. It's available at no cost for a limited time, so find out more today -- click here to get the information you need.

The article Analysts Debate: Has Michael Kors Become a Top Stock? originally appeared on Fool.com.

Fool contributors Travis Hoium, Alex Planes, and Sean Williams do not have positions in any companies mentioned here. You can follow Travis on Twitter at @FlushDrawFool, Sean at @TMFUltraLong, and Alex at @TMFBiggles.The Motley Fool owns shares of Coach and Tiffany. Motley Fool newsletter services have recommended buying shares of Coach and Fossil. Motley Fool newsletter services have recommended shorting Fossil and Tiffany. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.