3 Things to Watch at Energy Transfer Partners

Energy Transfer Partners (NYS: ETP) is a midstream master limited partnership, or MLP, based in Dallas. Since the end of 2010, ETP has announced $3 billion worth of organic growth projects, the majority of which will be online and in service by the end of this year, indicating that the partnership may be on the verge of some big time returns for investors.

Today, we'll take a look at three things investors need to keep an eye on when evaluating ETP for their portfolios.

1. A return to distribution growth

All eyes are on ETP's distributable cash flow right now. The reason investors love buying MLPs is because the tax structure of these entities typically begets high yields. The partnership hasn't increased its distribution since 2008, but with close to $2 billion in new projects coming online by the end of 2012, investors have high expectations for an increase in 2013.

This is a key issue affecting ETP's share price right now, and it is not unreasonable to also expect a pop in the stock once ETP announces a return to distribution growth. Let's quickly compare ETP's share price performance over the last five years to midstream MLP peers Kinder Morgan Energy Partners (NYS: KMP) , Plains All American Pipeline (NYS: PAA) and Enterprise Products Partners (NYS: EPD) .

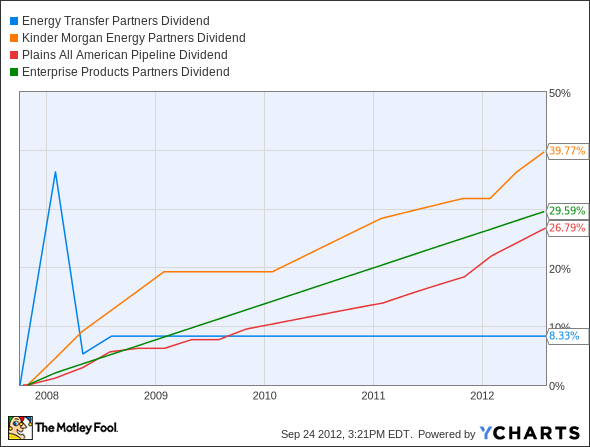

And now let's do the same thing with its dividend history:

ETP Dividend data by YCharts

All three of its competitors have increased distribution payments over time, Kinder Morgan leading the way percentage-wise, though Enterprise and Plains have more consistent performances.

ETP's annualized unit distribution has held steady at $3.58 for the last four years. It hasn't decreased, which is good; but, with so many MLP's growing their distributions, frankly, investors have had better options for returns.

ETP's management has listed the goal of achieving a 1.05 times distribution coverage ratio. It is currently sitting below 1.00 times coverage.

2. Managing new assets

The sheer volume of ETP's growth projects, combined with recent strategic acquisitions, lends itself well to increasing its distribution. But, if the company can't manage its new size, then there could be trouble.

ETP put in a bid for Sunoco because of its crude oil and petroleum products distribution capabilities. The company also picked up Sunoco's marketing segment however, which means ETP is the now proud owner of 4,900 gas station convenience stores. Analysts are quick to point out that ETP has no business operating a bevy of tight margin gas retailers, and investors should keep a close eye on how the partnership handles this part of the acquisition going forward.

Though ETP's management has a long history of integrating new assets successfully, the company has no prior experience with the marketing and retail assets it acquired from Sunoco. The complexity may prove to be a challenge for ETP's management, and if it continues to hold those assets and can't manage them properly, the affects will certainly show up on the balance sheet.

3. Diversification

Organic growth projects and the Sunoco acquisition were part of ETP's plan to diversify its asset portfolio. Though these measures have certainly helped diversify its business mix, 66% of the partnership's revenue still comes from natural gas pipelines and midstream operations. If U.S. natural gas producers continue to move away from gas production, particularly in Texas where the partnership has most of its assets, ETP could suffer. The flip side is also true, however, and any increase in the price of dry gas and NGLs that boosts production will serve ETP and its investors quite well.

The partnership also has worked to grow its asset footprint outside of Texas, which is equally important to diversifying the assets themselves. Most of the Sunoco assets are in the northeast, but another crucial pick-up for ETP was its recent acquisition of a 50% stake in the Citrus pipeline system, which runs from Texas along the Gulf Coast and down into Florida. Florida is a quiet, yet incredibly significant player in the world of natural gas. Second only to Texas, the state generates 62% of its electricity from natural gas. ETP's pick-up is a smart foray into one of the most crucial gas markets in the U.S.

Foolish takeaway

Energy Transfer Partners presents a pretty compelling opportunity for investors right now. The partnership has made some key changes that will very likely make a big impact in 2013. For another forward-looking idea, check out the Fool's newest free report, "The One Energy Stock You Must Own Before 2014."

The article 3 Things to Watch at Energy Transfer Partners originally appeared on Fool.com.

Fool contributor Aimee Duffy holds no position in any company mentioned. Click here to see her holdings and a short bio. If you have the energy, check out what she's keeping an eye on by following her on Twitter, where she goes by @TMFDuffy.Motley Fool newsletter services have recommended buying shares of Enterprise Products Partners. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.