Is This Packaged-Food Company Priced for Perfection?

Shares of B&G Foods (NYS: BGS) hit a 52-week high on Thursday. Let's take a look at how it got there and see whether clear skies are still in the forecast.

How it got here

Rising input costs be damned, B&G Foods is going to be off to the races with or without you!

B&G Foods, a provider of shelf-stable foods and the name behind such brands as Emeril's, Ortega, Mrs. Dash, and Cream of Wheat, has been utilizing its keen eye for a good deal to grow its bottom line and product portfolio through acquisitions over the last couple of years. As I've noted previously, B&G purchased Cream of Wheat from Kraft Foods (NYS: KFT) in 2007, and more recently Mrs. Dash and Kleen Guard from Unilever (NYS: UL) . Just yesterday, B&G announced a $62.5 million acquisition of the New York Style and Old London brands from Chipita America.

In its most recent quarter, B&G attributed a $19.5 million boost in sales from its purchase of Culver Specialty Brands. B&G noted that a mix of higher-margin product and a $4.3 million boost in pricing gains helped raise its operating income by 33% to $35.1 million.

But, as I alluded to earlier, things aren't completely healthy within the packaged-food sector. Food input costs are going through the roof thanks in part to drought conditions throughout the country. Outside of B&G's acquisition of Culver Specialty Brands, net sales from organic operations actually fell by $0.3 million!

B&G shareholders shouldn't feel bad, however, as other packaged-food companies are suffering right alongside B&G, including Kellogg (NYS: K) , which reported a lower second-quarter profit that's been hurt by European weakness and higher commodity costs, and General Mills (NYS: GIS) , which topped EPS estimates this week thanks to numerous one-time gains, but backed a weak U.S. sales forecast that was below Wall Street's estimates.

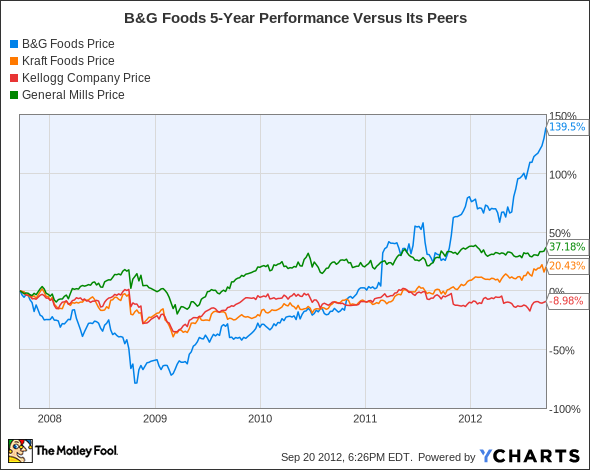

How it stacks up

Let's see how B&G Foods stacks up next to its peers.

As you can see, since 2010, only B&G Foods has been able to tack on significant gains, while the rest of its peers have traded sideways.

Company | Price/Book | Price/Cash Flow | Forward P/E | Dividend Yield |

|---|---|---|---|---|

B&G Foods | 6.4 | 17.7 | 20.8 | 3.1% |

Kraft Foods | 2 | 13.6 | 14.3 | 2.8% |

Kellogg | 8.5 | 11.3 | 13.7 | 3.4% |

General Mills | 4.1 | 11.2 | 12.8 | 3.1% |

Source: Morningstar.

It may not seem like it, but we do actually have some noticeable differentiation here.

Kraft Foods is priced the cheapest relative to book. The upcoming split of its snack food business (to be known as Mondelez International) from its North American food operations should provide better visibility to shareholders and help get that figure more in line with its peers'.

Kellogg and General Mills both are the cheapest on a cash flow basis within this grouping, but both have also had trouble controlling costs and generating sales growth at home and abroad.

B&G Foods is without question the priciest, but its high-yielding dividend is what continues to attract investors. Keep in mind, though, that organic growth was actually negative in the second quarter and it no longer looks like an exceptional value.

What's next

Now for the $64,000 question: What's next for B&G Foods? That depends on how well it can pass along the rising costs of food onto its customers, whether it can continue to make savvy acquisitions, and whether it can lure income seekers with a growing dividend.

Our very own CAPS community gives the company a three-star rating (out of five), with a whopping 94.8% of members expecting it to outperform. As a noted skeptic, is it really that surprising that I'm in the minority on this one, with a CAPScall of underperform that's currently underwater by 34 points?

You might think I'd take my lumps and walk away, but a mixture of stubbornness and common sense is going to keep me on the underperform side here a little bit longer. My main beef still remains: Where is the organic growth?! B&G has been purchasing its way to larger operating income, but if its name brands stagnate after purchase, what's the point? I also don't see B&G as a "super stock," able to overcome food inflation. If prices are hurting General Mills and Kellogg, they're going to hurt B&G, plain and simple. Finally, why are investors paying 21 times forward earnings for a company with negative organic growth? Feel free to try to explain that to me in the comments section below, but I'll remain decidedly negative in the meantime.

If dividends are what you're after, then sit back, relax, and grab a copy of our latest special report on the three Dow dividends you need in your portfolio. This report is free for a limited time only, so click here for your opportunity to see our analysts' choices for top Dow dividend-paying stocks.

The article Is This Packaged-Food Company Priced for Perfection? originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended buying shares of Unilever. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.