Is This Stock a Comforting Value or a Sheepish Play?

Shares of Deckers Outdoor (NAS: DECK) hit a 52-week low on Wednesday. Let's take a look at how it got there, and see if cloudy skies are still in the forecast.

How it got here

Deckers Outdoor, the company behind the fashionable Ugg brand, as well as the Simple, Teva, and Tsubo shoe brands, has been struggling for months, due to rising input costs and expansion miscues.

The cost of sheepskin, which is a primary component of Ugg boots, has been on the rise, and hurting margins for nearly a year now. A more pressing issue, though, has been Deckers' aggressive expansion into Europe during the height of its sovereign debt crisis. In Deckers most recent quarter, net sales rose 13.1%, but it was definitely a tale of two regions, as domestic sales jumped 37%, while international sales backtracked 14%. Deckers plans to move forward with its international expansion plans nonetheless, and to focus on Asia in the coming years.

However, the nail in the coffin came from an admission by Deckers that it plans to reduce the price of its best-selling Ugg boots in light of rising inventory levels and a weakening retail environment. The move doesn't really come as a surprise given that many of its peers' earnings reports have similarly fallen flat. Nike (NYS: NKE) badly missed its earnings estimates, due to a slowdown in Europe and Asia. Crocs' (NAS: CROX) earnings surpassed estimates in the second quarter, but revenue came in about $10 million shy of estimates, due to a 5% decline in sales from Europe. Hush Puppies maker Wolverine World Wide (NYS: WWW) noted earlier this month that it's unlikely to meet its previous sales goals, due to weakness in Europe. Finally, Skechers (NYS: SKX) has produced a loss in three consecutive quarters, due to a demand slowdown.

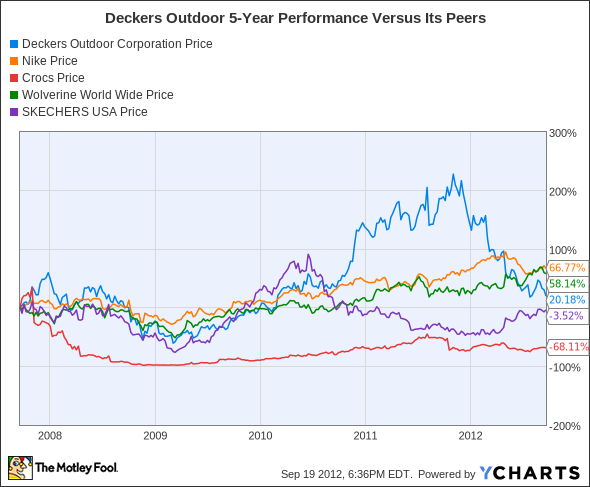

How it stacks up

Let's see how Deckers Outdoor stacks up next to its peers.

Deckers was at one time outperforming its peers by a long shot, but has since been relegated to just a mediocre five-year return.

Company | Price/Book | Price/Cash Flow | Forward P/E | Debt/Equity |

|---|---|---|---|---|

Deckers Outdoor | 2 | 10.8 | 6.7 | 0% |

Nike | 4.3 | 24.1 | 15.6 | 3.7% |

Crocs | 2.7 | 10.7 | 9.9 | 1.9% |

Wolverine World Wide | 3.4 | 18.6 | 13.7 | 4.5% |

Skechers | 1.3 | 7.1 | 43.6 | 15.9% |

Sources: Morningstar, Yahoo! Finance.

One of the first things that stands out is that none of these retailers carries an exorbitant amount of debt. In fact, Deckers is the lone standout that carries no debt whatsoever.

From an overall valuation perspective, both Deckers and Crocs offer the most intriguing value. Crocs continues to get little respect, and has had trouble escaping the "fad" moniker. Similarly, Deckers has worked on expanding its product reliance beyond that of the Ugg brand, (although Ugg still accounts for more than 60% of total sales, but it, too, suffers from the fad stigma.

Skechers is notably inexpensive based on book value and cash flow, but that has a lot to do with its three consecutive quarterly losses more than anything else.

What's next

Now for the $64,000 question: What's next for Deckers Outdoor? That will depend on whether it can keep its input costs under control, and/or pass along rising costs to consumers, whether it can successfully expand its product lines into high-growth China, and whether it can keep a tighter lid on its inventory levels.

Our very own CAPS community gives the company a three-star rating (out of five), with 85.4% of members expecting it to outperform. Currently, I'm among the minority, boasting a CAPScall of underperform on Deckers that's in the positive by a whopping 82 points. However, it's finally time for me to swap my pessimism for a green thumb on Deckers Outdoor.

Why am I switching to an outperform call now? Frankly, this is the first time management has looked at things from a realistic perspective in a while. A price decrease in its Ugg boots was inevitable, and putting it off was only hurting the company over the short run. I would expect both sheepskin costs to level off, and European sales to stabilize in the coming quarters, as Deckers begins to reap substantial benefits from its investments in Asia. Even though I highly question some of the company's marketing activities -- I still seriously want to know who approved this bonehead idea! -- I expect sales growth to remain in the low single digits as the company focuses on its expansion into Asia, improving its operating efficiency, and better controlling its inventory.

If you want the scoop on three companies ready to rule the retail sector right now, then click here to get your copy of our latest special report from Motley Fool Stock Advisor. Oh yeah, did I mention it's free?

The article Is This Stock a Comforting Value or a Sheepish Play? originally appeared on Fool.com.

Fool contributorSean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.Motley Fool newsletter serviceshave recommended buying shares of Deckers Outdoor and Nike, as well as creating a diagonal call position in Nike. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.