China's New Energy Source?

Two weeks ago, China announced a series of infrastructure projects amounting to the country's own hands-on version of quantitative easing. Excited investors poured money into Chinese coal stocks, jostling prices up and down as analysts settled on their new sweet spot. As the trading turmoil settles, let's take a critical look at whether the Chinese government's $280 billion infusion will actually affect this commodity's future.

The big bang

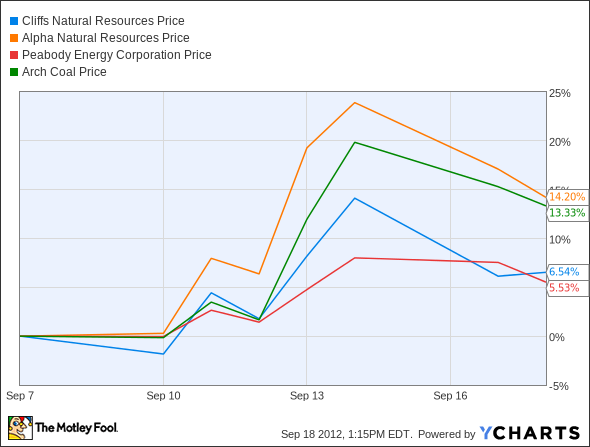

The day after the announcement, shares of Cliffs Natural Resources (NYS: CLF) , Alpha Natural Resources (NYS: ANR) , Peabody Energy (NYS: BTU) , and Arch Coal (NYS: ACI) all jumped more than 10%. Investing in energy is an easy way to get in on the bottom floor of economic growth, and coal is a major player in Chinese steel production.

A week later, each stock peaked, with Alpha Natural topping out at a 23% gain. Since then, each company's shares have steadily declined to post-announcement gains of 5%-14%.

Who's doing what?

To give some context to our story, let's see what each company's past, and its prospects, in China actually look like.

In a September 11 investor presentation, Cliffs Natural Resources outlines expected growth in Chinese steel production and infrastructure investments, but a global footprint map shows that Cliff's Asian direct export presence is currently limited to Russia and Japan.

Cliffs' 2011 acquisition of Consolidated Thompson gives it exposure to China's third-largest steel producer, but a March 2012 conference call presentation puts Cliff's steel exposure into perspective. The company's own projections put metallurgical coal (used for steel production) at only around 15% of total coal production by volume over the next few years.

In Alpha Natural Resources' August quarterly earnings report, the company cites slowing steel production in China as a reason for the recent drop in price of metallurgical coal. With the new stimulus, investors might expect this demand to shoot steel-making-coal prices through the roof. However, Alpha also states that supply is higher than ever due to resolved labor disputes in Australia.

Peabody Energy, the world's largest private sector coal company, could be seen as the perfect match for China, the world's largest coal consumer. But Peabody reports that increases in coal production in the U.S., Indonesia, and Colombia have pushed down seaborne coal prices. For the last quarter, Peabody decreased its metallurgical coal price expectations by a cool 36%.

Peabody's Australian mining segment is its main metallurgical coal producer, and accounted for the largest portion of the company's sales and profit in 2012. Peabody might've lured in a few China bulls with its latest quarterly report. In its "long-term outlook" section, Peabody states that it is "exploring projects" in China and Mongolia.

Arch Coal is the only entirely U.S.-based company listed here. With 18 mines scattered across the South and Midwest, its metallurgical reserves are limited to Appalachia. Last quarter, Arch sold 1.9 million tons of steel-producing coal, just over half of Peabody's 3.6 million tons. Against the geographical and scale advantages of its larger competitors, Arch probably isn't prepared to supply China with coal for its new infrastructure projects.

Rewind, review

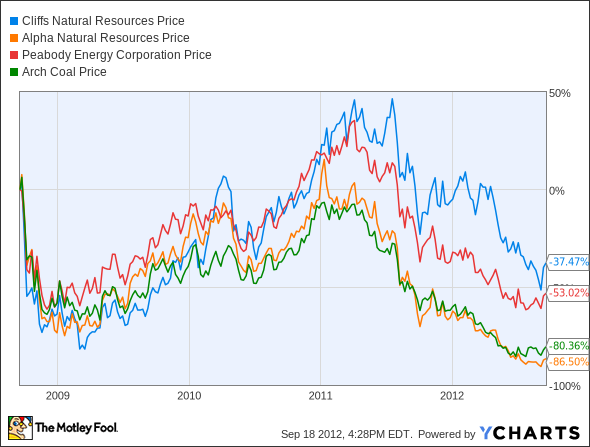

Coal investors have been looking for a reason to love again, and this stimulus announcement served as the commodity's apology letter to its shareholders. But as for me, I'm not jumping back in bed with this beast, high dividends or not. There's a reason that the same companies that saw gains this past month have plummeted over the past four years, and a $280 billion one-time infrastructure investment isn't going to wipe away those memories.

The events of the past two weeks have made me more convinced than ever of coal's ultimate demise. China and India are expected to account for 75% of coal energy demand in the next 20 years, but the very reason this stimulus occurred is due to a slowdown in China's economy. Likewise, corruption scandals in India are tearing its coal infrastructure apart and paving the way for smaller, less capital intensive energy projects.

What now?

Investing in natural gas or renewable energy sources is the long-term strategy that holds more water in my portfolio pool. There are plenty of companies to choose from, many with direct exposure to emerging markets. China has plans to generate at least 15% of its energy from renewables by 2020, and Trina Solar (NYS: TSL) is poised to capture a large portion of that market.

China's announcement will most likely spur economic growth, but don't expect this (or any) country to linger at coal's dirty doorstep. Despite each company's long-term investments and prospects, China isn't looking for a wedded relationship with any one energy source. Adjust your portfolio today for tomorrow's energy use, and reap returns in the years to come.

To help you in your search for the next big energy winner, The Motley Fool has prepared a special free report, "The One Energy Stock You Must Own Before 2014." By investing in this multibillion-dollar energy company, you can get in before its stock rebounds, when natural gas prices eventually do turn upward. And until natural gas prices do rebound (which a top Motley Fool analyst expects will happen by 2014), you can cash in on its stable 5.7% dividend. But hurry, the report is available for a limited time only, so grab your free copy today.

The article China's New Energy Source? originally appeared on Fool.com.

Fool contributor Justin Loiseau owns none of these stocks. You can follow him on Twitter, @TMFJLo, and on Motley Fool CAPS, @TMFJLo. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.