Why Jazz Pharmaceuticals Could Head Even Higher

Shares of Jazz Pharmaceuticals (NAS: JAZZ) hit a 52-week high today. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

Jazz may not be the ideal music to rock out to (that's subjective, of course), but there's little denying that shareholders have been riding this train higher for multiple years now as story after story keeps going in its favor.

Jazz's primary growth driver has been narcolepsy drug Xyrem, which saw sales rise by a brisk 59% in the second quarter to $89.1 million. Although there had been some concern that growth would taper off (and inevitably it will), there's been no indication from Jazz's market-beating results that this is occurring. Just as important, Jazz also appears to be in line to win a ruling it filed against Roxane Laboratories to sell a generic version of Xyrem, according to a Markman letter. With patents clearly in hand, it seems that competition for Xyrem is still a ways off.

Jazz has also grown its other products organically, expanded through acquisition, and jettisoned some of its products to boost its balance sheet.

Psychiatry drug Luvox, though contributing to a smaller portion of sales than Xyrem, still saw sales rise 44% in the second quarter. Jazz's acquisition of EUSA Pharma added acute lymphoblastic leukemia drug Erwinase, while the Azur Pharma acquisition added chronic pain treatment Prialt and schizophrenia drug FazaClo to its rapidly expanding drug portfolio. Finally, Jazz is selling its women's health business for $95 million in cash to specialty pharmaceutical company Meda.

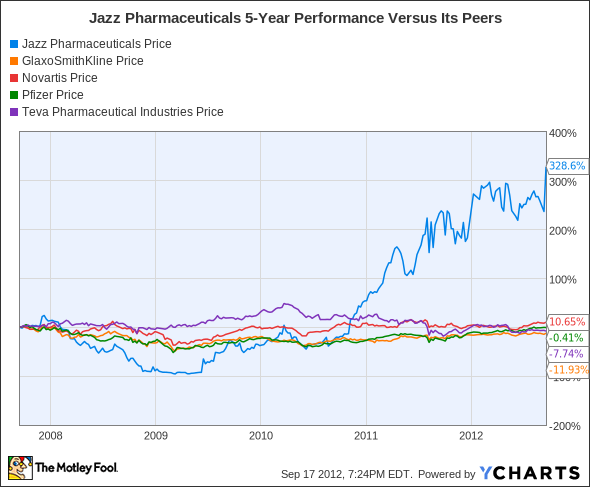

How it stacks up

Let's see how Jazz Pharmaceuticals stacks up next to its peers.

As you can see, Jazz is crushing its narcolepsy competition in terms of performance. However, it should be noted that GlaxoSmithKline (NYS: GSK) , Pfizer (NYS: PFE) , Novartis (NYS: NVS) , and Teva Pharmaceutical (NYS: TEVA) -- which purchased Cephalon -- have far more diverse portfolios than Jazz's.

Company | Price/Book | Price/Cash Flow | Forward P/E |

|---|---|---|---|

Jazz Pharmaceuticals | 4.4 | 17.7 | 13.3 |

GlaxoSmithKline | 10.4 | 11 | 18.4 |

Pfizer | 2.3 | 11.3 | 9.8 |

Novartis | 2.3 | 10.2 | 11 |

Teva Pharmaceutical | 1.5 | 9 | 6.5 |

Source: Morningstar.

One drawback for Jazz shareholders is that every other larger pharmaceutical company here pays a dividend -- except for Jazz. Glaxo pays out nearly 5%, Novartis just north of 4% and Pfizer just below 4%. Even Teva, which pays out nearly 2%, offers the advantage of a diverse generic drug portfolio, as well as the added growth of branded drugs. It's also worth noting that aside from Glaxo, Jazz is handily pricier on paper than the rest of this group.

Where Jazz makes up for its dividend shortcomings is in its growth rates. Xyrem is blowing its competition out of the water in terms of growth, but investors should understand that this is a fiercely competitive field. Provigil and Nuvigil -- acquired by Teva when it purchased Cephalon -- Concerta from Novartis, and Pfizer's Pristiq are all vying for the same space as Xyrem.

What's next

Now for the $64,000 question: What's next for Jazz Pharmaceuticals? That question depends on the success of Xyrem, the ability of Jazz to integrate its newly acquired drugs, and its ability to protect the patents on its exclusive drugs.

Our very own CAPS community gives the company a two-star rating (out of five), with 75.8% of members expecting it to outperform. On the other hand, I've considered this a five-star value for a long time. My current CAPScall on Jazz is up 28 points at the moment.

Earlier in the year, I suggested that it was possible that Jazz could double in value yet again -- we're nearly halfway there. The patent protection ruling on Xyrem will be the key moving forward to protecting Jazz's most valuable drug for many years to come. Jazz has shown an uncanny ability to make acquisitions that are immediately accretive to earnings and has, for the most part, blasted Wall Street's expectations into a pulp quarter-after-quarter. Even here, with a double-digit P/E, I wouldn't be surprised to see EPS estimates rise dramatically over current expectations. In short, I intend to remain long and strong Jazz in my CAPS portfolio.

Just as Jazz Pharmaceuticals is seeking to uncover and commercialize the next disruptive technology in the biotechnology sector, our analysts are seeking out the next disruptive technology that could revolutionize the tech sector. In our latest special report, you can find out the identity of three stocks they feel are set to lead the next industrial revolution. Click here and get this special report, for free, for a limited time!

The article Why Jazz Pharmaceuticals Could Head Even Higher originally appeared on Fool.com.

Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.