Why Procter & Gamble Could Head Even Higher

Shares of Procter & Gamble (NYS: PG) hit a 52-week high on Friday. Let's take a look at how it got there and see whether clear skies are still in the forecast.

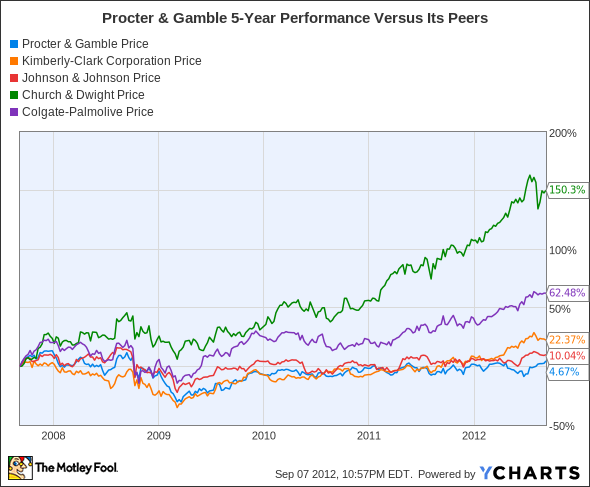

How it got here

If I told you that Procter & Gamble had lowered its outlook twice this year already, you'd probably be in bewilderment, seeing that the stock is currently at a 52-week high -- but it's true! P&G has suffered through a myriad of issues this past year, including weak consumer-spending habits that have caused consumers to trade down to lower-margin products, tough competition, and a stronger dollar that hurts its overseas sales.

In spite of these issues, P&G's resilience has shown through, and it's focused on multiple growth and market-share growth initiatives. To begin with, P&G is watching its costs like a hawk. It announced plans earlier this year to cut 5,700 jobs before the end of its fiscal 2013 but noted that these cuts would be countered with hiring in high-growth emerging-market areas and China. It also made a decent profit in the fourth quarter from the sale of the Pringles snack brand to Kellogg (NYS: K) .

P&G also stands prepared to introduce new products and push its higher-priced household and beauty products. The company feels confident that we're on the precipice of a major shift in consumer trends that will have more people choosing to trade up to brand-name products.

Finally, P&G has price inelasticity on its side. Even though it was forced to scale back some of its price increases earlier this year, many of its products are near-necessity items that offer relative price and cash-flow stability.

What's keeping P&G from moving higher is the following army of hyphens and ampersands: Kimberly-Clark (NYS: KMB) , Johnson & Johnson (NYS: JNJ) , Church & Dwight (NYS: CHD) , and Colgate-Palmolive.

How it stacks up

Let's see how Procter & Gamble stacks up next to its peers.

That would indeed P&G bringing up the rear, with the much smaller Church & Dwight leading the pack.

Company | Price/ Book | Price/ Cash Flow | Forward P/E | Dividend Yield |

|---|---|---|---|---|

Procter & Gamble | 3 | 15.2 | 15.5 | 3.2% |

Kimberly-Clark | 6 | 12.6 | 14.1 | 3.5% |

Johnson & Johnson | 3.1 | 12.1 | 12.2 | 3.5% |

Church & Dwight | 3.9 | 17.6 | 19.8 | 1.6% |

Colgate-Palmolive | 3 | 17.4 | 17.6 | 2.3% |

Source: Morningstar.

One thing about conglomerates is that their financials are often painfully similar, and so it's tough to distinguish strengths and weaknesses. What we can say is that each company here faces a unique set of struggles.

P&G is cheap relative to book value in this group, but it's had trouble maintaining its market share and pricing against other detergent makers. Kimberly-Clark offers a premium dividend at 3.5% but has not had much success in expanding internationally, as I've discussed previously. Johnson & Johnson could be the best value of this group, as it recently completed a $19.7 billion purchase of medical-device maker Synthes. Church & Dwight appears to be the priciest of the group based on these metrics and is also the most recent company here to lower its earnings forecast because of weak consumer spending. Finally, Colgate-Palmolive has felt the pangs of increased input cost inflation.

Each company offers its own set of well-known brand names and steady cash flow, but each has concerns to address about where future growth will come from.

What's next

Now for the $64,000 question: What's next for Procter & Gamble? That question depends on whether it can maintain pricing power, if it can maintain its U.S. market share while promoting growth in emerging markets, and if it can create shareholder value through share buybacks and dividend increases.

Our very own CAPS community gives the company a highly coveted five-star rating, with 96.9% of members expecting it to outperform. I, too, count myself among the vast majority having made a CAPScall on P&G, and mine is currently down about four points.

It's true that P&G has ample challenges that lie ahead, but it's taking the appropriate steps to regain its lost market share and reinvigorate growth. As long as P&G continues its push into emerging markets, uses its pricing power to fend off rising inflationary costs, and rewards shareholders (i.e., the recently initiated $4 billion share buyback), I see little reason this won't head higher over the long run.

While P&G has been a Dow Jones Industrial Average standout stock, the Dow index is a minefield of fantastic dividends. In our latest special report from Stock Advisor, you can find out, for free, which two other companies join P&G as the cream of the crop in Dow dividends. Get this report and claim your investing edge.

The article Why Procter & Gamble Could Head Even Higher originally appeared on Fool.com.

Fool contributorSean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong. The Motley Fool owns shares of Johnson & Johnson.Motley Fool newsletter serviceshave recommended buying shares of Procter & Gamble, Kimberly-Clark, and Johnson & Johnson, as well as creating a diagonal call position in Johnson & Johnson. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policythat's hyphen and ampersand friendly.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.